Advertisement

Thinking about what to do with Coupang stock right now? You are not alone. There has been a lot of buzz around this South Korean e-commerce giant recently, and if you are weighing your next move, it is helpful to look past the headlines and see what the numbers are really telling us. In the past year, Coupang’s stock has delivered an impressive 25.7% total return. Year-to-date gains stand at nearly 29%, outpacing many competitors in the retail sector. Investors have been paying attention to the company’s strong revenue growth and a striking 42% year-over-year jump in net income, suggesting enhanced operational efficiency and potential for long-term profitability.

Despite some ups and downs in the stock price, including a recent pullback of about 5.9% over the past month, the broader momentum has generally been positive. This momentum has been supported by strong quarterly results and growing confidence in Coupang’s ability to expand its footprint both in Korea and abroad. These trends, along with recent reports of improved market conditions in e-commerce and logistics, have brought Coupang back into the spotlight as a growth story with real financial traction.

Now, when we dig into valuation, the company currently scores a 2 out of 6 in our undervaluation checks. That means, by several traditional metrics, Coupang is undervalued in two out of the six key areas analysts look at. But as with all stocks, there are nuances that can help you see whether it is worth your hard-earned cash. Next, we will break down the main ways investors analyze Coupang’s value and share why there is an even better approach to understanding what this stock could be worth.

Coupang delivered 25.7% returns over the last year. See how this stacks up to the rest of the Multiline Retail industry.Approach 1: Coupang Cash Flows

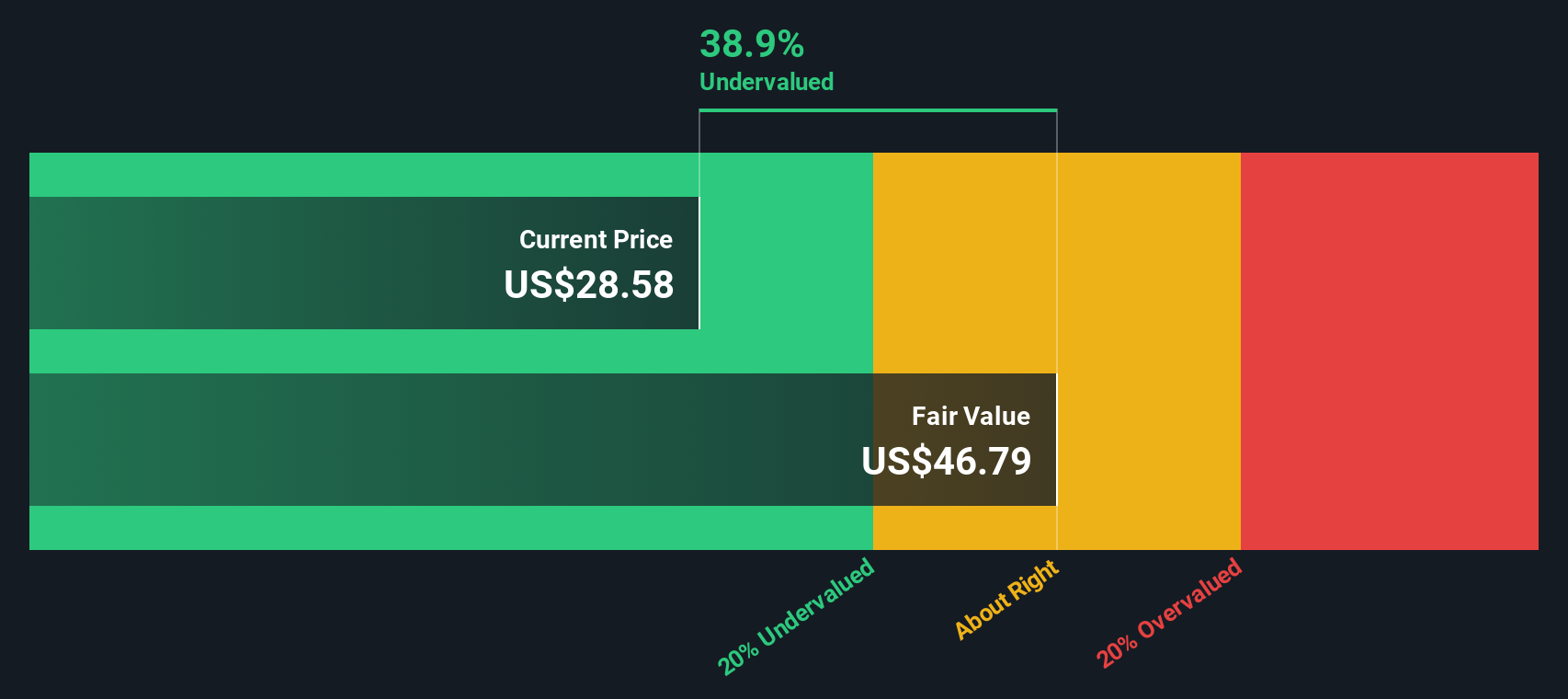

A Discounted Cash Flow (DCF) model is a popular method investors use to estimate a company's true value by projecting its future cash flows and then discounting them back to today’s dollars. This approach examines how much cash a business can generate in the future, making it a useful tool for reducing uncertainty in valuation.

For Coupang, the latest numbers show Free Cash Flow (FCF) at $833 million. Looking ahead, analysts forecast the FCF will climb to roughly $6.7 billion by 2035, with the path to reach this level featuring steady year-by-year growth. This pattern of expanding cash generation is an important part of the company’s long-term story and growth narrative.

Based on these projections, the DCF calculation estimates a fair value of $46.94 per share. In comparison to the market, this suggests Coupang is 38.7% undervalued. According to this model, the stock may offer an opportunity for those who prefer investing with a margin of safety.

Result: UNDERVALUED

Approach 2: Coupang Price vs Earnings

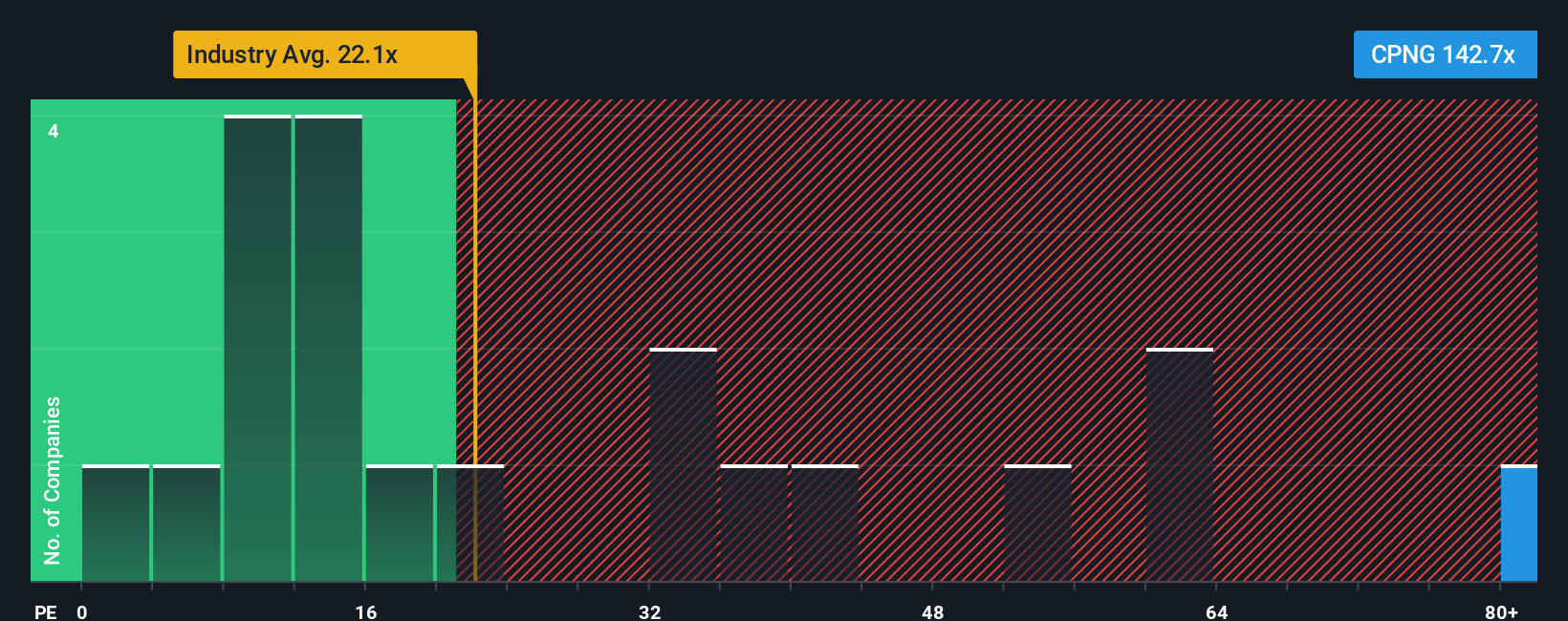

The Price-to-Earnings (PE) ratio is a widely used valuation metric and is particularly effective for profitable companies like Coupang. This ratio helps investors compare the price of a stock to its actual earnings, giving a sense of how much the market is willing to pay for each dollar of profit. Importantly, higher growth expectations and lower risk tend to justify higher PE ratios. In contrast, slower growth or elevated risk usually mean lower PE multiples are appropriate.

Coupang currently trades at a PE ratio of 143.6x, which is significantly higher than both the Multiline Retail industry average of 22.8x and the average for its peers at 26.1x. This premium suggests that investors are anticipating strong earnings growth ahead, or are assigning a higher quality or lower-risk assessment to Coupang compared to its competitors.

To offer a more nuanced perspective, Simply Wall St calculates a Fair PE Ratio for Coupang based on factors such as the company’s earnings growth, industry trends, profit margins, market cap, and specific risks. For Coupang, the Fair Ratio stands at 47.5x. When we compare this with the actual PE ratio, the stock trades at a substantial premium to what would typically be justified by its financial profile and risk factors.

Result: OVERVALUED

Upgrade Your Decision Making: Choose your Coupang Narrative

Beyond ratios and models, investment "Narratives" are a straightforward way to explain your perspective on a company. They link the company's big-picture story—your outlook on its future revenue, earnings, and margins—with the numbers, creating a forecast and an estimated fair value grounded in your unique view.

With Narratives, Simply Wall St makes this process accessible for everyone. Millions of investors use Narratives to build and refine their forecasts, compare different stories and outcomes, and debate what a stock could be worth based on updated data, news, and earnings.

When you create or follow a Narrative, you see how the story you believe in ties directly to an up-to-date fair value. This makes it easy to compare that value against Coupang's current share price and make informed decisions about buying or selling.

Narratives are updated dynamically as new information arrives, so your valuation adapts automatically to things like fresh earnings or industry news. This helps keep your decisions relevant in real time.

For Coupang, for example, one investor’s Narrative might assume aggressive revenue growth and a fair value as high as $39.00 per share. Another might price in slower growth and higher risk, leading to a more cautious fair value of $26.20 per share.

For Coupang, here are previews of two leading Coupang Narratives: 🐂 Coupang Bull Case- Fair Value: $33.99

- Current price is 15.4% below this narrative’s target (undervalued)

- Projected revenue growth: 12.6%

- Technology-led efficiency, expanding margins, and rapid geographic growth position Coupang for potential long-term earnings expansion.

- Operational leverage is anticipated from automation and AI, supported by strong customer spend and successful expansion in Taiwan, reinforcing bullish views.

- Risks include challenges in scaling, elevated expenses, and high dependence on the Korean market, but consensus still points to a higher future fair value.

- Fair Value: $27.25

- Current price is 5.5% above this narrative’s target (overvalued)

- Projected revenue growth: 12%

- Profitability remains inconsistent despite strong revenue growth, and operational risks such as labor issues and new acquisitions impact the outlook.

- Intense competition from both domestic and international players, especially new ventures from Alibaba, may affect market share.

- There is real growth potential for risk-tolerant investors, but volatility, regulatory issues, and expansion risks should be monitored closely for the next 1 to 3 years.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CPNG

Coupang

Owns and operates retail business through its mobile applications and internet websites in South Korea and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Gaxos.ai: Early-Stage AI Innovator in Gaming & Health

Fair Value US$2.21|6.3% undervalued

JO

Community Contributor

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value US$500.00|0.9% overvalued

PI

Community Contributor

Amazon's Future Rises as Stock Price Falls: A Long-Term Investment Vision

Fair Value US$234.75|2.9% undervalued

ZW

Community Contributor