Advertisement

ContextLogic Inc. (NASDAQ:WISH) and the Problems With Cheap User Acquisition

ContextLogic Inc. (NASDAQ:WISH) has gained a lot of attention recently, and investors are split between thinking that the company has high potential based on gross margins and revenue, and those who are concerned that the bottom has yet to be reached. In this article we will look at the performance, predictions as well as take a look at expenses and see why the market might have such a divergent view on the company.

On a quick side note, ContextLogic's Vice President of Operations, Thomas Chuang resigned on the 17th August, and the resignation was published on the 23rd August.

Performance & Estimates

The company announced quarter-to-date total revenue through July 2021 was down approximately 40% compared with the prior quarter, while Marketplace revenue was down approximately 55% compared to the same period. With the pullback in digital ad spending, The company expects third quarter revenue to decline further.

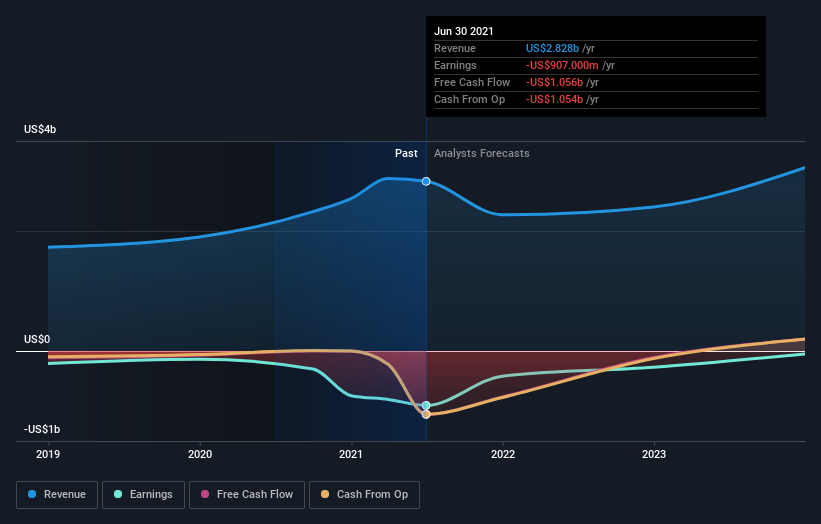

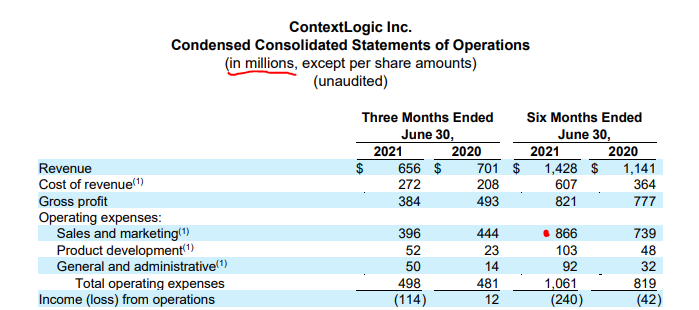

ContextLogic Inc. reported earnings results for the second quarter and six months ended June 30, 2021. For the quarter, revenue of $656 million compared to $701 million a year ago.

Loss from operations was $114 million compared to income from operations $12 million a year ago.

Net loss was $111 million, compared to $11 million a year ago.

Analysts have decreased the price target to US$9.83, down from US$17.10. The current price target is an average from 11 analysts and is 47% above last closing price of US$6.69.

View our latest analysis for ContextLogic

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

ContextLogic is well known by investors, and plenty of analysts have tried to predict the future profit levels. You can see what analysts are predicting for ContextLogic in this interactive graph of future profit estimates.

Notable Business Expenses

Now that we have the fundamentals, let's take a dive into ContextLogic's expenses and see what they might reveal about the future and business model.

Normally, when you see a young growth company, you expect a large portion of business expenses to go towards sales and marketing. With time, these expenses should result in growth of the company and provide a solid foundation for the future.

In the case of ContextLogic, the goal of a marketing campaign would be that it attracts clients, makes them buy products and offer them a platform where they become repeat buyers. If these criteria are not met, the marketing campaign is mostly wasted. Just imagine spending close to a Billion USD, just so your platform is known to many people, but on average they make one purchase and never visit again. Purchases do not create value, unless the client is satisfied with the product and buys again.

Looking at the figure above, it seems that the company is investing all of its gross profit plus some more into marketing. However, our ttm revenue growth chart above, show that sales is declining, even on the back of the pandemic, which was a positive catalyst for many e-commerce businesses. Even the sheer percentage of marketing spend, suggests that management is trying hard to acquire new users.

In their latest report, ContextLogic defines this clearly: "Our model relies on cost-effectively adding new users, converting those users into buyers and improving engagement and monetization of those buyers on Wish over time...".

From the outside, in the past few quarters, it looked like the company was steadily growing, but investors might be faced with the prospect of it being "cheap growth", or growth at the expense of margins and costly marketing campaigns.

If we turn and look at buyer statistics (page 22), we see that LTM (Last Twelve Months) Active Users declined to 50 million in Q2 2021 vs the 70 million in Q2 2020. These are the users that have bought at least 1 product in the last 12 months.

The numbers suggest stagnation at best - if we write off the pandemic effect as a booster to sales. But the 22% decrease in buyers is indicative of a weak marketing strategy, or simply, an unpleasant shopping experience for consumers. It is interesting to note, that management offers no substantial explanation to the drop in LTM Active Users, and presents is as "primarily driven by lower monthly active users and reduced conversion".

Conclusion

A lot of investors seem to have lost money investing in ContextLogic, and we desire to caution our readers that people with vested interests in a stock going up, may present opinions that tend to selectively focus on revenue growth, draw parallels between WISH, Amazon, JD, Alibaba, Dollar General, and overfocus on the yearly sales to price. We need to remember that stocks are forward-looking, and do our best to estimate what is left of the company after the cash has been burnt away from marketing and other expenses.

Companies can only flash their application so many times in the form of ads, before users decide if it is worth their while and memorable. In the case of ContextLogic, it is hard to make that case.

We've identified 2 fundamental warning signs with ContextLogic, and understanding them should be part of your investment process.

We will like ContextLogic better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About OTCPK:LOGC

Flawless balance sheet minimal.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor