- United States

- /

- General Merchandise and Department Stores

- /

- NasdaqGS:AMZN

Amazon.com (NasdaqGS:AMZN) Eyes TikTok Acquisition Amid Weekly Price Drop Of 11%

Reviewed by Simply Wall St

Amazon.com (NasdaqGS:AMZN) recently captured headlines with a controversial bid to acquire TikTok amid heightened scrutiny from U.S. regulators, reflecting its push for strategic growth. Meanwhile, significant market turmoil marked by a 9% weekly plunge in the Nasdaq was influenced by a global trade war spurred by newly announced tariffs by the U.S. administration. The simultaneous bid and market instability provided a backdrop for Amazon's share price drop of 11% this past week, as investors grappled with broader economic fears and the company's ambitious acquisition strategies amidst pending regulatory challenges.

Buy, Hold or Sell Amazon.com? View our complete analysis and fair value estimate and you decide.

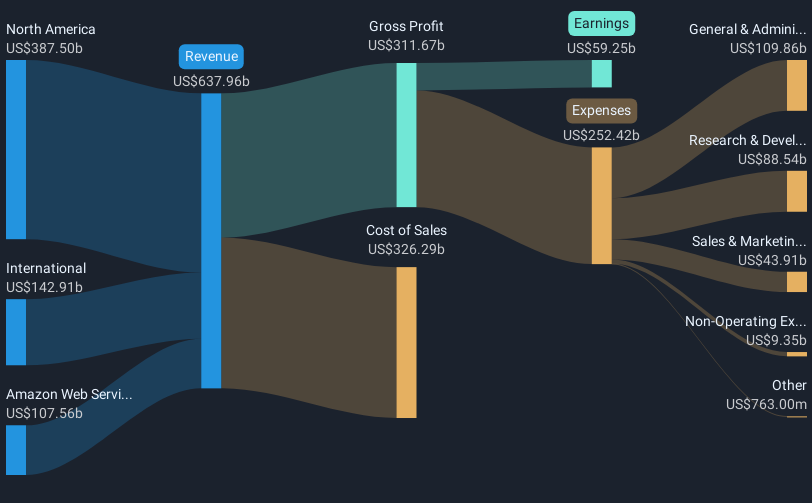

Amazon.com has posted a total return of 67.42% over the past five years, a period marked by significant operational and strategic developments. Notable progress was made in the cloud and retail domains, especially through investments in fulfillment automation and enhancements in AI-driven AWS, which have strengthened its profitability prospects. Amazon's strong performance in advertising also played a crucial role in expanding margins with a revenue run rate surpassing US$69 billion. However, foreign exchange fluctuations have intermittently stressed margins, evidenced by a US$700 million higher headwind than anticipated.

Regulatory and legal challenges have also been part of Amazon's narrative. A June 2023 FTC complaint accused Amazon of manipulative user-interface practices, impacting consumer relations. Labor issues, such as ongoing strikes demanding better working conditions and union recognition, further complicated its operational landscape. Despite these complexities, Amazon's earnings have grown considerably, with a 22.6% annual increase over the past five years, underscoring resilience amid challenges. Despite underperforming the US Multiline Retail industry by 5.9% over the last year, Amazon continues to anticipate robust revenue streams from diversified efforts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:AMZN

Amazon.com

Engages in the retail sale of consumer products, advertising, and subscriptions service through online and physical stores in North America and internationally.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Community Narratives