Advertisement

- United States

- /

- Office REITs

- /

- NYSE:CUZ

Could Cousins Properties’ (CUZ) Sunbelt Focus Limit Its Edge in the AI Real Estate Boom?

Simply Wall St

Reviewed by Sasha Jovanovic

- Jefferies downgraded Cousins Properties to Hold in October 2025, pointing to limited gains from artificial intelligence-driven demand and moderating migration in its Sunbelt markets, after the company reported mixed second-quarter results and announced a third-quarter cash dividend.

- This shift highlights how concentrated geographic exposure and shifting industry trends can influence expectations for occupancy rates and long-term growth potential in the commercial property sector.

- We'll examine how concerns over Cousins Properties' limited exposure to artificial intelligence-driven real estate demand may impact its investment outlook.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Cousins Properties Investment Narrative Recap

To own shares of Cousins Properties, you have to believe in the continued success of its Sun Belt-focused office portfolio and confidence that migration and job growth in these markets will offset sector headwinds. Jefferies’ recent downgrade, pointing to slower artificial intelligence-driven demand and moderating migration, could weigh on short-term sentiment, but unless Sun Belt demand quickly deteriorates, the biggest catalyst remains sustained regional leasing, while the main risk lies in occupancy volatility due to migration shifts.

Of the company’s recent actions, the acquisition of The Link, a well-leased, long-term office property in Dallas, stands out as directly relevant, as it aims to strengthen the company’s presence in a core Sun Belt market and potentially reinforce portfolio quality despite sector-wide doubts. This move relates directly to Cousins’ ongoing strategy of focusing on premier assets in desirable metros, supporting the catalyst of market-leading occupancy and rent growth in its core areas.

However, in contrast to the stability offered by landmark acquisitions, investors should pay close attention to the risk of large tenant move-outs and the associated impact on revenue volatility…

Read the full narrative on Cousins Properties (it's free!)

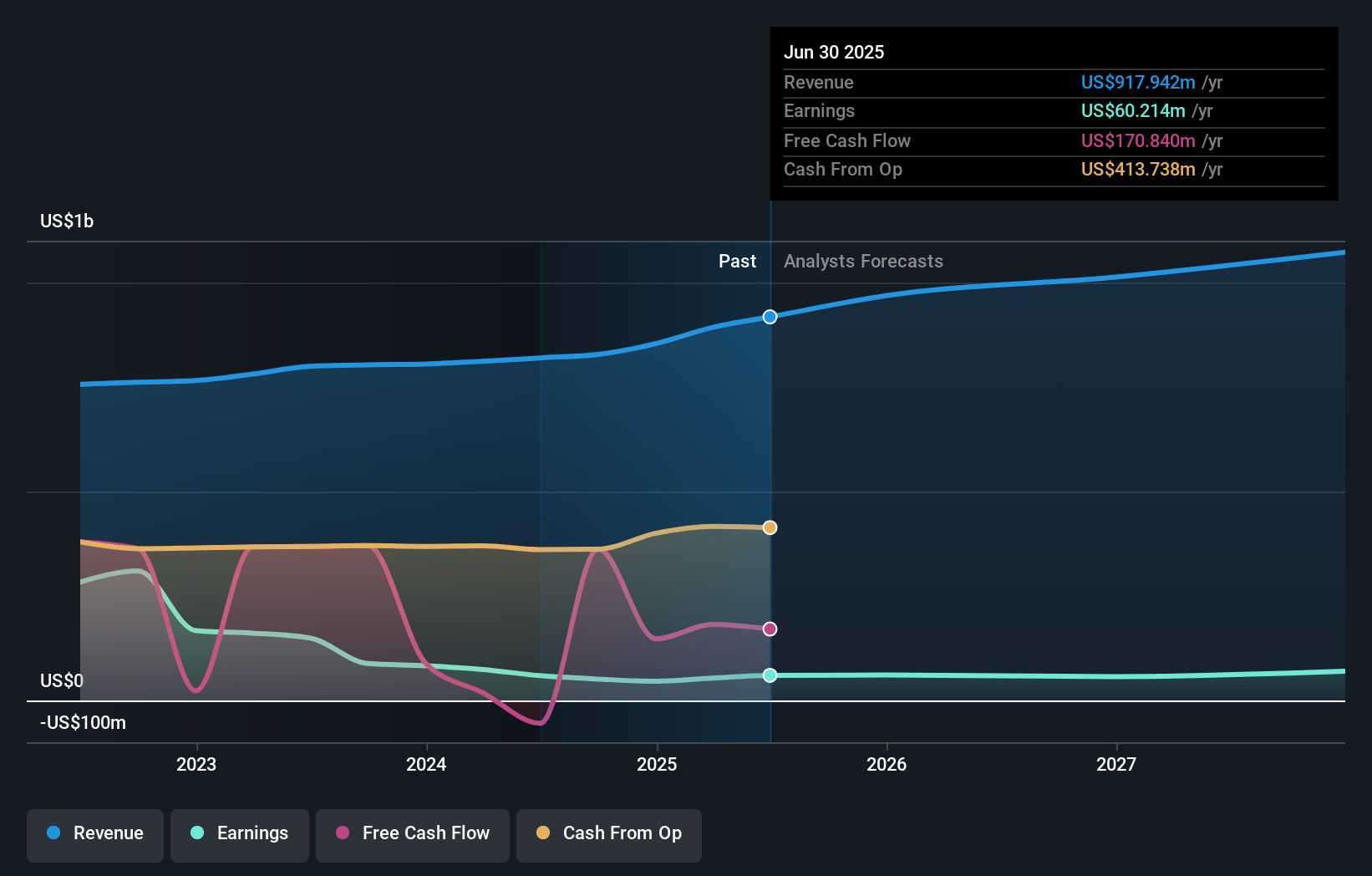

Cousins Properties' narrative projects $1.1 billion revenue and $65.7 million earnings by 2028. This requires 5.2% yearly revenue growth and a $5.5 million earnings increase from $60.2 million.

Uncover how Cousins Properties' forecasts yield a $32.83 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Two Community members estimate fair value for Cousins Properties between US$30.95 and US$32.83 per share. With margin pressure linked to shifting Sun Belt migration trends, these varied views underscore how much investor opinions can differ.

Explore 2 other fair value estimates on Cousins Properties - why the stock might be worth just $30.95!

Build Your Own Cousins Properties Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cousins Properties research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Cousins Properties research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cousins Properties' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CUZ

Cousins Properties

Cousins Properties is a fully integrated, self-administered and self-managed real estate investment trust (REIT).

Average dividend payer with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|4.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|39.4% undervalued

TR

Community Contributor