Advertisement

- United States

- /

- Biotech

- /

- NasdaqGM:CRVS

Companies Like Corvus Pharmaceuticals (NASDAQ:CRVS) Are In A Position To Invest In Growth

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So, the natural question for Corvus Pharmaceuticals (NASDAQ:CRVS) shareholders is whether they should be concerned by its rate of cash burn. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. Let's start with an examination of the business' cash, relative to its cash burn.

View our latest analysis for Corvus Pharmaceuticals

How Long Is Corvus Pharmaceuticals' Cash Runway?

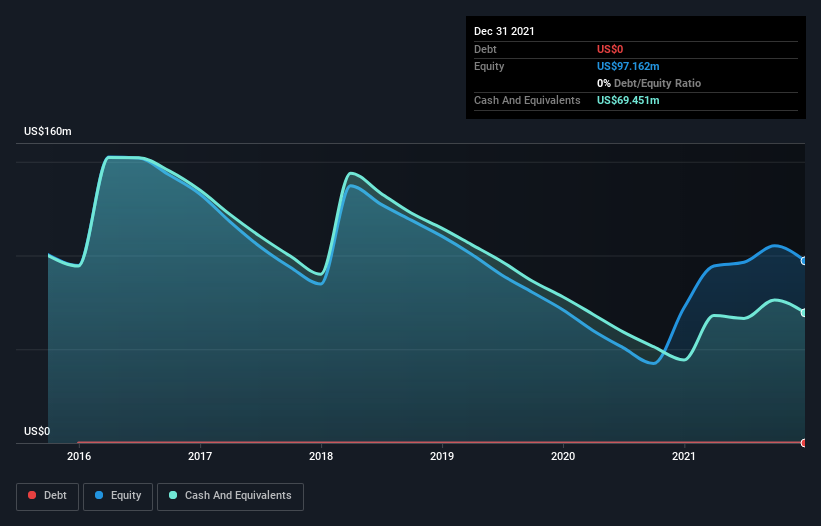

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. As at December 2021, Corvus Pharmaceuticals had cash of US$69m and no debt. In the last year, its cash burn was US$37m. Therefore, from December 2021 it had roughly 23 months of cash runway. Notably, however, analysts think that Corvus Pharmaceuticals will break even (at a free cash flow level) before then. If that happens, then the length of its cash runway, today, would become a moot point. You can see how its cash balance has changed over time in the image below.

How Is Corvus Pharmaceuticals' Cash Burn Changing Over Time?

Because Corvus Pharmaceuticals isn't currently generating revenue, we consider it an early-stage business. Nonetheless, we can still examine its cash burn trajectory as part of our assessment of its cash burn situation. Over the last year its cash burn actually increased by 5.4%, which suggests that management are increasing investment in future growth, but not too quickly. However, the company's true cash runway will therefore be shorter than suggested above, if spending continues to increase. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Easily Can Corvus Pharmaceuticals Raise Cash?

Since its cash burn is increasing (albeit only slightly), Corvus Pharmaceuticals shareholders should still be mindful of the possibility it will require more cash in the future. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Many companies end up issuing new shares to fund future growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of US$95m, Corvus Pharmaceuticals' US$37m in cash burn equates to about 39% of its market value. That's not insignificant, and if the company had to sell enough shares to fund another year's growth at the current share price, you'd likely witness fairly costly dilution.

So, Should We Worry About Corvus Pharmaceuticals' Cash Burn?

As you can probably tell by now, we're not too worried about Corvus Pharmaceuticals' cash burn. In particular, we think its cash runway stands out as evidence that the company is well on top of its spending. While its cash burn relative to its market cap wasn't great, the other factors mentioned in this article more than make up for weakness on that measure. It's clearly very positive to see that analysts are forecasting the company will break even fairly soon. Looking at all the measures in this article, together, we're not worried about its rate of cash burn; the company seems well on top of its medium-term spending needs. Separately, we looked at different risks affecting the company and spotted 6 warning signs for Corvus Pharmaceuticals (of which 2 make us uncomfortable!) you should know about.

Of course Corvus Pharmaceuticals may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:CRVS

Corvus Pharmaceuticals

A clinical stage biopharmaceutical company, engages in the development of product candidates that precisely target proteins that are critical to immune cell maturation and function in the United States.

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.1% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.6% undervalued

RO

Community Contributor