- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:META

These Fundamentals Suggest Facebook, Inc. (NASDAQ:FB) may be Primed for a Bull Run

Sometimes a storm is a great moment to pause and reevaluate our thesis on a company. Facebook, Inc. (NASDAQ:FB) has been hit both by controversy leading to investigations, and stagnating growth in the developed markets. In cases like this, the fundamentals can provide a great basis for the long-term stability of the company, and we may be able to take advantage of the current confusion.

We cannot rule out the risk that the situation leads to permanent changes, but a fresh look may provide opportunity.

See our Fundamental Report for Facebook

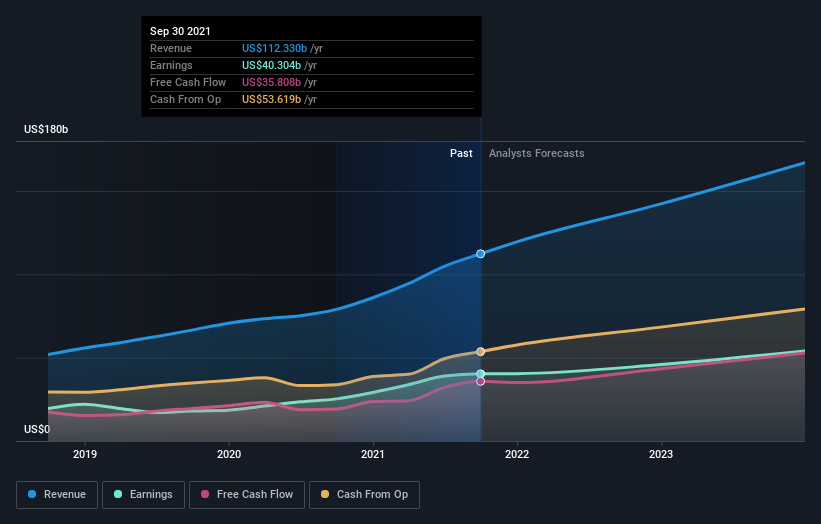

We first want to start with the future earnings potential of the company and get a good perspective of the income structure.

A good proxy for the future estimates can be provided by analysts that follow the company.

There are a few important things we discover from reviewing Facebook's past and future potential. The company's attractiveness comes from the high 36% profit margins, primarily resulting from their advertising revenue.

Second is the conversion of profits to cash flows - since investors can only be attributed free cash flows, we ultimately care about the cash making capacity of the company. In the case of Facebook, it has an accrual ratio of 0.06, which indicates that the company has some difficulty converting earnings into cash. On the long-term, this can be a leading indicator to stagnation in earnings.

Third is the future outlook. Analysts still see moderate to high revenue growth in the future. However, the company may find it difficult to convert the new revenue to higher profits, primarily because of competitors reducing the advertising power of Facebook, as well as the stabilized average revenue per user of US$10 worldwide.

The Price of Profits

For investors, it is important to evaluate if the market in correctly pricing these developments, or perhaps there is an overreaction to current events.

For an investment to make sense, Facebook must be able to provide enough free cash flows to investors. One way to assess the current level of cash vs the price of Facebook stock is by using the P/E proxy.

Facebook's Price to Earnings (P/E) ratio is 22.1x. Which simply means that it would take 22 years for investors to make a full return on their investment in Facebook stock, or if we treat the profits as dividends and assume a 50% payout ratio, Facebook would currently have an implied divided yield of 2.26%.

This means that, from a cash flows perspective, Facebook is still strong both as a growth and as a value investment. With earnings growth that's superior to most other companies of late, Facebook has been doing relatively well.

By comparing Facebook to peers, we see that the company is trading significantly lower than the peer group P/E of 37.7x, which may be a chance to get Facebook at a better price.

Want the full picture on analyst estimates for the company? Then our free report on Facebook will help you uncover what's on the horizon.

Is There Enough Growth For Facebook?

In order to justify its P/E ratio, Facebook would need to produce impressive growth in excess of the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 61% last year. EPS has also lifted 113% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 13% each year over the next three years. With the market predicted to deliver 12% growth each year, the company is positioned for a comparable earnings result.

Conclusion

Facebook's fundamentals are high enough to justify a deeper dive into the company. The market seems to be currently underpricing earnings, and even if somewhat stagnant, Facebook has enough growth and cash flows to justify a higher valuation.

If current events have short-term consequences, then the stock has high future potential.

The next step is to examine a valuation model for Facebook, and you can start with our Free Cash Flow to Equity Intrinsic Valuation model HERE.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NasdaqGS:META

Meta Platforms

Engages in the development of products that enable people to connect and share with friends and family through mobile devices, personal computers, virtual reality and mixed reality headsets, augmented reality, and wearables worldwide.

Outstanding track record and undervalued.

Similar Companies

Market Insights

Community Narratives