- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:BIDU

Baidu (NasdaqGS:BIDU) Expands Apollo Go To Dubai Testing Autonomous Services

Reviewed by Simply Wall St

Baidu (NasdaqGS:BIDU) has made headlines with its recent strategic cooperation with Dubai’s Roads and Transport Authority to launch autonomous driving services, marking the international expansion of its Apollo Go platform. Over the last quarter, the company's stock price increased by over 7%, a significant move considering the broader market trends, with the Nasdaq Composite seeing a decline during the same period. The strategic alignment in Dubai is a key development, showcasing Baidu’s ambition in autonomous transportation. Additionally, its advancements in AI technologies like the ERNIE models contributed to positive investor sentiment, reflecting in the stock's upward trajectory.

Buy, Hold or Sell Baidu? View our complete analysis and fair value estimate and you decide.

Find companies with promising cash flow potential yet trading below their fair value.

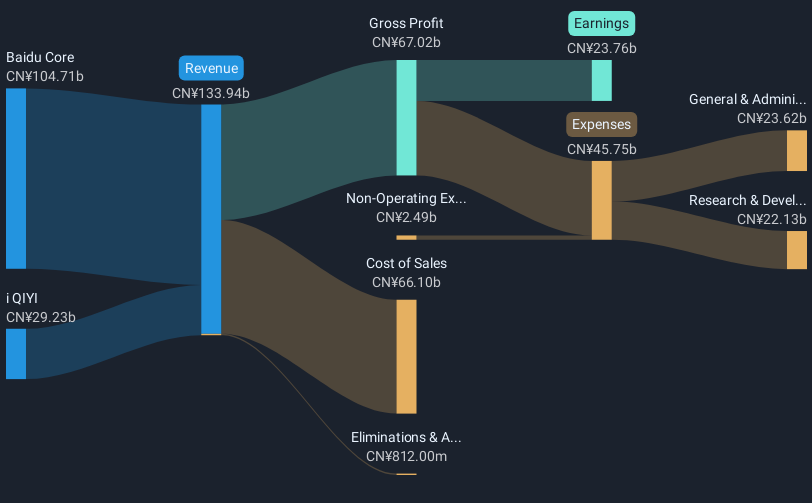

Despite short-term gains, Baidu's total shareholder return over the past five years was a decline of 3.94%, underscoring challenges that countered its recent achievements. This period witnessed competitive and regulatory hurdles in China's AI and autonomous driving sectors, impacting revenue streams, especially in Baidu's core online marketing segment, which saw a 7% year-over-year decline in Q4 2024. Additionally, while Baidu's AI Cloud showed strong growth, the significant costs of supporting these operations placed pressure on margins.

Throughout this timeframe, the company's strategic initiatives included launching new AI models like ERNIE 4.5 and expanding autonomous services internationally, such as the Dubai Apollo Go partnership. However, despite these efforts, Baidu underperformed its industry peers and the US market over the last year. Financial maneuvers, including debt financing amounting to CNY 10 billion and share buybacks totaling $356 million this quarter, have influenced shareholder returns but haven't reversed the longer-term decline.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Baidu might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:BIDU

Baidu

Provides online marketing and cloud services through an internet platform in the People’s Republic of China.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Community Narratives