- United States

- /

- Chemicals

- /

- NYSE:CE

Does Celanese’s 37% Slide in 2025 Create an Opportunity for Long Term Investors?

Reviewed by Bailey Pemberton

- If you have been wondering whether Celanese is a beaten down bargain or a value trap, this is exactly the kind of setup where a deeper valuation check can make a real difference to your returns.

- The stock has bounced 7.4% over the last week and 3.4% over the last month, but that is off a much lower base after a painful slide of around 37.5% year to date and 37.7% over the last year.

- Investors have been digesting a mix of macro headlines around demand for specialty materials and chemicals, plus ongoing debate about how rising input costs and global growth uncertainty could affect Celanese's margins and cash flows. At the same time, the market has been watching management's capital allocation decisions, including growth investments and balance sheet discipline, to gauge whether the current strategy can unlock long term value.

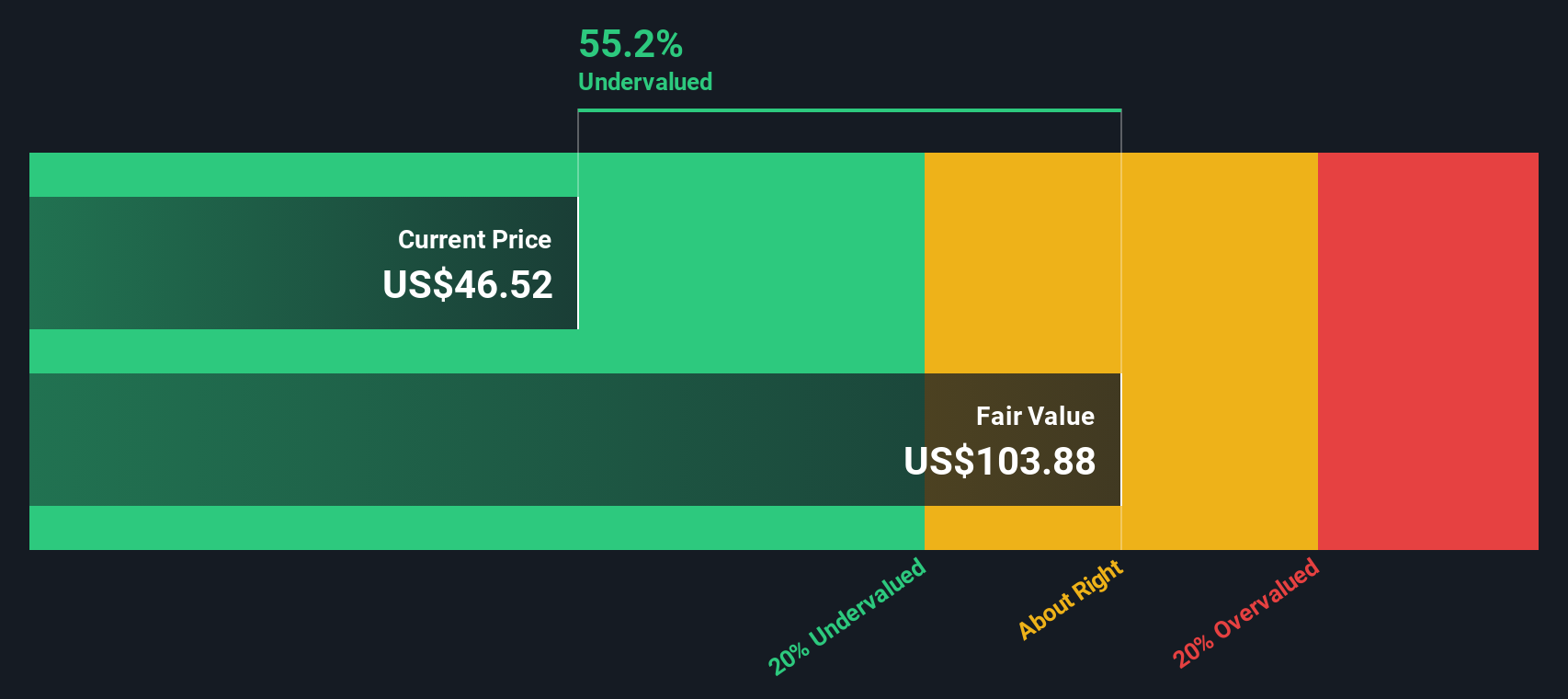

- Despite the rough share price history, Celanese currently scores a 5/6 valuation check for being undervalued on our framework. That makes it worth unpacking how different valuation methods line up and, later on, exploring an even better way to connect those numbers to the real investment story.

Find out why Celanese's -37.7% return over the last year is lagging behind its peers.

Approach 1: Celanese Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes the cash Celanese is expected to generate in the future, then discounts those projections back to today to estimate what the business is worth right now. In this case, Simply Wall St uses a 2 Stage Free Cash Flow to Equity approach, starting with analyst forecasts and then extending them further out.

Celanese generated about $946.6 Million in free cash flow over the last twelve months, and analysts expect this to rise to around $987.35 Million by 2027. Beyond the explicit analyst horizon, cash flows are extrapolated out to 2035, with projections gradually climbing toward roughly $1.22 Billion. These future cash flows are then discounted to arrive at an estimated intrinsic value of about $90.02 per share.

With the DCF suggesting the shares are trading at roughly a 52.5% discount to this fair value estimate, the model points to Celanese appearing meaningfully undervalued at current levels.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Celanese is undervalued by 52.5%. Track this in your watchlist or portfolio, or discover 904 more undervalued stocks based on cash flows.

Approach 2: Celanese Price vs Sales

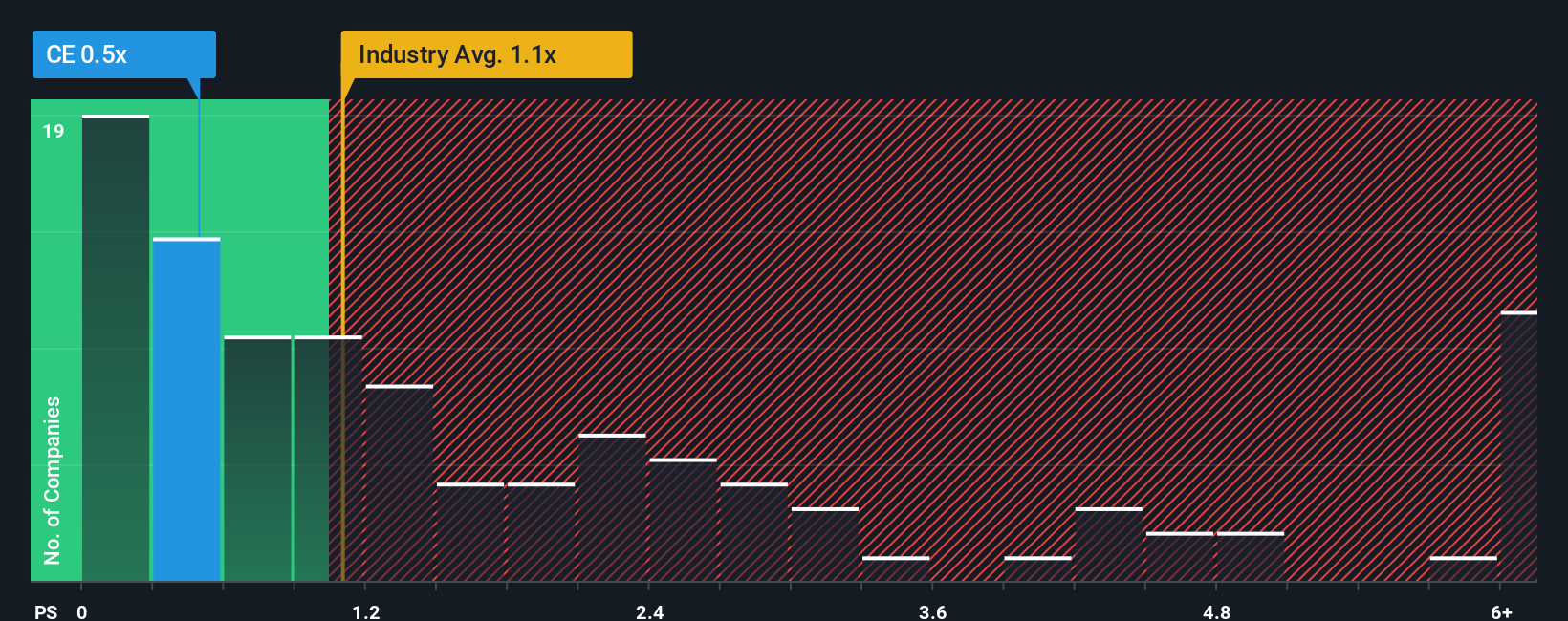

For companies like Celanese, where revenues are a key driver and earnings can be more cyclical or noisy, the price to sales multiple is a useful way to gauge what the market is paying for each dollar of revenue. It helps strip out some of the short term accounting swings and focuses on the underlying scale of the business.

In general, higher growth and lower risk justify a richer multiple, while slower growth or more uncertainty should mean a lower, or discounted, price to sales ratio. Celanese currently trades on a price to sales multiple of about 0.48x, which is well below both the wider Chemicals industry average of around 1.18x and the peer group average of roughly 2.80x.

Simply Wall St also uses a proprietary Fair Ratio, which estimates what price to sales multiple a company like Celanese should trade on, after accounting for its growth outlook, profitability, risk profile, industry and market cap. This is more tailored than a simple peer or industry comparison, which can be skewed by outliers. Celanese’s Fair Ratio is approximately 1.00x, comfortably above the current 0.48x, which indicates that, on this metric, the shares still screen as undervalued.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1447 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Celanese Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to attach your own story about Celanese to the numbers you think are realistic for its future revenues, earnings, margins and fair value.

A Narrative is your investment thesis written out as a clear storyline, then translated into a financial forecast that connects what you believe about the business to a specific fair value estimate, rather than relying only on static multiples or someone else’s assumptions.

On Simply Wall St, millions of investors build and share Narratives on the Community page, where the platform turns each story into a set of projected financials and a fair value, and then compares that Fair Value to the current share price to help you decide whether Celanese looks like a buy, a hold or a sell.

Narratives also stay live and dynamic, automatically updating when new information such as earnings, news about low carbon materials or changes in analyst forecasts comes in. This means a bullish Celanese Narrative that leans toward the 100.0 price target and a cautious one closer to 40.0 can both be tracked and compared in real time as the facts evolve.

Do you think there's more to the story for Celanese? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CE

Celanese

A chemical and specialty materials company, manufactures and sells engineered polymers worldwide.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion