Advertisement

- United States

- /

- Insurance

- /

- NasdaqGS:ROOT

Could Lower Rates Shift Root's (ROOT) Risk Profile or Reinforce Its Long-Term Business Model?

Reviewed by Sasha Jovanovic

- Shares of digital auto insurance provider Root rose following Federal Reserve President John Williams' recent comments suggesting potential near-term interest rate cuts as the central bank considers moving towards a less restrictive policy stance.

- This shift can provide financial firms like Root with increased flexibility and potential gains from their investment portfolios as interest rates decline.

- We'll explore how increased expectations for interest rate cuts could affect Root's investment narrative regarding its business outlook and risk profile.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Root Investment Narrative Recap

To be a Root shareholder, you need to believe that the company’s technology-first approach in auto insurance, including its rapid deployment of AI-powered underwriting and expansion into new states, will drive profitable policy growth despite tough competition and changing economic conditions. The recent jump in shares, following Fed comments on lower rates, offers some short-term optimism for Root’s investment portfolio flexibility but does not materially change the biggest near-term catalyst, continued customer acquisition and margin improvement, or address the key risk of market share pressure from larger digital competitors.

Root’s announcement of its Washington State expansion in September 2025 is particularly relevant, supporting the company’s drive to grow its national footprint and improve scale, a factor that could be more meaningful as industry conditions evolve in response to shifting interest rate expectations.

On the other hand, investors should also be aware of how pressure from deeper-pocketed competitors in digital insurance could...

Read the full narrative on Root (it's free!)

Root's outlook anticipates $1.9 billion in revenue and $72.3 million in earnings by 2028. This reflects a 10.8% annual revenue growth rate and a decrease of $9.3 million in earnings from the current $81.6 million.

Uncover how Root's forecasts yield a $124.40 fair value, a 65% upside to its current price.

Exploring Other Perspectives

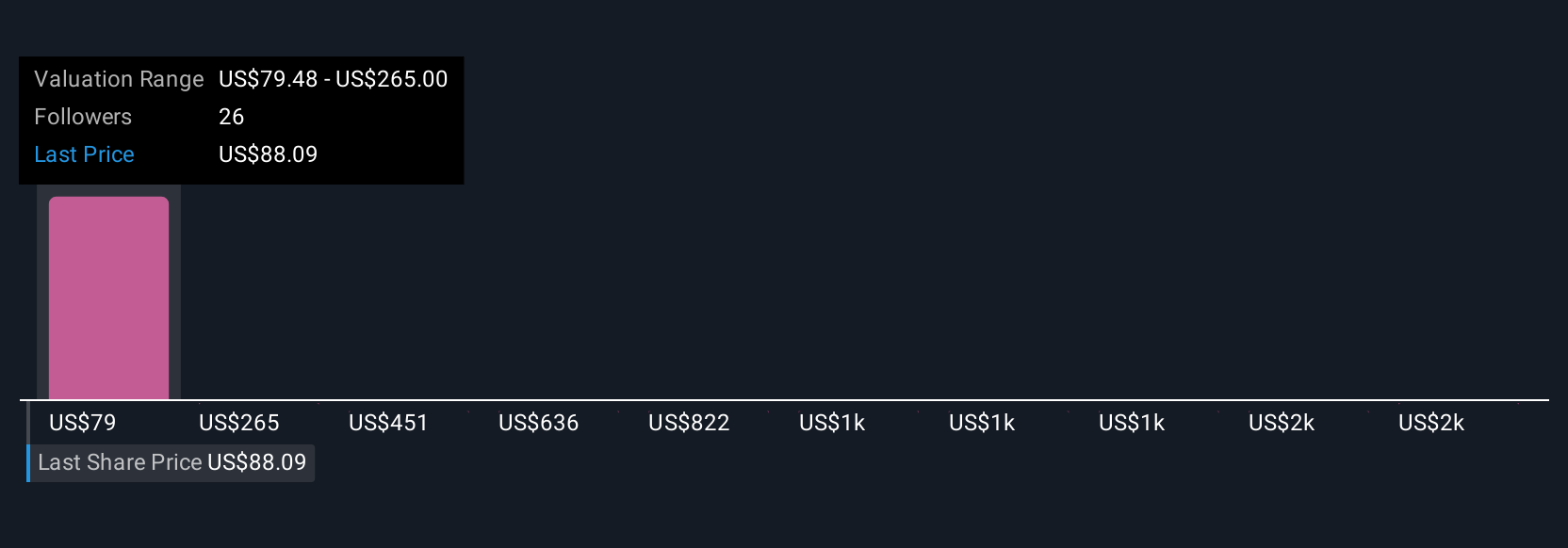

Fourteen individual fair value estimates from the Simply Wall St Community range widely from US$79.48 to US$1,934.69 per share, demonstrating striking variation. While many are optimistic, clear ongoing risks exist for Root’s direct channel growth as it faces stronger rivals with more resources, making it vital for investors to consider multiple viewpoints before forming any conclusions.

Explore 14 other fair value estimates on Root - why the stock might be worth just $79.48!

Build Your Own Root Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Root research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Root research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Root's overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ROOT

Root

Provides insurance products and services in the United States.

Excellent balance sheet with questionable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2535.8% undervalued

146 followersusers have followed this narrative

0 commentsusers have commented on this narrative

26 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0332.6% undervalued

31 followersusers have followed this narrative

3 commentsusers have commented on this narrative

10 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.521.1% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.726.3% undervalued

41 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Recently Updated Narratives

HU

Hunter_Z on Oriental Kopi Holdings Berhad ·

Oriental Kopi's Indonesia JV Strengthens Regional Growth Narrative

Fair Value:RM 1.533.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ST

StoxEurope on UCB ·

FV 206,24 but with a 310-154 range...to discuss

Fair Value:€206.249.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Figma ·

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value:US$22.3625.9% overvalued

62 followersusers have followed this narrative

7 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28021.7% undervalued

260 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9116.1% overvalued

128 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$202.6278.9% overvalued

139 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0