- United States

- /

- Healthcare Services

- /

- NYSE:HIMS

3 US Growth Companies With High Insider Ownership Seeing Up To 40% Earnings Growth

Reviewed by Simply Wall St

As the U.S. markets continue their upward momentum with the S&P 500 extending its winning streak, investors are increasingly focusing on growth companies that demonstrate strong potential for significant earnings increases. In this environment, stocks with high insider ownership often stand out as they can indicate confidence from those closest to the company's operations.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 24.1% |

| Victory Capital Holdings (NasdaqGS:VCTR) | 10.5% | 31.5% |

| Super Micro Computer (NasdaqGS:SMCI) | 14.4% | 24.3% |

| Duolingo (NasdaqGS:DUOL) | 14.6% | 41.6% |

| On Holding (NYSE:ONON) | 19.1% | 29.7% |

| Coastal Financial (NasdaqGS:CCB) | 18% | 46.1% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.8% | 95% |

| Alkami Technology (NasdaqGS:ALKT) | 11% | 98.6% |

| BBB Foods (NYSE:TBBB) | 22.9% | 50.7% |

Here's a peek at a few of the choices from the screener.

monday.com (NasdaqGS:MNDY)

Simply Wall St Growth Rating: ★★★★★☆

Overview: monday.com Ltd. develops software applications globally, serving regions such as the United States, Europe, the Middle East, Africa, and the United Kingdom, with a market cap of approximately $12.97 billion.

Operations: The company's revenue is primarily derived from its Internet Software & Services segment, totaling $906.59 million.

Insider Ownership: 15.4%

Earnings Growth Forecast: 40% p.a.

monday.com is experiencing robust growth, with revenue expected to increase by 20.9% annually, outpacing the US market. Recent expansions include a new Denver office to support growth and foster innovation. Despite a Q3 net loss of US$12.03 million, the company turned profitable over nine months with US$9.37 million in net income. With no significant insider trading activity recently and plans for strategic acquisitions, monday.com remains focused on long-term expansion and operational excellence under new leadership.

- Delve into the full analysis future growth report here for a deeper understanding of monday.com.

- The analysis detailed in our monday.com valuation report hints at an inflated share price compared to its estimated value.

Hims & Hers Health (NYSE:HIMS)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Hims & Hers Health, Inc. operates a telehealth platform connecting consumers with licensed healthcare professionals in the United States, the United Kingdom, and internationally, with a market cap of approximately $4.76 billion.

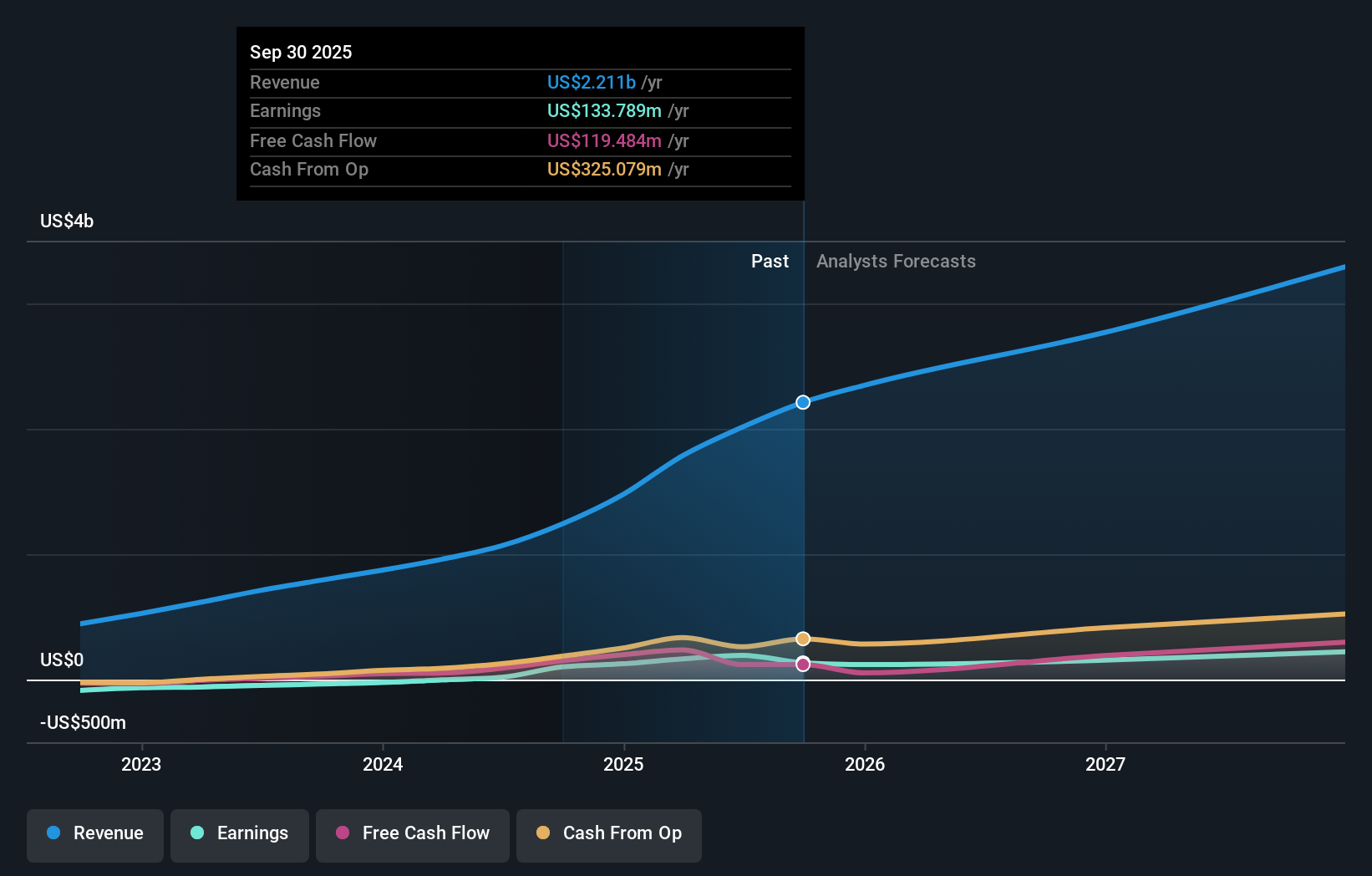

Operations: The company's revenue segment includes $1.24 billion from online retailers.

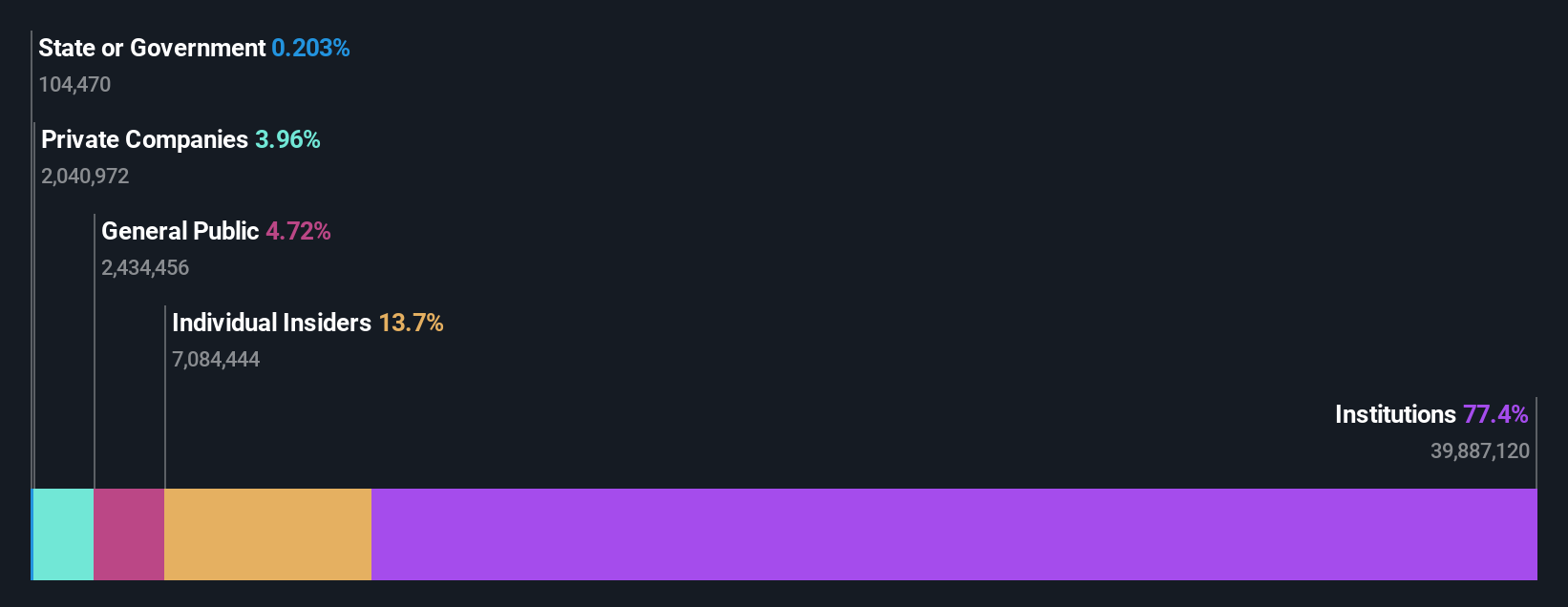

Insider Ownership: 13.4%

Earnings Growth Forecast: 17.2% p.a.

Hims & Hers Health is experiencing significant revenue growth, projected at 22.3% annually, surpassing the US market's average. Despite recent shareholder dilution, insider transactions show more buying than selling in the past quarter. The company has become profitable this year with a net income of US$75.59 million in Q3 2024 and is trading below its estimated fair value. Recent strategic moves include board enhancements and plans for acquisitions to bolster platform expansion.

- Get an in-depth perspective on Hims & Hers Health's performance by reading our analyst estimates report here.

- Our valuation report here indicates Hims & Hers Health may be undervalued.

TAL Education Group (NYSE:TAL)

Simply Wall St Growth Rating: ★★★★★☆

Overview: TAL Education Group offers K-12 after-school tutoring services in the People’s Republic of China and has a market cap of approximately $6.13 billion.

Operations: The company's revenue is primarily generated from its K-12 after-school tutoring services in China, amounting to $1.84 billion.

Insider Ownership: 31.7%

Earnings Growth Forecast: 36.1% p.a.

TAL Education Group has demonstrated strong financial performance, with significant revenue growth of US$1.03 billion for the first half of 2024 and a return to profitability. Earnings are projected to grow at 36.1% annually, outpacing the US market, while revenue is expected to rise by 21.4% per year. Despite high share price volatility and low forecasted return on equity, the stock trades below estimated fair value and has completed substantial buybacks worth $509.32 million since 2021.

- Dive into the specifics of TAL Education Group here with our thorough growth forecast report.

- Our valuation report unveils the possibility TAL Education Group's shares may be trading at a discount.

Next Steps

- Click through to start exploring the rest of the 205 Fast Growing US Companies With High Insider Ownership now.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Hims & Hers Health might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HIMS

Hims & Hers Health

Operates a telehealth platform that connects consumers to licensed healthcare professionals in the United States, the United Kingdom, and internationally.

Exceptional growth potential with flawless balance sheet.