April 2025's Leading Growth Companies With High Insider Ownership

Reviewed by Simply Wall St

As the U.S. stock market navigates a volatile landscape marked by new tariff announcements and economic uncertainties, investors are closely monitoring indices like the S&P 500 and Nasdaq Composite, which have recently experienced fluctuations. In this environment, growth companies with high insider ownership may offer unique insights into potential resilience and alignment of interests between company leaders and shareholders.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Super Micro Computer (NasdaqGS:SMCI) | 14.2% | 29.8% |

| Hims & Hers Health (NYSE:HIMS) | 13.2% | 21.8% |

| Duolingo (NasdaqGS:DUOL) | 14.4% | 37.1% |

| Coastal Financial (NasdaqGS:CCB) | 14.5% | 46.4% |

| Astera Labs (NasdaqGS:ALAB) | 15.9% | 61.3% |

| BBB Foods (NYSE:TBBB) | 16.2% | 41.1% |

| Clene (NasdaqCM:CLNN) | 19.5% | 63.1% |

| Upstart Holdings (NasdaqGS:UPST) | 12.7% | 100.1% |

| Enovix (NasdaqGS:ENVX) | 12.2% | 56.5% |

| Credit Acceptance (NasdaqGS:CACC) | 14.4% | 33.6% |

Here we highlight a subset of our preferred stocks from the screener.

LifeStance Health Group (NasdaqGS:LFST)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: LifeStance Health Group, Inc. operates through its subsidiaries to offer outpatient mental health services across various age groups in the United States, with a market cap of approximately $2.58 billion.

Operations: Revenue Segments (in millions of $): The company's revenue is primarily derived from Mental Health Services, totaling $1.25 billion.

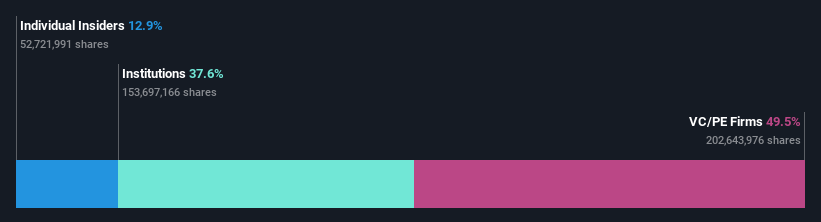

Insider Ownership: 12.9%

Revenue Growth Forecast: 13.1% p.a.

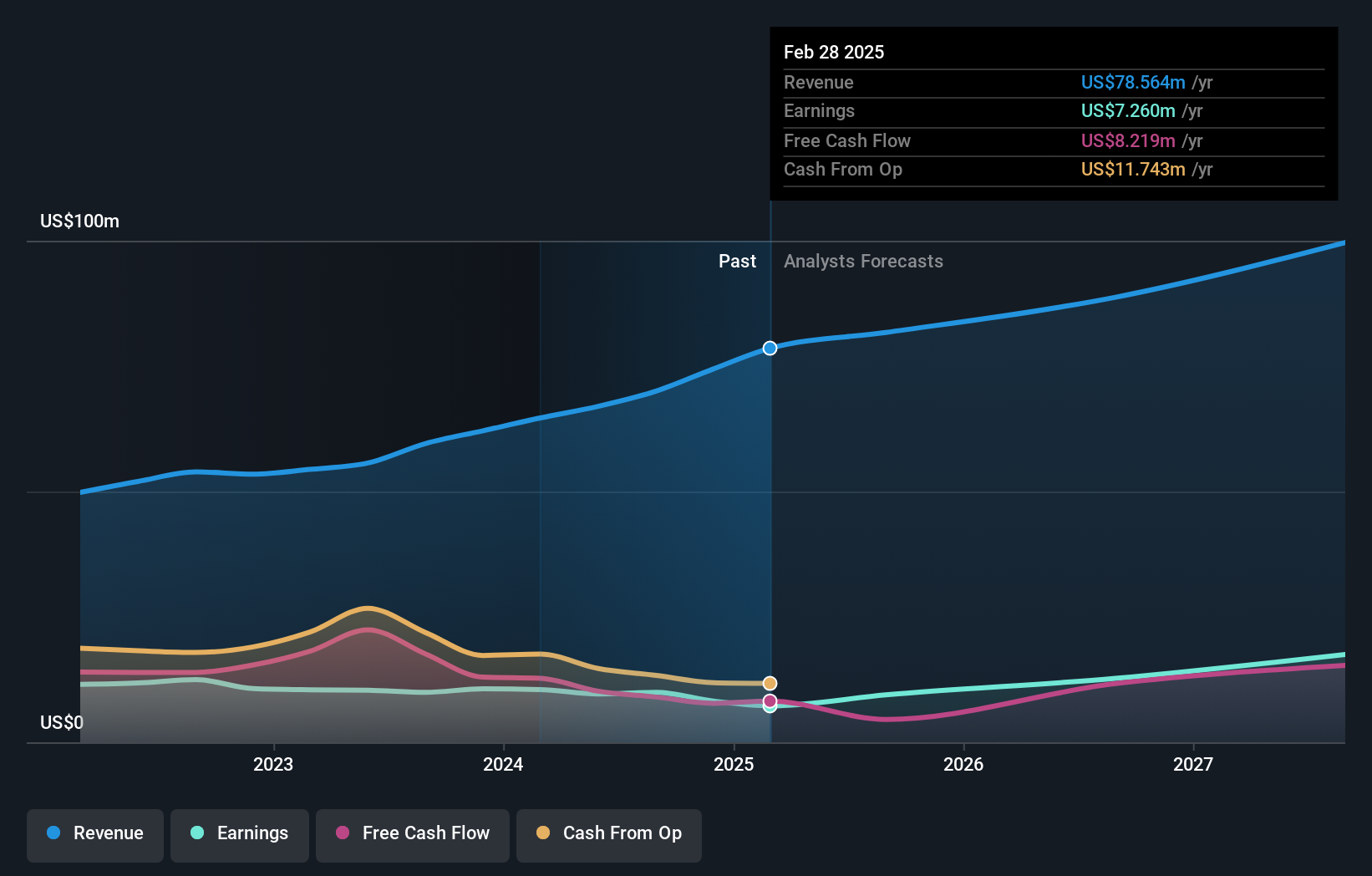

LifeStance Health Group is experiencing significant executive changes, with Dave Bourdon succeeding Ken Burdick as CEO. The company forecasts revenue growth of 13.1% annually, surpassing the US market's average. Despite recent insider selling, LifeStance remains attractive due to its expected profitability within three years and a stock price trading below analyst targets by 3.4%. Recent earnings show improved financial performance with reduced net losses and increased sales reaching US$1.25 billion for 2024.

- Click here to discover the nuances of LifeStance Health Group with our detailed analytical future growth report.

- The analysis detailed in our LifeStance Health Group valuation report hints at an deflated share price compared to its estimated value.

Simulations Plus (NasdaqGS:SLP)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Simulations Plus, Inc. develops drug discovery and development software using AI and machine learning for modeling, simulation, and molecular property prediction globally, with a market cap of $488.05 million.

Operations: The company's revenue is derived from two main segments: Services, contributing $30.29 million, and Software, generating $44.15 million.

Insider Ownership: 17.7%

Revenue Growth Forecast: 14.3% p.a.

Simulations Plus, Inc. has recently entered a strategic collaboration with the Enabling Technologies Consortium to enhance its GastroPlus platform, aiming to improve drug development and regulatory processes. Despite a decline in profit margins from 17.2% to 11%, the company forecasts significant earnings growth at 32.1% annually, outpacing the US market average of 13.8%. The stock is trading significantly below its estimated fair value, presenting potential upside for investors focused on growth opportunities in healthcare technology solutions.

- Click to explore a detailed breakdown of our findings in Simulations Plus' earnings growth report.

- In light of our recent valuation report, it seems possible that Simulations Plus is trading behind its estimated value.

MediaAlpha (NYSE:MAX)

Simply Wall St Growth Rating: ★★★★★☆

Overview: MediaAlpha, Inc. operates an insurance customer acquisition platform in the United States with a market cap of $626.73 million.

Operations: The company's revenue is primarily generated from its Internet Information Providers segment, which accounts for $864.70 million.

Insider Ownership: 13.9%

Revenue Growth Forecast: 10.9% p.a.

MediaAlpha has shown substantial growth, reporting US$864.7 million in sales for 2024, up from US$388.15 million the previous year, and achieving profitability with net income of US$16.63 million. The company's earnings are forecast to grow significantly at 24.72% annually over the next three years, surpassing market averages. Recent strategic appointments like Bradley Hunt to its Board and Keith Cramer as Chief Revenue Officer aim to bolster its growth trajectory despite high debt levels and large one-off items affecting financial results.

- Delve into the full analysis future growth report here for a deeper understanding of MediaAlpha.

- Upon reviewing our latest valuation report, MediaAlpha's share price might be too optimistic.

Key Takeaways

- Delve into our full catalog of 201 Fast Growing US Companies With High Insider Ownership here.

- Searching for a Fresh Perspective? Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

If you're looking to trade MediaAlpha, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MAX

MediaAlpha

Through its subsidiaries, operates an insurance customer acquisition platform in the United States.

High growth potential low.

Similar Companies

Market Insights

Community Narratives