- United States

- /

- Medical Equipment

- /

- NasdaqGS:DXCM

3 Stocks That May Be Trading Below Estimated Value In March 2025

Reviewed by Simply Wall St

As the U.S. stock market navigates a period of mixed performance, with major indices like the Dow Jones and S&P 500 experiencing fluctuations amid economic uncertainties and tariff concerns, investors are keenly observing potential opportunities that may arise from these volatile conditions. In this environment, identifying stocks that are trading below their estimated value can be crucial for those looking to capitalize on potential market inefficiencies while considering factors such as inflation projections and Federal Reserve policies.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | $30.91 | $61.74 | 49.9% |

| Dime Community Bancshares (NasdaqGS:DCOM) | $28.37 | $56.28 | 49.6% |

| Associated Banc-Corp (NYSE:ASB) | $22.83 | $44.95 | 49.2% |

| KBR (NYSE:KBR) | $51.30 | $101.72 | 49.6% |

| Datadog (NasdaqGS:DDOG) | $104.43 | $206.82 | 49.5% |

| Coastal Financial (NasdaqGS:CCB) | $84.44 | $167.69 | 49.6% |

| Viking Holdings (NYSE:VIK) | $40.09 | $78.93 | 49.2% |

| Gaotu Techedu (NYSE:GOTU) | $3.89 | $7.69 | 49.4% |

| Driven Brands Holdings (NasdaqGS:DRVN) | $17.56 | $34.82 | 49.6% |

| Mobileye Global (NasdaqGS:MBLY) | $14.54 | $28.81 | 49.5% |

Here's a peek at a few of the choices from the screener.

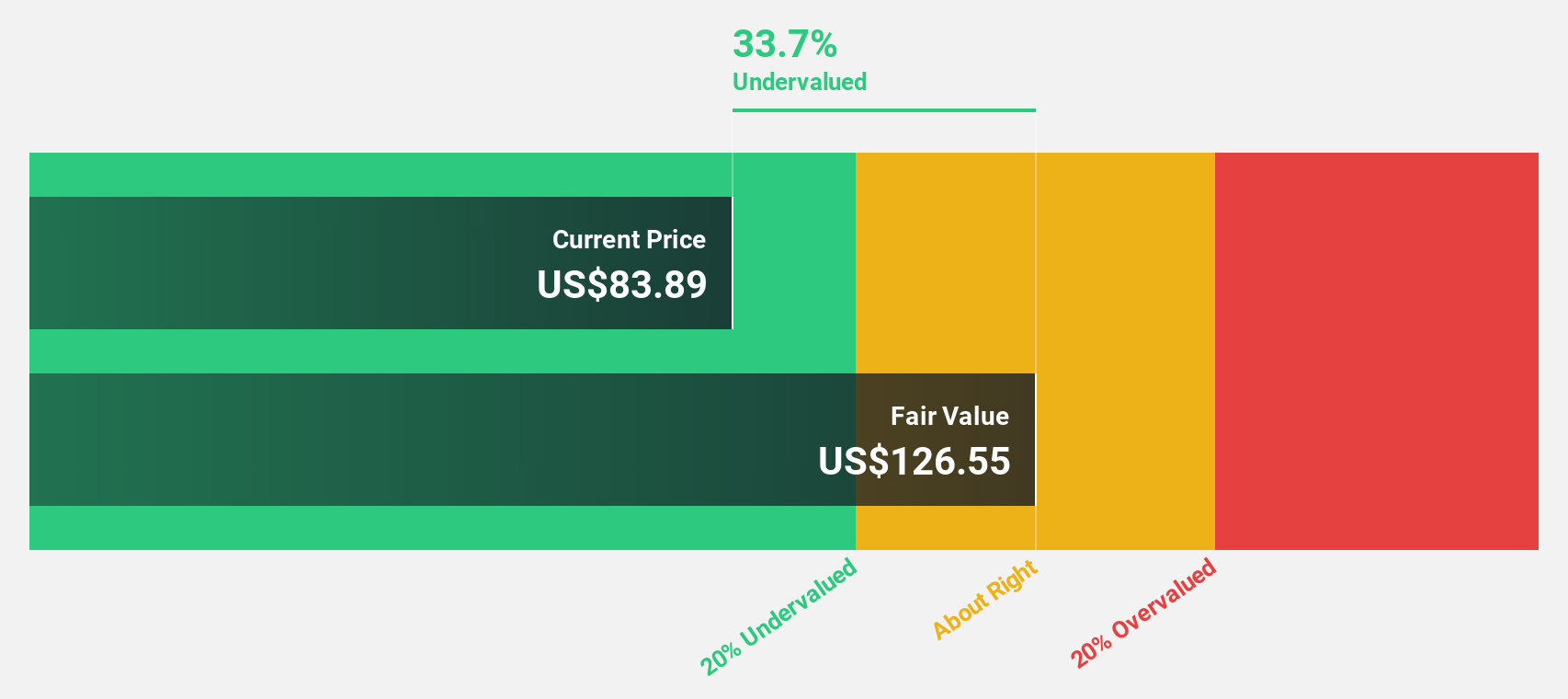

DexCom (NasdaqGS:DXCM)

Overview: DexCom, Inc. is a medical device company that specializes in designing, developing, and commercializing continuous glucose monitoring systems globally, with a market cap of approximately $27.63 billion.

Operations: The company's revenue is primarily derived from its Patient Monitoring Equipment segment, which generated $4.03 billion.

Estimated Discount To Fair Value: 35.5%

DexCom is trading 35.5% below its estimated fair value of US$113.71, suggesting it may be undervalued based on cash flows. Despite a recent FDA warning letter concerning manufacturing processes, the company continues to project robust growth with anticipated 2025 revenue of US$4.60 billion and earnings expected to grow at 19.1% annually, outpacing the broader market. The appointment of Renée Galá as a director could bolster strategic leadership amid these challenges.

- The analysis detailed in our DexCom growth report hints at robust future financial performance.

- Take a closer look at DexCom's balance sheet health here in our report.

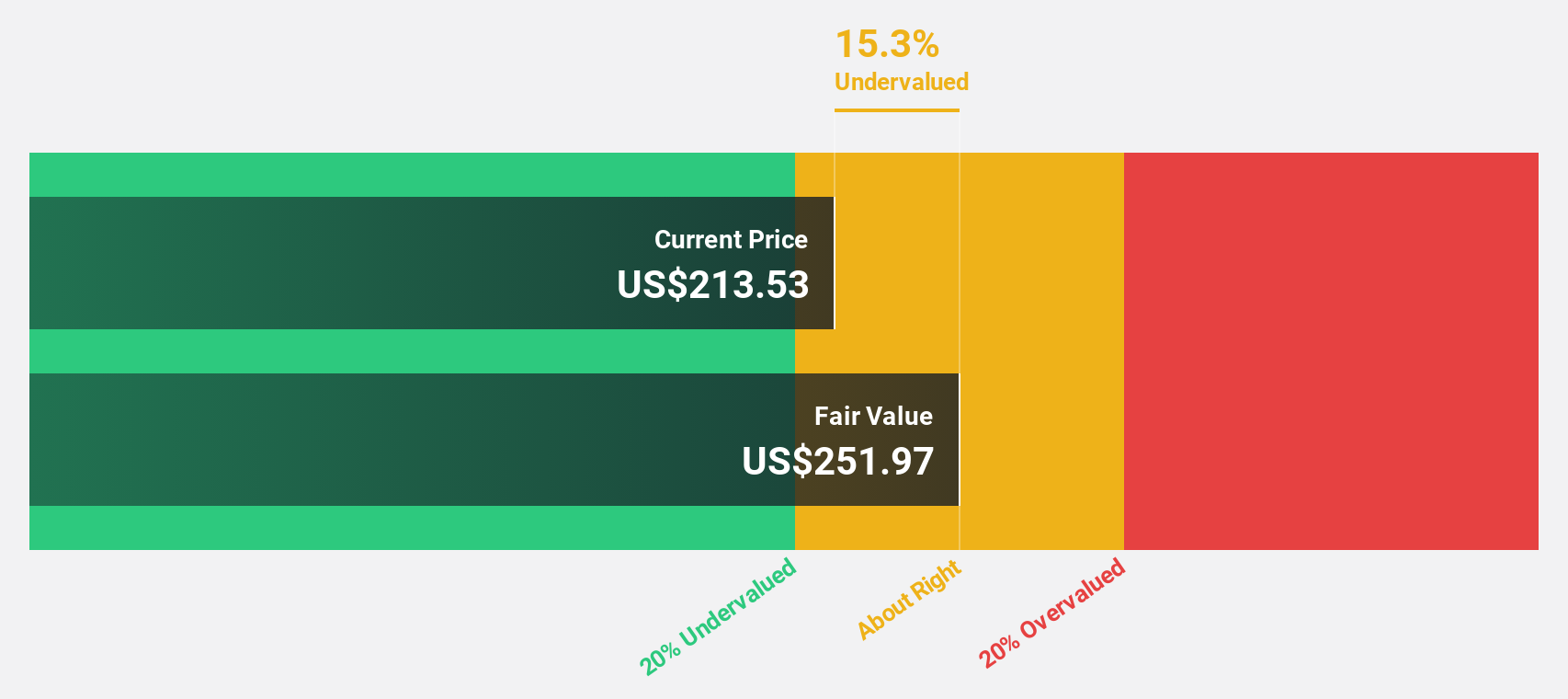

Atlassian (NasdaqGS:TEAM)

Overview: Atlassian Corporation, with a market cap of approximately $57.50 billion, designs, develops, licenses, and maintains various software products worldwide through its subsidiaries.

Operations: The company's revenue primarily stems from its Software & Programming segment, which generated approximately $4.79 billion.

Estimated Discount To Fair Value: 33.9%

Atlassian is trading at US$229.86, significantly below its estimated fair value of US$347.81, which highlights potential undervaluation based on cash flows. The company has shown consistent revenue growth, with recent quarterly earnings revealing a revenue increase to US$1.29 billion from the previous year's US$1.06 billion despite ongoing net losses. Analysts expect Atlassian to achieve profitability within three years, with anticipated high returns on equity and robust revenue growth surpassing market averages.

- Upon reviewing our latest growth report, Atlassian's projected financial performance appears quite optimistic.

- Click here and access our complete balance sheet health report to understand the dynamics of Atlassian.

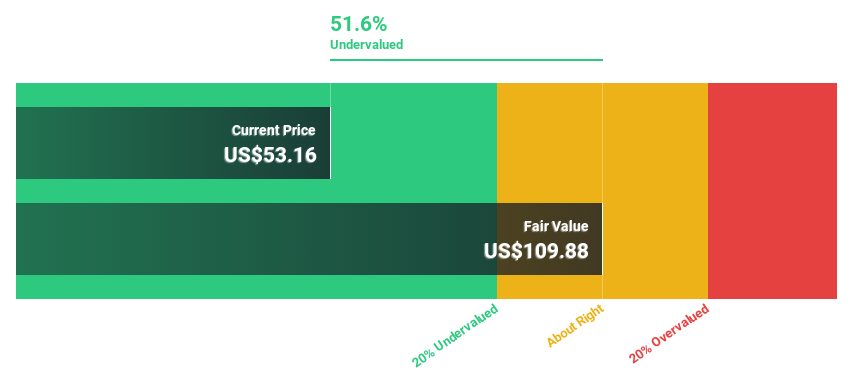

Smurfit Westrock (NYSE:SW)

Overview: Smurfit Westrock Plc, along with its subsidiaries, is involved in the manufacturing, distribution, and sale of containerboard, corrugated containers, and other paper-based packaging products with a market cap of $23.43 billion.

Operations: The company's revenue segments include North America at $10.09 billion, Latin America at $1.71 billion, and Europe, the Middle East and Africa, and Asia-Pacific collectively at $9.58 billion.

Estimated Discount To Fair Value: 48.9%

Smurfit Westrock, trading at US$46, is significantly undervalued with an estimated fair value of US$89.98. Despite recent insider selling and profit margins declining to 1.5% from 6.8%, the company forecasts strong earnings growth of 26% annually, outpacing the market average. However, its dividend yield of 3.75% isn't well-covered by free cash flows, and debt coverage by operating cash flow remains a concern amidst ongoing board changes and acquisition pursuits.

- According our earnings growth report, there's an indication that Smurfit Westrock might be ready to expand.

- Unlock comprehensive insights into our analysis of Smurfit Westrock stock in this financial health report.

Where To Now?

- Investigate our full lineup of 197 Undervalued US Stocks Based On Cash Flows right here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade DexCom, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DXCM

DexCom

A medical device company, focuses on the design, development, and commercialization of continuous glucose monitoring (CGM) systems in the United States and internationally.

Flawless balance sheet with reasonable growth potential.