Advertisement

- United States

- /

- Consumer Finance

- /

- NasdaqGS:UPST

Will Upstart's (UPST) New Credit Union Partnerships Offset Concerns About Cash Flow and Debt?

Simply Wall St

Reviewed by Sasha Jovanovic

- Upstart Holdings has recently expanded its lending network through new credit union partnerships and is drawing attention ahead of its scheduled earnings report, expected to show a very large increase in earnings per share compared to the same period last year.

- Despite Upstart's innovative AI-powered credit-scoring platform and growth partnerships, concerns remain about negative cash flow, high customer acquisition costs, and debt levels impacting its financial stability.

- We'll examine how rising optimism about Upstart's expected earnings jump and AI platform expansion shapes its current investment narrative.

These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Upstart Holdings Investment Narrative Recap

To see long-term value in Upstart Holdings, investors must believe in the company's ability to drive growth by expanding its AI-driven lending platform and forming more partnerships with credit unions. The recent buzz around an expected large earnings-per-share increase in the upcoming report stands as a potential short-term catalyst, but underlying issues like negative cash flow and sizable debt remain the key risks, and the latest news has not materially eased those concerns.

Upstart's recent partnerships with credit unions, such as Cornerstone Community Financial and ABNB Federal Credit Union, are directly relevant. These alliances are designed to broaden lending reach and reinforce Upstart's main growth catalysts ahead of the anticipated earnings surge.

However, beyond the current optimism around earnings, investors should be aware that Upstart's reliance on consistent model accuracy remains a major risk if...

Read the full narrative on Upstart Holdings (it's free!)

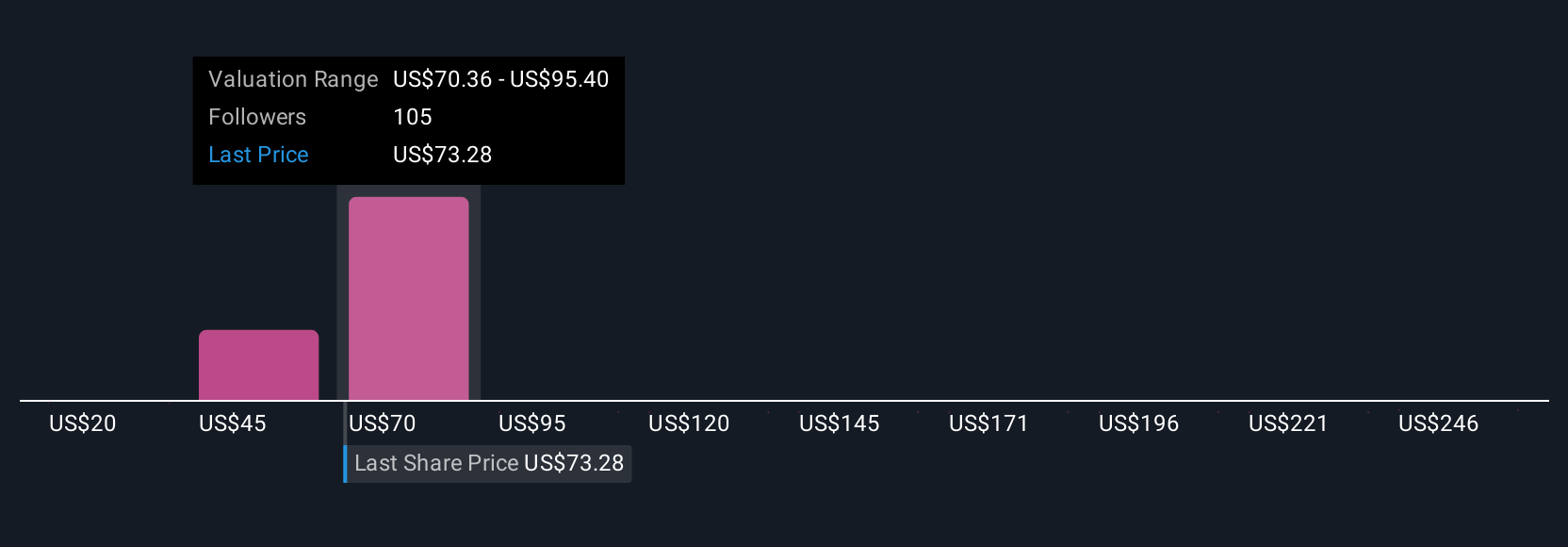

Upstart Holdings' narrative projects $1.8 billion in revenue and $337.2 million in earnings by 2028. This requires 27.2% yearly revenue growth and an earnings increase of $343.6 million from current earnings of -$6.4 million.

Uncover how Upstart Holdings' forecasts yield a $79.54 fair value, a 64% upside to its current price.

Exploring Other Perspectives

Seventeen Simply Wall St Community members estimate Upstart's fair value between US$21.91 and US$85 per share, with significantly differing outlooks. Against this backdrop, growing debate centers on whether Upstart's improved underwriting accuracy can offset risks from macroeconomic shifts and financial pressures.

Explore 17 other fair value estimates on Upstart Holdings - why the stock might be worth as much as 75% more than the current price!

Build Your Own Upstart Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Upstart Holdings research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free Upstart Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Upstart Holdings' overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:UPST

Upstart Holdings

Operates a cloud-based artificial intelligence (AI) lending platform in the United States.

Exceptional growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor