- United States

- /

- Consumer Finance

- /

- NasdaqGS:UPST

Upstart Holdings' (NASDAQ:UPST) Earnings Aren't Just Growing Quickly - They Are Of High Quality Too

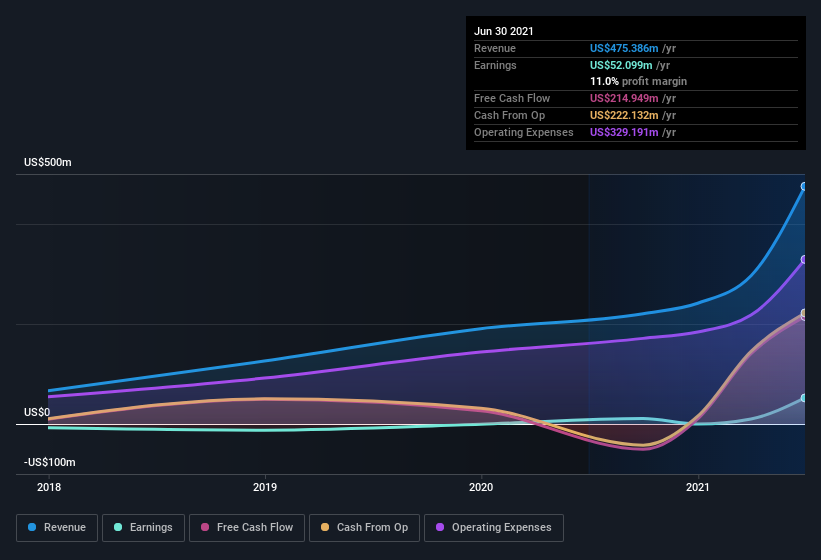

Upstart Holdings' ( NASDAQ:UPST ) second quarter results have been one of the highlights of the current earnings seasons. The company earned $0.62 a share, which was more than twice the expected $0.25 a share. Revenue for the quarter was $193.9 million, well ahead of consensus estimates that averaged $157 million.

Guidance for full year revenue was raised from $600 million to $750 million. Several other metrics including the operating margin, transaction volumes, and the conversion rate on requests also improved significantly.

Unsurprisingly, several analysts have raised their price targets and the stock price has risen more than 30% since earnings were released on Tuesday. We have done some analysis, and we found several positive factors beyond the profit numbers - in particular the quality of Upstart’s earnings.

View our latest analysis for Upstart Holdings

NasdaqGS:UPST Earnings and Revenue History August 12th 2021

A Closer Look at Upstart Holdings' Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio . The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. The ratio shows us how much a company's profit exceeds its FCF.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

Upstart Holdings has an accrual ratio of -0.79 for the year to June 2021. That implies it has very good cash conversion, and that its earnings in the last year actually significantly understate its free cash flow. Indeed, in the last twelve months it reported free cash flow of US$215m, well over the US$52.1m it reported in profit. Given that Upstart Holdings had negative free cash flow in the prior corresponding period, the trailing twelve-month result of US$215m would seem to be a step in the right direction.

Our Take on Upstart Holdings' Profit Performance

As we discussed above, Upstart Holdings' accrual ratio indicates strong conversion of profit to free cash flow, which is a positive for the company. Because of this, we think Upstart Holdings' underlying earnings potential is as good as, or possibly even better, than the statutory profit makes it seem! And on top of that, its earnings per share have grown at an extremely impressive rate over the last year. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider.

Now that we know that Upstart’s earnings are of high quality, the key factor to consider is likely revenue growth going forward. The stock is now trading on a P/E ratio of 157, which indicates that the market believes the growth trajectory will continue.

Upstart certainly has a compelling business model. The company uses artificial intelligence and demographic data, rather than credit scores, to evaluate the risk on loans. This gives Upstart and its partner banks access to an untapped market of potential borrowers. For the most part, Upstart acts as a sales channel for banks rather than providing the loans themselves. This means Upstart doesn’t need a large balance sheet like banks, which should in time lead to an attractive ROE too.

This is the third set of quarterly results Upstart has released since its IPO in December last year. So far the results have all been better than expected and appear to show the company is executing on its strategy successfully.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates. These estimates are likely to be raised in the next few days as analysts update their models.

This note has only looked at a single factor that sheds light on the nature of Upstart Holdings' profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity , or this list of stocks that insiders are buying to be useful.

If you're looking to trade Upstart Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.

About NasdaqGS:UPST

Upstart Holdings

Operates a cloud-based artificial intelligence (AI) lending platform in the United States.

Exceptional growth potential with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives