Advertisement

- United States

- /

- Consumer Finance

- /

- NasdaqGS:CACC

Does Credit Acceptance's (CACC) New Buyback Reveal Deeper Management Conviction or Limited Growth Options?

Simply Wall St

Reviewed by Sasha Jovanovic

- Credit Acceptance Corporation announced in late September 2025 that its Board of Directors has authorized a new share repurchase program, enabling the company to buy back up to 2,000,000 shares with no expiration date specified.

- This move may be interpreted as management’s confidence in the company’s long-term prospects and its commitment to returning value to shareholders.

- With the board’s latest share repurchase authorization, we’ll explore how this could impact Credit Acceptance’s investment narrative and future outlook.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Credit Acceptance Investment Narrative Recap

To be a shareholder in Credit Acceptance Corporation, you generally need conviction in the profitability and resilience of the U.S. subprime auto lending market, especially as revenue and earnings have recovered in the most recent quarters. The recent share repurchase program signals management’s confidence but does not materially shift the most pressing near-term catalysts or risks, such as further loan performance deterioration or market share losses amid ongoing competition.

The most relevant recent announcement is July’s completion of repurchasing over 1.6 million shares, reflecting the company’s ongoing commitment to shareholder returns. While this supports potential per-share earnings growth, it does not directly address credit risk in vintages from recent years, a key factor underpinning both the share price and broader investment outlook. Contrast this focus on buybacks with persistent concerns around loan performance from 2022–2024, which investors should not overlook, especially if...

Read the full narrative on Credit Acceptance (it's free!)

Credit Acceptance's narrative projects $4.5 billion revenue and $504.0 million earnings by 2028. This requires 56.2% yearly revenue growth and a $79.6 million earnings increase from $424.4 million today.

Uncover how Credit Acceptance's forecasts yield a $467.50 fair value, a 5% downside to its current price.

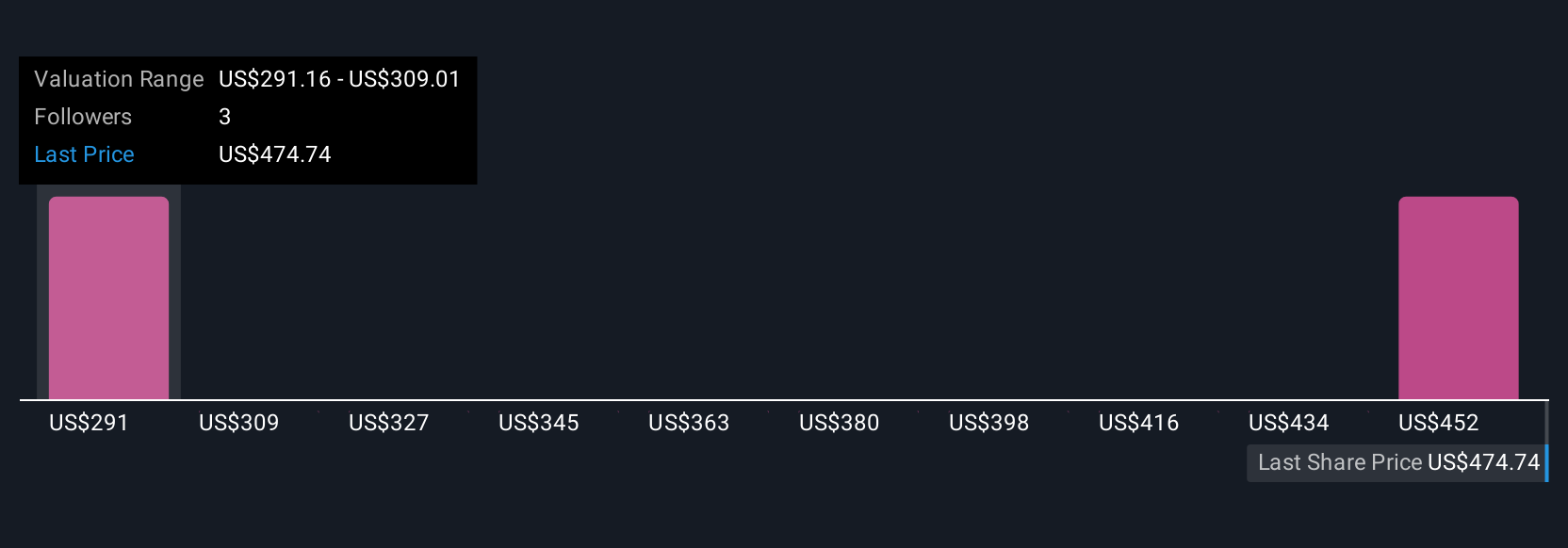

Exploring Other Perspectives

Fair value estimates for Credit Acceptance from three Simply Wall St Community members range widely from US$289.58 to US$469.67 per share. In light of these differing views, ongoing credit risks tied to recent loan vintages remain a crucial factor you should be aware of as they could shape future profitability and confidence in share repurchases.

Explore 3 other fair value estimates on Credit Acceptance - why the stock might be worth 41% less than the current price!

Build Your Own Credit Acceptance Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Credit Acceptance research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Credit Acceptance research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Credit Acceptance's overall financial health at a glance.

Contemplating Other Strategies?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CACC

Credit Acceptance

Engages in the provision of financing programs, and related products and services in the United States.

Proven track record with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|30.4% undervalued

MA

Community Contributor

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.0% undervalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|20.4% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor