Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:PLYA

Growth Investors: Industry Analysts Just Upgraded Their Playa Hotels & Resorts N.V. (NASDAQ:PLYA) Revenue Forecasts By 12%

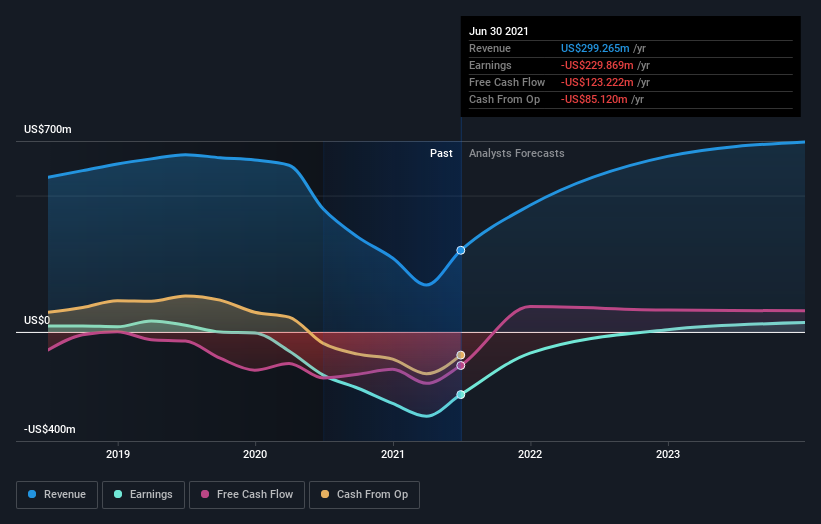

Celebrations may be in order for Playa Hotels & Resorts N.V. (NASDAQ:PLYA) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects.

After the upgrade, the six analysts covering Playa Hotels & Resorts are now predicting revenues of US$464m in 2021. If met, this would reflect a substantial 55% improvement in sales compared to the last 12 months. Before the latest update, the analysts were foreseeing US$416m of revenue in 2021. The consensus has definitely become more optimistic, showing a nice gain to revenue forecasts.

Check out our latest analysis for Playa Hotels & Resorts

We'd point out that there was no major changes to their price target of US$9.50, suggesting the latest estimates were not enough to shift their view on the value of the business. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic Playa Hotels & Resorts analyst has a price target of US$11.00 per share, while the most pessimistic values it at US$6.00. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Playa Hotels & Resorts' past performance and to peers in the same industry. For example, we noticed that Playa Hotels & Resorts' rate of growth is expected to accelerate meaningfully, with revenues forecast to exhibit 141% growth to the end of 2021 on an annualised basis. That is well above its historical decline of 7.9% a year over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 20% annually. So it looks like Playa Hotels & Resorts is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The highlight for us was that analysts increased their revenue forecasts for Playa Hotels & Resorts this year. Analysts also expect revenues to grow faster than the wider market. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at Playa Hotels & Resorts.

That's a pretty serious upgrade, but shareholders might be even more pleased to know that forecasts expect Playa Hotels & Resorts to be able to reach break-even within the next few years. For more information, you can click through to our free platform to learn more about these forecasts.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

When trading Playa Hotels & Resorts or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGS:PLYA

Playa Hotels & Resorts

Through its subsidiaries, owns, develops, and operates resorts in prime beachfront locations in Mexico and the Caribbean.

Slightly overvalued with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|29.6% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|49.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.4% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|54.5% undervalued

AX

Community Contributor