Advertisement

- United States

- /

- Machinery

- /

- NYSE:TNC

Undiscovered Gems in United States Stocks To Explore January 2025

Simply Wall St

Reviewed by Simply Wall St

Over the last 7 days, the United States market has experienced a 2.5% drop, yet it has shown resilience with a 22% rise over the past year and an optimistic forecast of 15% annual earnings growth. In this dynamic environment, identifying stocks that are not only poised for potential growth but also remain under the radar can offer intriguing opportunities for investors seeking to diversify their portfolios.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Eagle Financial Services | 170.75% | 12.30% | 1.92% | ★★★★★★ |

| Omega Flex | NA | 0.39% | 2.57% | ★★★★★★ |

| Franklin Financial Services | 173.21% | 5.55% | -1.86% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Morris State Bancshares | 10.20% | -0.28% | 6.97% | ★★★★★★ |

| Parker Drilling | 46.05% | 0.86% | 52.25% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.65% | 11.17% | ★★★★★★ |

| Teekay | NA | -3.71% | 60.91% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 7.11% | -35.88% | ★★★★★☆ |

| FRMO | 0.13% | 19.43% | 29.70% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

EZCORP (NasdaqGS:EZPW)

Simply Wall St Value Rating: ★★★★★☆

Overview: EZCORP, Inc. operates pawn services across the United States and Latin America, with a market capitalization of approximately $643.78 million.

Operations: EZCORP generates revenue primarily from its U.S. Pawn segment, contributing $836.08 million, and its Latin America Pawn segment, which adds $325.48 million.

EZCORP, a notable player in consumer finance, has demonstrated impressive earnings growth of 116% over the past year, surpassing industry averages. With a price-to-earnings ratio of 8x, it trades below the US market average of 18.1x, suggesting good value. The company’s net debt to equity ratio stands at 19.5%, indicating satisfactory debt management. Recent strategic moves include Latin American expansions and U.S. acquisitions aimed at boosting revenue streams alongside initiatives like EZ+ Rewards to enhance customer engagement. However, potential risks such as currency volatility and economic fluctuations could impact future stability despite current profitability and positive cash flow trends.

National Presto Industries (NYSE:NPK)

Simply Wall St Value Rating: ★★★★★★

Overview: National Presto Industries, Inc. operates in North America, offering a range of housewares and small appliances, defense, and safety products with a market cap of $676.45 million.

Operations: NPK's revenue primarily comes from its defense segment, generating $249.79 million, followed by housewares and small appliances at $100.84 million, and safety products contributing $1.33 million.

National Presto Industries, a nimble player in the market, showcases a debt-free status over the past five years, which likely contributes to its financial stability. Despite an 11% annual earnings drop over five years, recent performance indicates a turnaround with earnings surging by 44% last year. The company reported third-quarter sales of US$91.82 million and net income of US$8.08 million, reflecting solid growth from the previous year’s figures of US$83.14 million and US$7.02 million respectively. Trading at 23% below estimated fair value suggests potential for investors seeking undervalued opportunities in this sector.

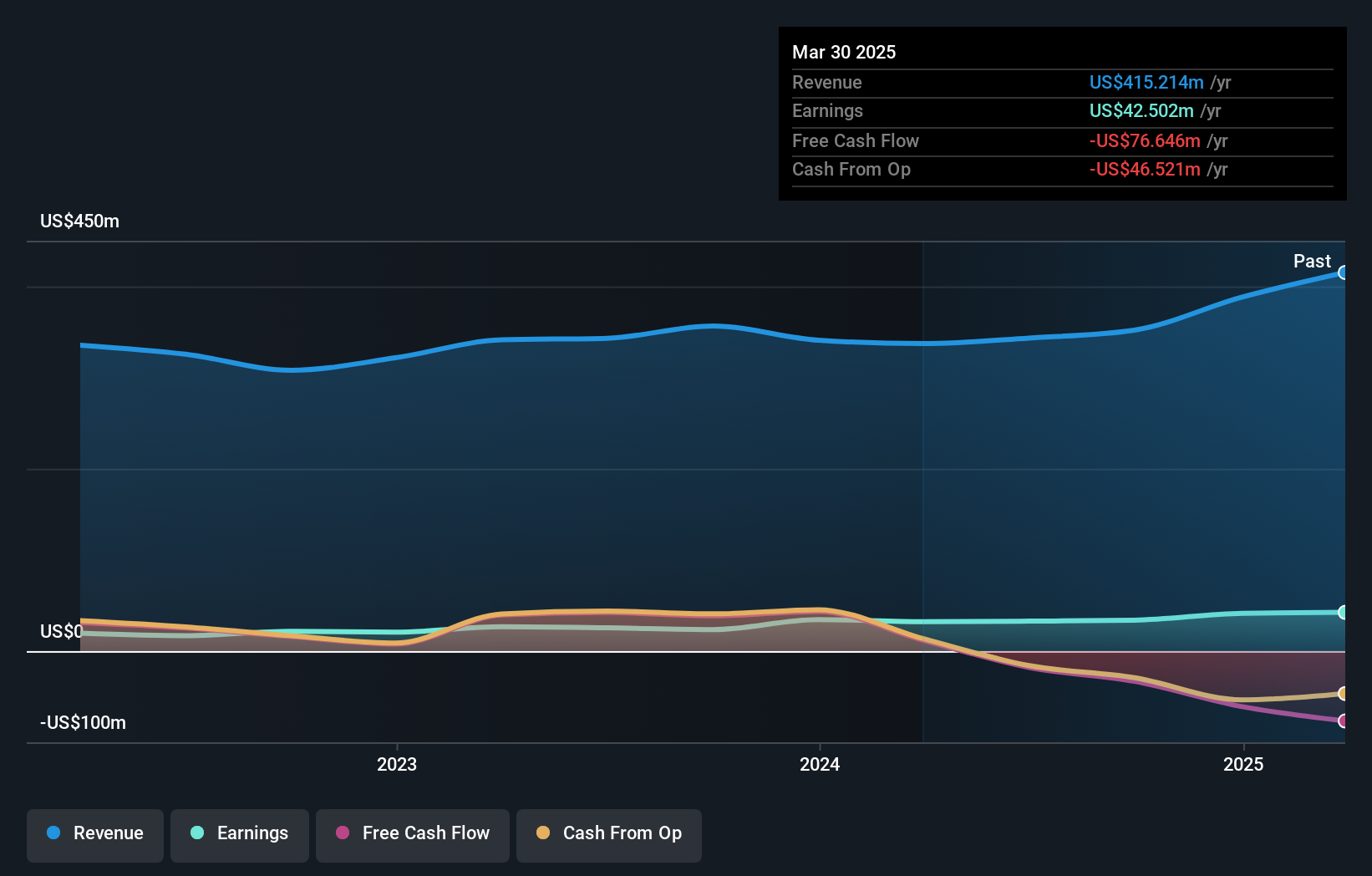

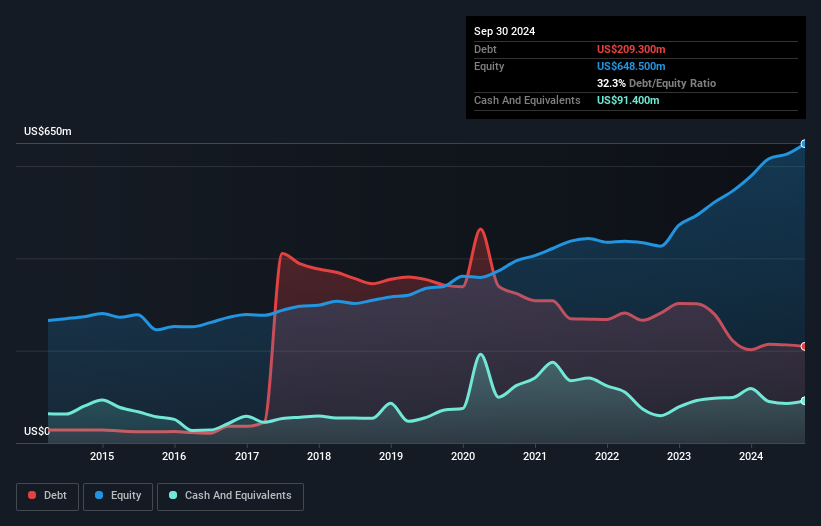

Tennant (NYSE:TNC)

Simply Wall St Value Rating: ★★★★★★

Overview: Tennant Company, along with its subsidiaries, specializes in the design, manufacture, and marketing of floor cleaning equipment across the Americas, Europe, the Middle East, Africa, and the Asia Pacific regions with a market cap of approximately $1.50 billion.

Operations: Tennant generates revenue primarily from the design, manufacture, and sale of products used in the maintenance of nonresidential surfaces, totaling approximately $1.27 billion.

Tennant, a nimble player in the machinery sector, has been making waves with its innovative lithium-ion battery-powered scrubbers like the T12 and T16 models. These enhancements align with their sustainability goals under the "Thriving People. Healthy Planet." framework. Financially, Tennant shows resilience; its debt to equity ratio impressively dropped from 100.7% to 32.3% over five years while maintaining satisfactory net debt levels at 18.2%. The company repurchased shares worth $31 million recently, signaling confidence in its valuation which trades at a good value compared to peers and industry standards.

Taking Advantage

- Click through to start exploring the rest of the 246 US Undiscovered Gems With Strong Fundamentals now.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tennant might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TNC

Tennant

Designs, manufactures, and markets floor cleaning equipment in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor