Last Update01 May 25Fair value Increased 1.90%

AnalystConsensusTarget made no meaningful changes to valuation assumptions.

Read more...Key Takeaways

- EZCORP's strategic expansion and innovation efforts are positioned to drive future revenue, earnings, and customer loyalty.

- Optimized inventory management and digital transformation are set to enhance operational efficiencies, supporting profit margin expansion despite recent contractions.

- Integration risks from expansion in Latin America combined with inventory and pricing pressures could challenge profit margins and cash flow efficiency.

Catalysts

About EZCORP- Provides pawn services in the United States and Latin America.

- EZCORP is leveraging its strengthened balance sheet to fund the expansion of its asset base through inorganic growth and new store developments, which is expected to drive future revenue and earnings.

- The company's focus on enhancing customer experience through technology and innovations, like the EZ+ Rewards program and expanded layaway options, aims at increasing customer loyalty and broadening engagement, potentially raising future revenue and net margins.

- Continued strong growth of earning assets, with a 22% year-over-year increase and significant PLO trajectory, indicates a robust pipeline for future revenue and earnings growth.

- Strategic moves to optimize inventory management and improve sales velocity are likely to positively impact gross profit margins and overall earnings, even with some margin contractions observed in recent quarters.

- The ongoing digital transformation, including increased online sales channels and a customer-centric approach, is expected to enhance operational efficiencies and support profit margin expansion over the long term.

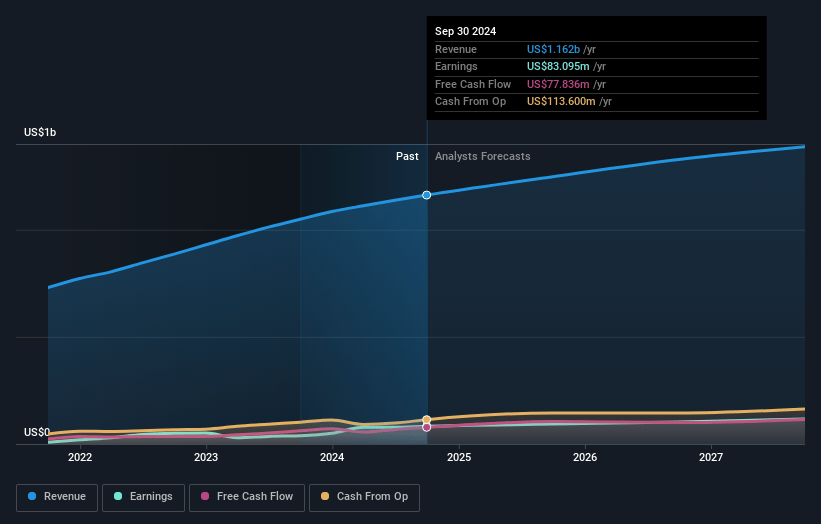

EZCORP Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming EZCORP's revenue will grow by 6.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.4% today to 8.4% in 3 years time.

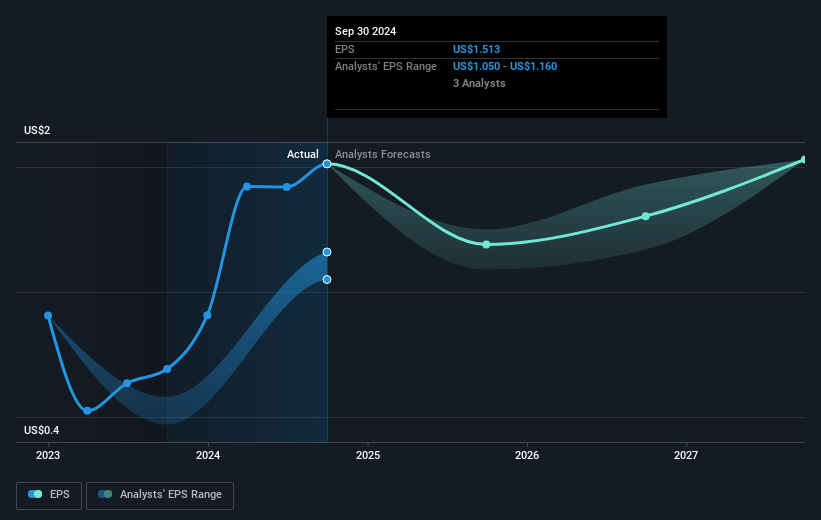

- Analysts expect earnings to reach $120.4 million (and earnings per share of $1.69) by about May 2028, up from $89.6 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.0x on those 2028 earnings, up from 9.8x today. This future PE is greater than the current PE for the US Consumer Finance industry at 10.0x.

- Analysts expect the number of shares outstanding to grow by 0.13% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.8%, as per the Simply Wall St company report.

EZCORP Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Increased price negotiations at the merchandise counter have led to a contraction in merchandise margin by 150 basis points, impacting gross profit margins.

- The company's expansion into Latin America through acquisitions and de novo stores could carry integration and operational risks, potentially affecting profit margins in that region.

- Inventory turnover rates have decreased, which might tie up capital and impact cash flow efficiency.

- There is potential pressure on inventory costs and sales margins from fluctuations in gold prices, which could impact financial results if not managed carefully.

- Mandatory lower interest rates on larger loans in states like Texas could lead to lower PLO yields, affecting revenue growth from pawn service charges.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $18.75 for EZCORP based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $24.0, and the most bearish reporting a price target of just $16.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.4 billion, earnings will come to $120.4 million, and it would be trading on a PE ratio of 11.0x, assuming you use a discount rate of 8.8%.

- Given the current share price of $15.93, the analyst price target of $18.75 is 15.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.