Advertisement

- United States

- /

- Banks

- /

- NYSEAM:BRBS

Should You Buy Blue Ridge Bankshares, Inc. (NYSEMKT:BRBS) For Its Upcoming Dividend?

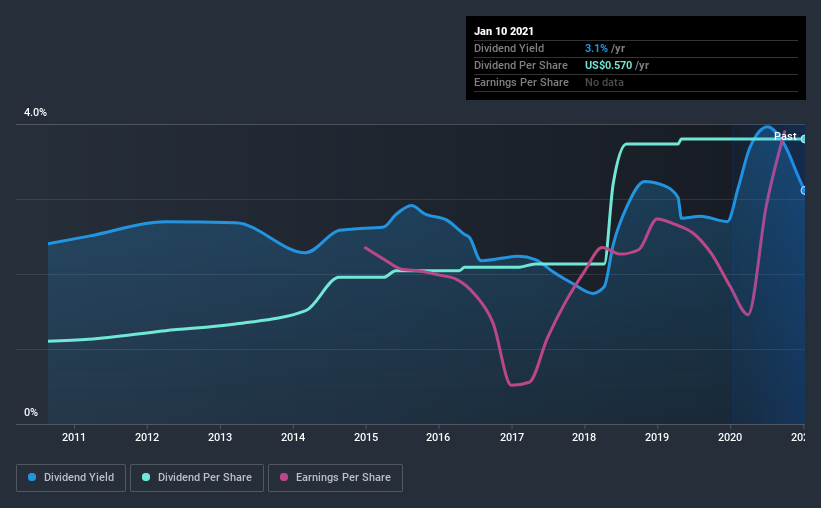

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Blue Ridge Bankshares, Inc. (NYSEMKT:BRBS) is about to trade ex-dividend in the next three days. You can purchase shares before the 15th of January in order to receive the dividend, which the company will pay on the 29th of January.

Blue Ridge Bankshares's next dividend payment will be US$0.14 per share, and in the last 12 months, the company paid a total of US$0.57 per share. Last year's total dividend payments show that Blue Ridge Bankshares has a trailing yield of 3.1% on the current share price of $18.3. If you buy this business for its dividend, you should have an idea of whether Blue Ridge Bankshares's dividend is reliable and sustainable. As a result, readers should always check whether Blue Ridge Bankshares has been able to grow its dividends, or if the dividend might be cut.

View our latest analysis for Blue Ridge Bankshares

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Blue Ridge Bankshares is paying out just 24% of its profit after tax, which is comfortably low and leaves plenty of breathing room in the case of adverse events. Blue Ridge Bankshares paid a dividend despite reporting negative free cash flow last year. That's typically a bad combination and - if this were more than a one-off - not sustainable.

Generally speaking, the lower a company's payout ratios, the more resilient its dividend usually is.

Click here to see how much of its profit Blue Ridge Bankshares paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. For this reason, we're glad to see Blue Ridge Bankshares's earnings per share have risen 11% per annum over the last five years.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Blue Ridge Bankshares has delivered an average of 13% per year annual increase in its dividend, based on the past 10 years of dividend payments. It's exciting to see that both earnings and dividends per share have grown rapidly over the past few years.

The Bottom Line

Should investors buy Blue Ridge Bankshares for the upcoming dividend? Typically, companies that are growing rapidly and paying out a low fraction of earnings are keeping the profits for reinvestment in the business. This is one of the most attractive investment combinations under this analysis, as it can create substantial value for investors over the long run. Overall, Blue Ridge Bankshares looks like a promising dividend stock in this analysis, and we think it would be worth investigating further.

With that in mind, a critical part of thorough stock research is being aware of any risks that stock currently faces. Every company has risks, and we've spotted 3 warning signs for Blue Ridge Bankshares (of which 1 doesn't sit too well with us!) you should know about.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade Blue Ridge Bankshares, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Blue Ridge Bankshares might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSEAM:BRBS

Blue Ridge Bankshares

Operates as a bank holding company for the Blue Ridge Bank, National Association that provides commercial and consumer banking, and financial services.

Excellent balance sheet very low.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|24.5% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|45.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|33.9% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|57.0% undervalued

AX

Community Contributor