- United States

- /

- Banks

- /

- NYSE:WAL

Earnings growth of 12% over 1 year hasn't been enough to translate into positive returns for Western Alliance Bancorporation (NYSE:WAL) shareholders

Even the best stock pickers will make plenty of bad investments. And unfortunately for Western Alliance Bancorporation (NYSE:WAL) shareholders, the stock is a lot lower today than it was a year ago. The share price is down a hefty 64% in that time. Longer term investors have fared much better, since the share price is up 19% in three years. More recently, the share price has dropped a further 59% in a month. Importantly, this could be a market reaction to the recently released financial results. You can check out the latest numbers in our company report.

If the past week is anything to go by, investor sentiment for Western Alliance Bancorporation isn't positive, so let's see if there's a mismatch between fundamentals and the share price.

View our latest analysis for Western Alliance Bancorporation

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

During the unfortunate twelve months during which the Western Alliance Bancorporation share price fell, it actually saw its earnings per share (EPS) improve by 12%. It could be that the share price was previously over-hyped.

The divergence between the EPS and the share price is quite notable, during the year. But we might find some different metrics explain the share price movements better.

Western Alliance Bancorporation's dividend seems healthy to us, so we doubt that the yield is a concern for the market. From what we can see, revenue is pretty flat, so that doesn't really explain the share price drop. Unless, of course, the market was expecting a revenue uptick.

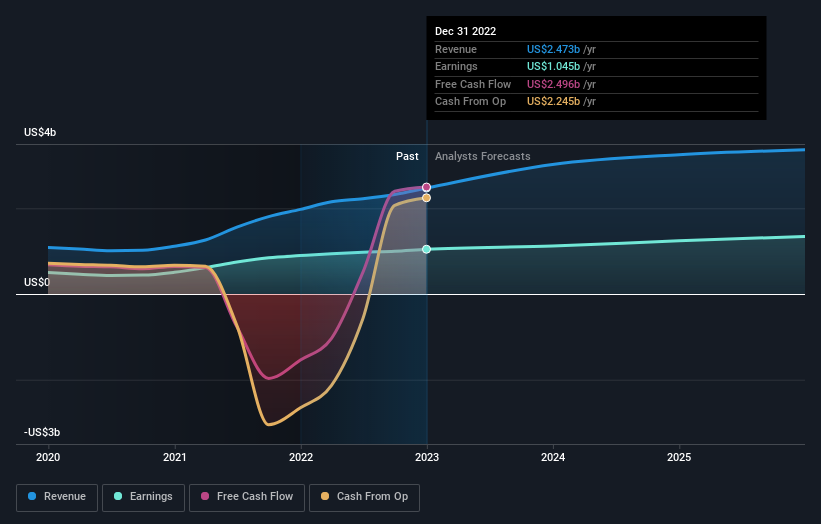

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

We like that insiders have been buying shares in the last twelve months. Even so, future earnings will be far more important to whether current shareholders make money. So we recommend checking out this free report showing consensus forecasts

A Different Perspective

While the broader market lost about 13% in the twelve months, Western Alliance Bancorporation shareholders did even worse, losing 64% (even including dividends). However, it could simply be that the share price has been impacted by broader market jitters. It might be worth keeping an eye on the fundamentals, in case there's a good opportunity. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 7% per year over five years. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. It's always interesting to track share price performance over the longer term. But to understand Western Alliance Bancorporation better, we need to consider many other factors. Case in point: We've spotted 4 warning signs for Western Alliance Bancorporation you should be aware of, and 1 of them shouldn't be ignored.

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Western Alliance Bancorporation might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:WAL

Western Alliance Bancorporation

Operates as the bank holding company for Western Alliance Bank that provides various banking products and related services primarily in Arizona, California, and Nevada.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives