Advertisement

- United States

- /

- Banks

- /

- NYSE:NU

Nu Holdings (NYSE:NU) is Disrupting Banking in Latin America, but the Valuation may be Concerning

Nu Holdings Ltd. (NYSE:NU) is one of the newer stocks added to Warren Buffett's portfolio since the company went public last year. Investors tracking his performance are interested in the qualities of this company, and that is what we will review today.

Just as a side note, Buffet also initiated a stake in Chevron (NYSE:CVX).

A quick glance of the key takeaways from our analysis:

- Nu is poised to be a high growth stock and investors are just catching on

- Estimated to become profitable by the end of 2023

- Enough cash and market cap to fund growth

- Current market cap implies around US$6b earnings in 10 years

See our latest analysis for Nu Holdings

Overview

Nu Holdings Ltd. operates as a digital financial services platform primarily in Brazil, Mexico, and Colombia. It offers credit and debit cards, mobile payment, savings and account services. In a nutshell, it is a general digital banking solution serving more than 48 million customers.

Nu's main point of sale is that it wants to be more convenient and price competitive in relation to traditional banks. A pitch like this may very well be something that can create value in growing economies.

Fundamentals

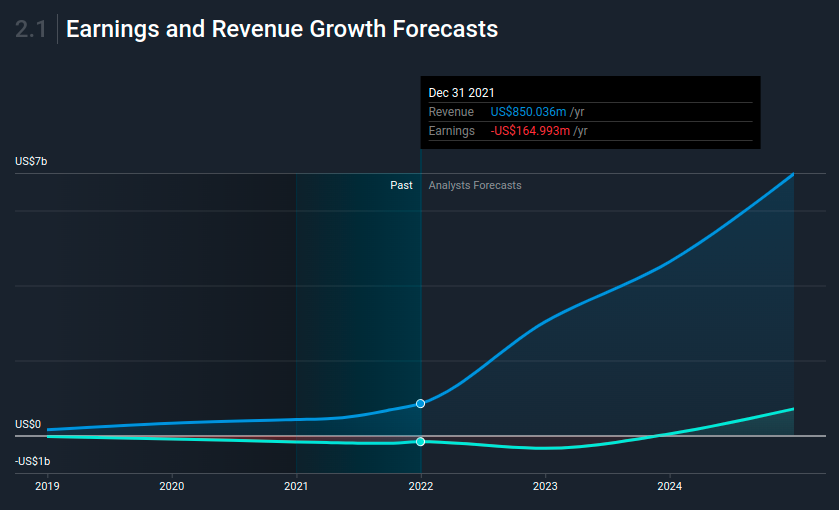

Part of the appeal is both the current and expected high growth for Nu.

Our analyst data illustrates where the company is expected to be in just a few years:

The startup seems to be finishing "setting up the terrain" phase, and is moving to high growth. Analysts expect the company to make close to US$7b in revenue 3 years from now. This would produce a 7x growth for the company. For net income, the projection becomes US$710m by 2025.

Breakeven

This also has implications for when the company is expected to break into profit. According to the 15 analysts covering the company, they expect NU to incur a final loss in 2022, before generating positive profits of US$41m in 2023.

The company is therefore projected to breakeven just over a year from now.

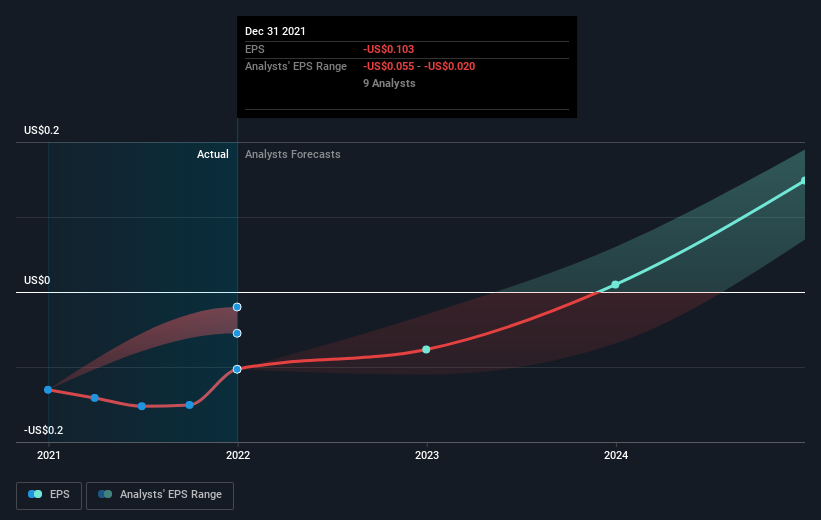

What rate will the company have to grow year-on-year in order to breakeven on this date? Using a line of best fit, we calculated an average EPS annual growth rate of 57%, which is rather optimistic!

The faster a company breaks even, the more value it creates sooner, therefore lowering the discount on future cash flows. Actual positive surprises in earnings may have a positive effect on the stock, if the company is appropriately priced by the market.

Considering that the company is expected to become profitable, the balance sheet is not a concern. But it is good to see that Nu, has a US$3.6b cash position, which can fund them until they break 0.

While debt is not something a pre-profit company should usually dabble with, their borrowings are a low US$259.6m. Given the current US$35.8b market valuation, Nu might be better off funding growth with issuing equity.

Valuation

Everything we do in finance is centered on valuation.

We may use different metrics and methods, but ultimately we want to know what a company like Nu is worth and compare that to today's price before deciding how to move forward.

There currently are no profits and the Price to Book Value of Equity is about 8.1x. The book value of equity increases mostly from the earnings a company retains during operations, which means that it is mostly influenced by Net Income and the value of total assets (such as cash).

Thus, the 8.1x book to equity, gives us an indication of what the current market price implies for the growth of the company. In simple terms, the market expects the company to grow net income by about 80% annually. However, we need to discount these earnings. Normally, we would go with about a 7.2% discount rate, however the company conducts operations primarily in Brazil, Mexico and Columbia, which are regions of the world with significantly more risk.

For this reason, we will set the discount rate to 11.4%, as a mix from operating regions and country risk premiums. This makes the discount rate in 10 years to be around 60% (starts at 11.4% in year 1, and moves down to 7.1% in year 10 accounting for the fact that the company becomes more stable).

If we estimate a scenario where the company earns around US$4b, these earnings have a value of US$1.6b today!

$4.162b * 0.382 discount factor = $1.588b

Decimals can't be predicted 10 years from now, so we are more precise by rounding the number to US$1.6b.

Since the company wants to be competitive in price, we will cap the returns to the costs of capital in the terminal year. This increases the amount of reinvestment needed and gives us earnings in the terminal year of US$3.282b.

By applying our discount rate, we get a present value of US$27b

Calculation: 3.283÷(0,071−0,0237)×(1−0,612)=26.930 or US$27b

- - -

We can now add the present values and get an intrinsic value for the company of about US$28.6b

Compared to the current market cap of US$35.8b, NU seems to be about 25% overvalued.

Arguably, in order to justify the current valuation, the company would need to earn about US$6b in 10 years.

- - -

Next Steps:

This article is not intended to be a comprehensive analysis on Nu Holdings, so if you are interested in understanding the company at a deeper level, take a look at Nu Holdings' company page on Simply Wall St. We've also compiled a list of important aspects you should further research:

- In order for the market valuation to make sense, investors need to be confident that the company can produce about US$6b in earnings in 10 years. Check the company's prospects and see if this is a reasonable number for yourself.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Nu Holdings’s board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

Valuation is complex, but we're here to simplify it.

Discover if Nu Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NYSE:NU

Nu Holdings

Provides digital banking platform in Brazil, Mexico, Colombia, Cayman Islands, Germany, Argentina, the United States, and Uruguay.

Exceptional growth potential with outstanding track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Enterprise, AI & Cloud Growth Ahead, Waiting For the Right Price 💸

Fair Value US$204.74|1.6% overvalued

FR

Community Contributor

Good foundation, but now it's all about the next steps

Fair Value US$147.87|27.9% undervalued

TO

Community Contributor

XTB's Path to 100–120 PLN by 2028 Amid Market Volatility

Fair Value zł100.96|33.3% undervalued

DZ

Community Contributor