- United States

- /

- Banks

- /

- NasdaqGS:HBAN

Is Huntington (HBAN) Using Rate Cuts and Preferred Payouts to Quietly Rebalance Its Growth Playbook?

Reviewed by Sasha Jovanovic

- In early December 2025, Huntington Bancshares reduced its prime rate from 7% to 6.75%, following an earlier cut in October, and its board has declared a US$356.25 per-share quarterly dividend on its 5.70% Series I Non-Cumulative Perpetual Preferred Stock, payable in March 2026.

- This prime rate cut directly lowers borrowing costs for customers on variable-rate products and offers fresh insight into how Huntington is positioning its balance sheet and loan growth priorities amid changing interest-rate conditions.

- With this latest prime rate reduction as a focal point, we’ll now examine how the announcement reshapes Huntington Bancshares’ broader investment narrative.

Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Huntington Bancshares Investment Narrative Recap

To own Huntington Bancshares, you need to believe in a regional bank that can grow beyond its Midwest roots while managing interest rate and integration risks. The latest prime rate cut modestly increases near term margin compression risk but also supports loan demand, so it does not materially change the core catalyst around successful expansion into the South and Carolinas.

The recent declaration of the US$356.25 per share quarterly dividend on the 5.70% Series I preferred stock underscores management’s focus on maintaining capital returns even as the bank trims its prime rate. For investors, this sits alongside branch growth in the Carolinas as a key near term catalyst, while keeping an eye on how further rate moves could affect funding costs and net interest income.

Yet investors should be aware that if interest rates keep drifting lower, Huntington’s margins could come under pressure just as it is ramping up expansion across...

Read the full narrative on Huntington Bancshares (it's free!)

Huntington Bancshares' narrative projects $8.9 billion revenue and $2.3 billion earnings by 2028. This requires 7.3% yearly revenue growth and about a $0.3 billion earnings increase from $2.0 billion today.

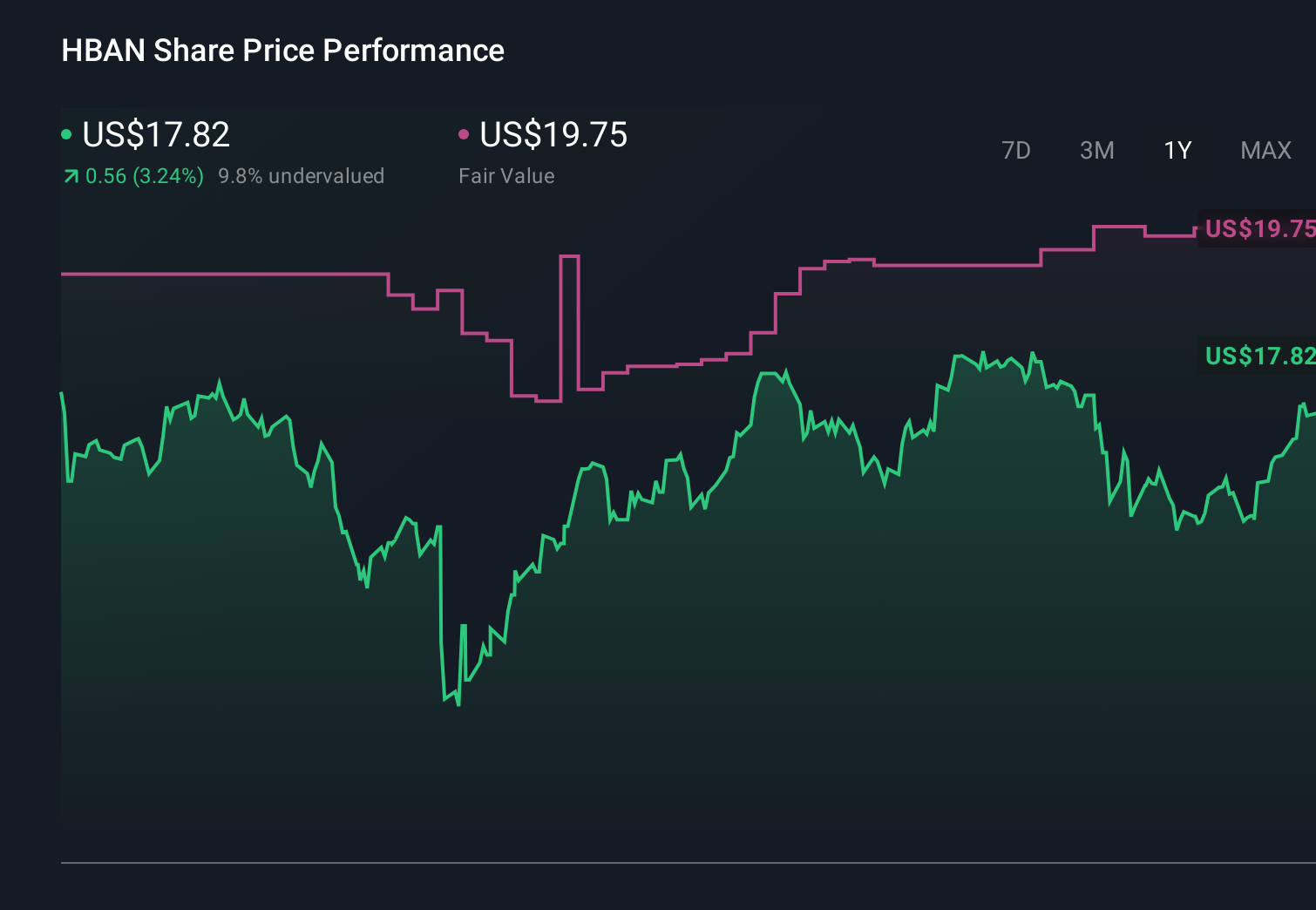

Uncover how Huntington Bancshares' forecasts yield a $19.75 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community currently see Huntington’s fair value between US$11.02 and US$31.89, showing a wide spread of expectations. Against that backdrop, the recent prime rate cut brings margin compression risk into sharper focus and invites you to weigh how future rate moves could influence the bank’s earnings power and growth plans.

Explore 5 other fair value estimates on Huntington Bancshares - why the stock might be worth as much as 79% more than the current price!

Build Your Own Huntington Bancshares Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Huntington Bancshares research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Huntington Bancshares research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Huntington Bancshares' overall financial health at a glance.

Want Some Alternatives?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Rare earth metals are the new gold rush. Find out which 37 stocks are leading the charge.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Huntington Bancshares might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:HBAN

Huntington Bancshares

Operates as the bank holding company for The Huntington National Bank that provides commercial, consumer, and mortgage banking services in the United States.

Flawless balance sheet with high growth potential and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)