Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Harley-Davidson (NYSE:HOG). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

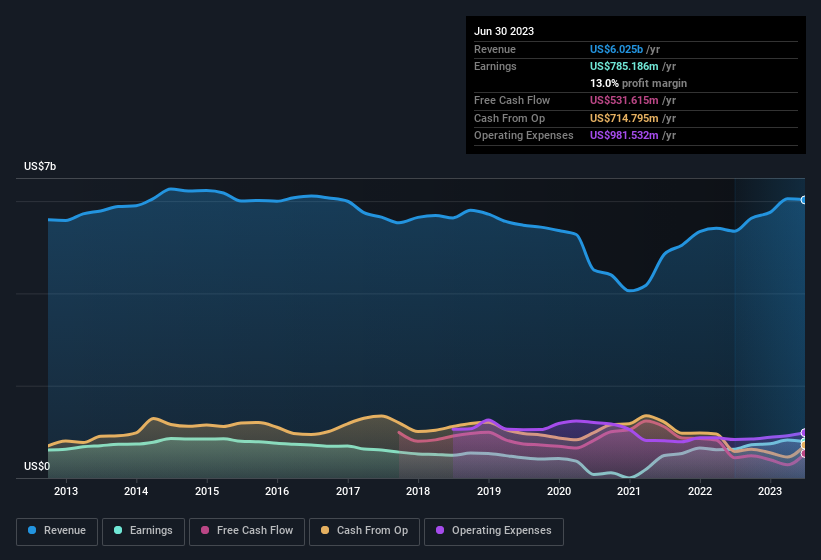

Check out our latest analysis for Harley-Davidson

Harley-Davidson's Improving Profits

Over the last three years, Harley-Davidson has grown earnings per share (EPS) at as impressive rate from a relatively low point, resulting in a three year percentage growth rate that isn't particularly indicative of expected future performance. Thus, it makes sense to focus on more recent growth rates, instead. Harley-Davidson's EPS shot up from US$4.10 to US$5.46; a result that's bound to keep shareholders happy. That's a commendable gain of 33%.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. It's noted that Harley-Davidson's revenue from operations was lower than its revenue in the last twelve months, so that could distort our analysis of its margins. While we note Harley-Davidson achieved similar EBIT margins to last year, revenue grew by a solid 13% to US$6.0b. That's a real positive.

In the chart below, you can see how the company has grown earnings and revenue, over time. For finer detail, click on the image.

While we live in the present moment, there's little doubt that the future matters most in the investment decision process. So why not check this interactive chart depicting future EPS estimates, for Harley-Davidson?

Are Harley-Davidson Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

Although we did see some insider selling (worth US$112k) this was overshadowed by a mountain of buying, totalling US$1.1m in just one year. This adds to the interest in Harley-Davidson because it suggests that those who understand the company best, are optimistic. We also note that it was the Chairman, Jochen Zeitz, who made the biggest single acquisition, paying US$1.0m for shares at about US$38.94 each.

On top of the insider buying, it's good to see that Harley-Davidson insiders have a valuable investment in the business. To be specific, they have US$31m worth of shares. That's a lot of money, and no small incentive to work hard. While their ownership only accounts for 0.6%, this is still a considerable amount at stake to encourage the business to maintain a strategy that will deliver value to shareholders.

Should You Add Harley-Davidson To Your Watchlist?

For growth investors, Harley-Davidson's raw rate of earnings growth is a beacon in the night. Not only that, but we can see that insiders both own a lot of, and are buying more shares in the company. Astute investors will want to keep this stock on watch. It is worth noting though that we have found 3 warning signs for Harley-Davidson (2 are concerning!) that you need to take into consideration.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Harley-Davidson, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Harley-Davidson might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:HOG

Harley-Davidson

Manufactures and sells motorcycles in the United States and internationally.

Very undervalued with adequate balance sheet.

Market Insights

Community Narratives