We Think China Petrochemical Development (TPE:1314) Has A Fair Chunk Of Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that China Petrochemical Development Corporation (TPE:1314) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for China Petrochemical Development

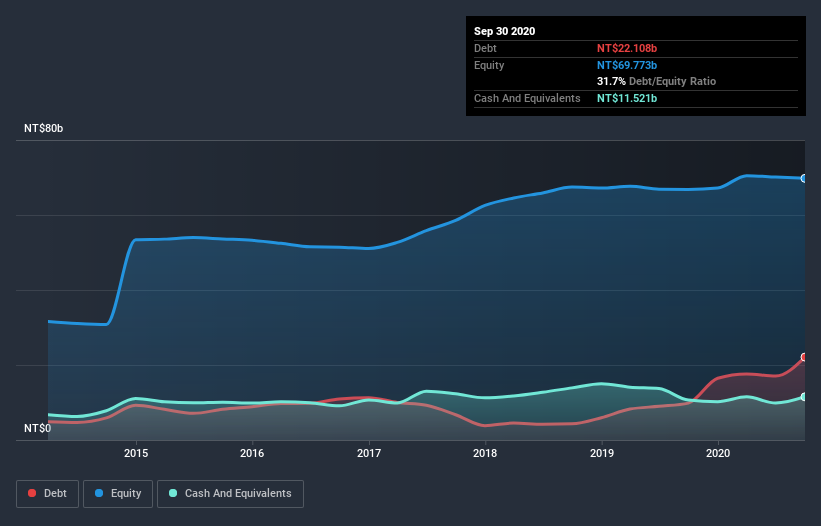

What Is China Petrochemical Development's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of September 2020 China Petrochemical Development had NT$22.1b of debt, an increase on NT$9.84b, over one year. However, it does have NT$11.5b in cash offsetting this, leading to net debt of about NT$10.6b.

How Strong Is China Petrochemical Development's Balance Sheet?

We can see from the most recent balance sheet that China Petrochemical Development had liabilities of NT$9.48b falling due within a year, and liabilities of NT$24.1b due beyond that. Offsetting these obligations, it had cash of NT$11.5b as well as receivables valued at NT$1.64b due within 12 months. So its liabilities total NT$20.4b more than the combination of its cash and short-term receivables.

This is a mountain of leverage relative to its market capitalization of NT$31.2b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since China Petrochemical Development will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, China Petrochemical Development made a loss at the EBIT level, and saw its revenue drop to NT$18b, which is a fall of 45%. That makes us nervous, to say the least.

Caveat Emptor

Not only did China Petrochemical Development's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Indeed, it lost NT$2.3b at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through NT$16b of cash over the last year. So in short it's a really risky stock. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example China Petrochemical Development has 2 warning signs (and 1 which doesn't sit too well with us) we think you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you decide to trade China Petrochemical Development, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:1314

China Petrochemical Development

Produces and sells petrochemical intermediates and related engineering plastics, synthetic resins, chemical fiber, and other derivative products in Taiwan, rest of Asia, and internationally.

Low with imperfect balance sheet.