Advertisement

3 Global Stocks Estimated To Be Up To 36.4% Below Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

As global markets grapple with economic uncertainty and inflation fears, compounded by trade policy concerns and persistent inflation, investors are increasingly cautious. Major indices have faced declines, highlighting the challenges posed by new tariffs and a potential economic slowdown. In such an environment, identifying undervalued stocks can be crucial for investors seeking opportunities to capitalize on discrepancies between market prices and intrinsic values.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Fujikura (TSE:5803) | ¥5342.00 | ¥10643.06 | 49.8% |

| Insource (TSE:6200) | ¥796.00 | ¥1580.36 | 49.6% |

| STI (KOSDAQ:A039440) | ₩22050.00 | ₩44056.68 | 50% |

| Food & Life Companies (TSE:3563) | ¥4461.00 | ¥8864.66 | 49.7% |

| Sangfor Technologies (SZSE:300454) | CN¥102.30 | CN¥202.16 | 49.4% |

| IONOS Group (XTRA:IOS) | €25.95 | €51.45 | 49.6% |

| Fodelia Oyj (HLSE:FODELIA) | €7.02 | €13.91 | 49.5% |

| W5 Solutions (OM:W5) | SEK71.90 | SEK142.79 | 49.6% |

| CJ CGV (KOSE:A079160) | ₩4485.00 | ₩8940.27 | 49.8% |

| Galderma Group (SWX:GALD) | CHF95.43 | CHF190.57 | 49.9% |

Let's explore several standout options from the results in the screener.

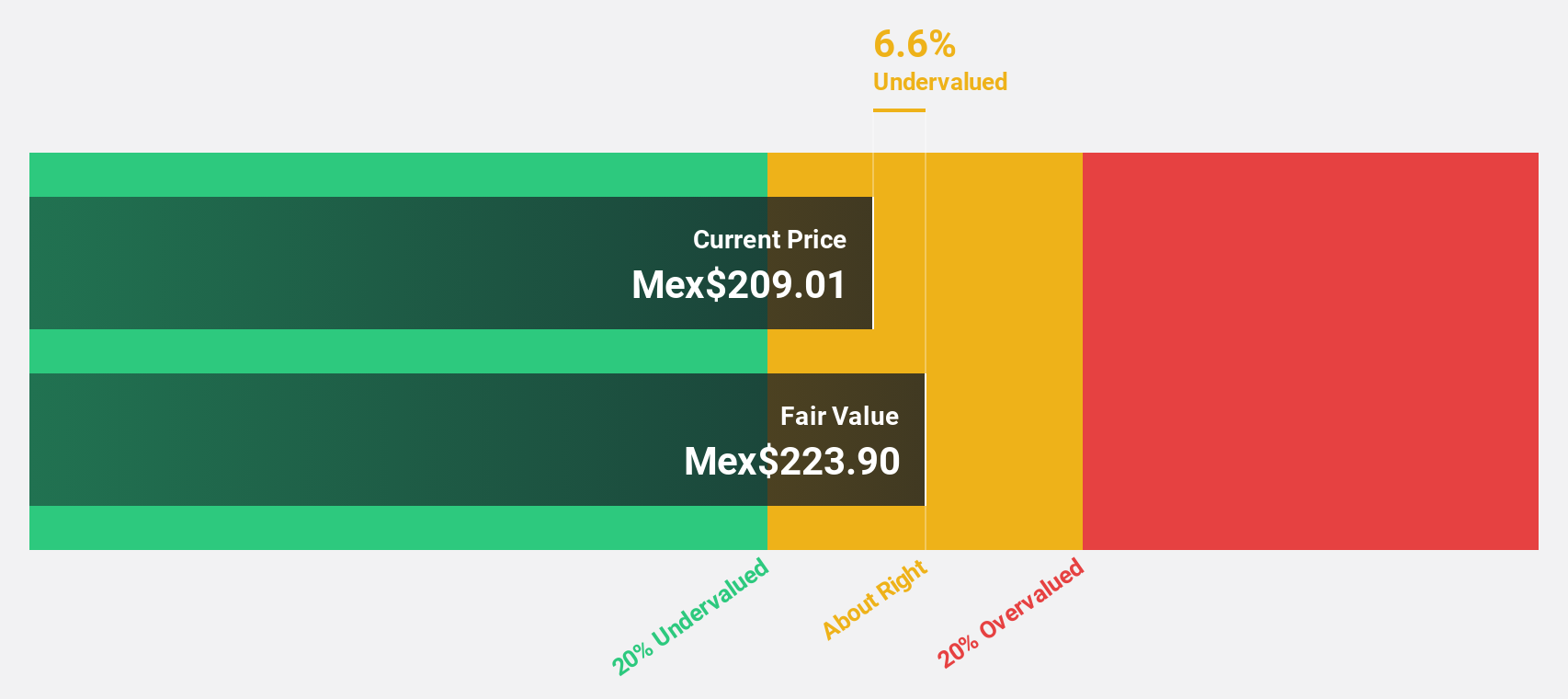

Quálitas Controladora. de (BMV:Q *)

Overview: Quálitas Controladora, S.A.B. de C.V. operates in the automobile insurance sector through its subsidiaries, providing insurance, coinsurance, and reinsurance services across Mexico, El Salvador, Costa Rica, Peru, and the United States with a market cap of MX$70.51 billion.

Operations: Quálitas Controladora's revenue is primarily derived from its insurance, coinsurance, and reinsurance services in the automobile sector across multiple countries including Mexico, El Salvador, Costa Rica, Peru, and the United States.

Estimated Discount To Fair Value: 17%

Quálitas Controladora's recent earnings results show strong growth, with net income rising to MX$5.12 billion for 2024 from MX$3.78 billion the previous year. The stock is currently trading at about 17% below its estimated fair value of MX$215.58, suggesting it may be undervalued based on cash flows. However, its dividend yield of 4.47% is not well covered by free cash flows, which could be a concern for investors prioritizing dividend sustainability.

- In light of our recent growth report, it seems possible that Quálitas Controladora. de's financial performance will exceed current levels.

- Click here and access our complete balance sheet health report to understand the dynamics of Quálitas Controladora. de.

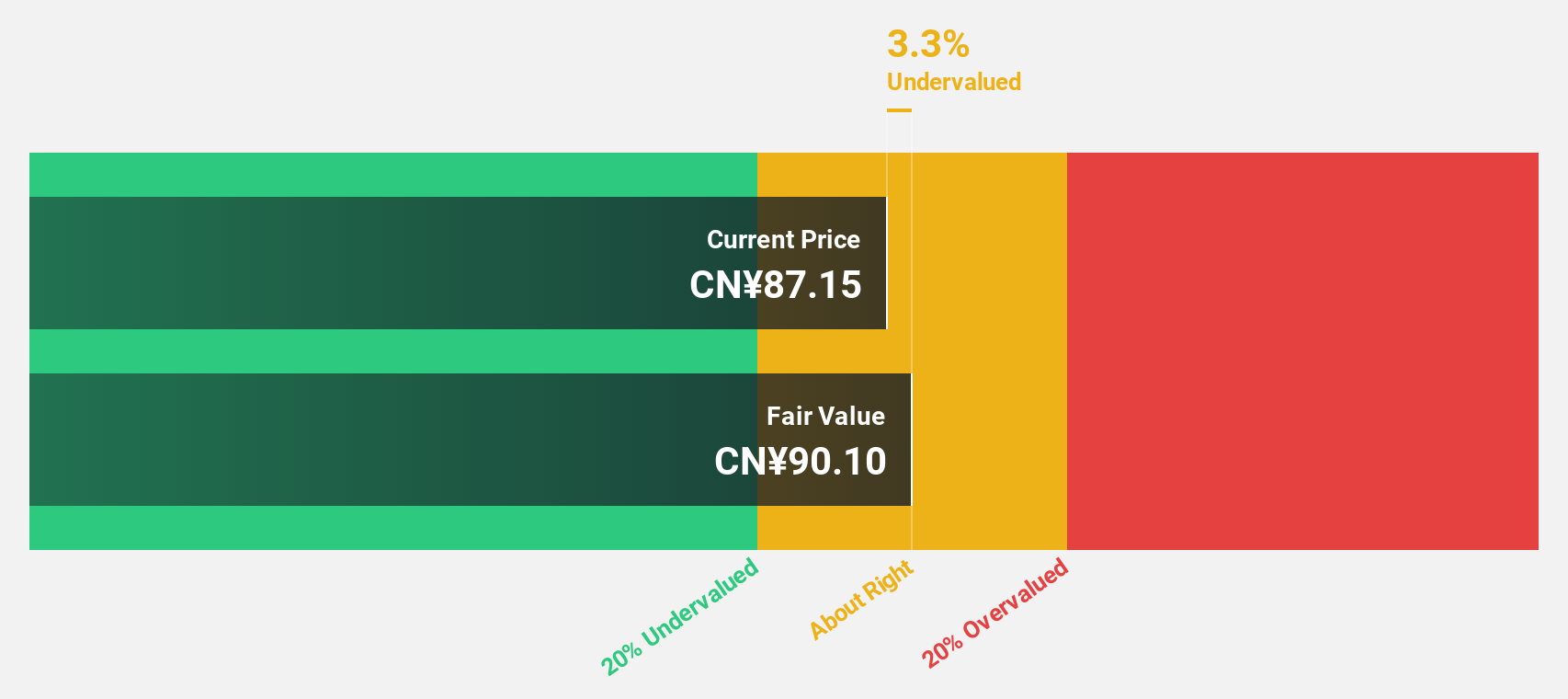

Shanghai MicroPort Endovascular MedTech (SHSE:688016)

Overview: Shanghai MicroPort Endovascular MedTech Co., Ltd. operates in the medical technology sector, focusing on the development and manufacturing of endovascular devices, with a market cap of CN¥11.26 billion.

Operations: Shanghai MicroPort Endovascular MedTech Co., Ltd. generates revenue primarily from the development and manufacturing of endovascular devices within the medical technology sector.

Estimated Discount To Fair Value: 12.7%

Shanghai MicroPort Endovascular MedTech's recent earnings report shows a slight increase in net income to CNY 497.86 million for 2024. The stock is trading at approximately 12.7% below its estimated fair value of CNY 112.73, indicating potential undervaluation based on cash flows. However, the dividend yield of 3.35% is not well covered by free cash flows, which could be a concern for some investors despite forecasts of significant revenue and earnings growth exceeding market averages.

- Insights from our recent growth report point to a promising forecast for Shanghai MicroPort Endovascular MedTech's business outlook.

- Click to explore a detailed breakdown of our findings in Shanghai MicroPort Endovascular MedTech's balance sheet health report.

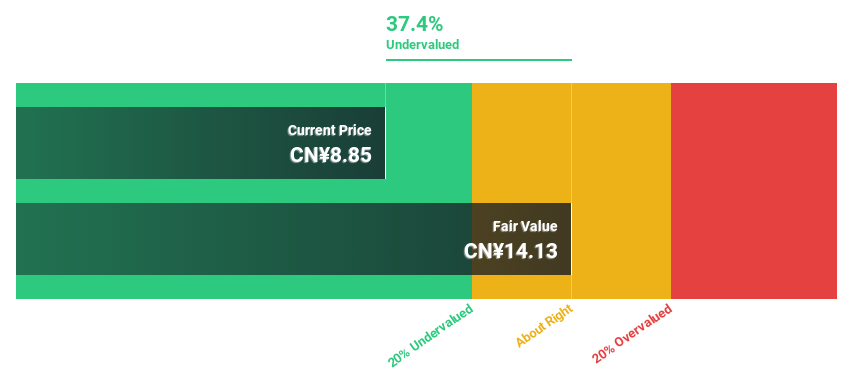

XCMG Construction Machinery (SZSE:000425)

Overview: XCMG Construction Machinery Co., Ltd. manufactures and sells construction machinery in China, with a market cap of CN¥103.14 billion.

Operations: The company generates revenue primarily from its Construction Machinery Industry segment, amounting to CN¥89.90 billion.

Estimated Discount To Fair Value: 36.4%

XCMG Construction Machinery is trading at CN¥8.79, significantly below its estimated fair value of CN¥13.82, suggesting undervaluation based on cash flows. Despite a dividend yield of 2.05% not being well covered by free cash flows, earnings grew by 29.5% last year and are expected to grow at 25.84% annually, outpacing the Chinese market average. Recent initiatives like their Used Equipment Certification program highlight a commitment to sustainability and expanding market presence in Southeast Asia.

- Our comprehensive growth report raises the possibility that XCMG Construction Machinery is poised for substantial financial growth.

- Navigate through the intricacies of XCMG Construction Machinery with our comprehensive financial health report here.

Where To Now?

- Explore the 502 names from our Undervalued Global Stocks Based On Cash Flows screener here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:000425

XCMG Construction Machinery

Engages in the manufacture and sale of construction machinery in China.

Undervalued with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Quality Assets, Cautious Expansion and Commodity Super-cycle To Deliver Steady Revenue Growth

Fair Value US$20.44|3.8% undervalued

ST

Equity Analyst and Writer

Tullow Oil's Share Price Could Soar Up to 135% if Oil Holds at $70

Fair Value UK£0.45|64.0% undervalued

OI

Community Contributor