Advertisement

- South Korea

- /

- Electronic Equipment and Components

- /

- KOSDAQ:A355150

Is Kostecsys (KOSDAQ:355150) Using Too Much Debt?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Kostecsys. Co., Ltd. (KOSDAQ:355150) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Kostecsys's Debt?

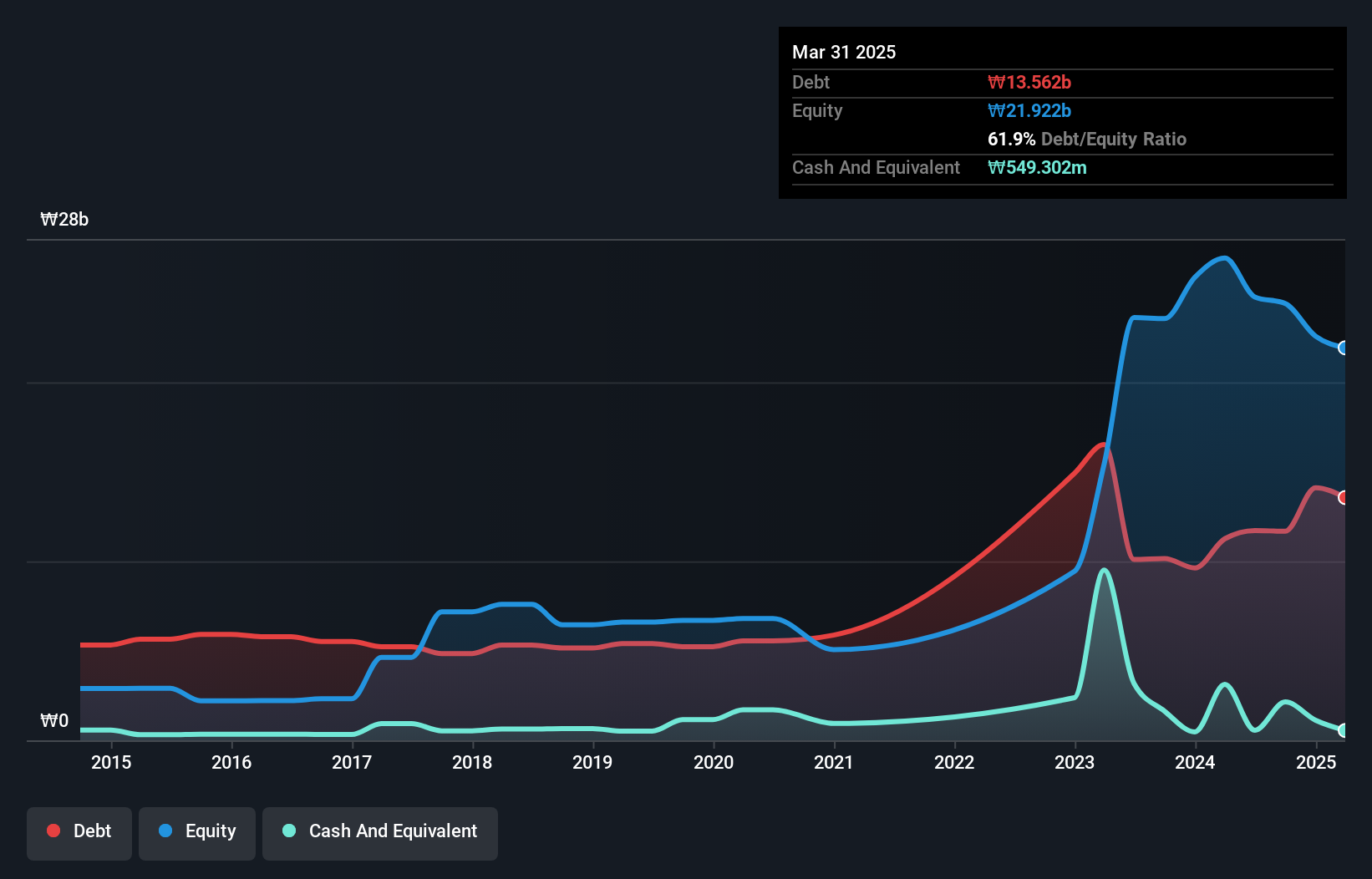

You can click the graphic below for the historical numbers, but it shows that as of March 2025 Kostecsys had ₩13.6b of debt, an increase on ₩11.3b, over one year. On the flip side, it has ₩549.3m in cash leading to net debt of about ₩13.0b.

A Look At Kostecsys' Liabilities

The latest balance sheet data shows that Kostecsys had liabilities of ₩6.63b due within a year, and liabilities of ₩9.53b falling due after that. Offsetting this, it had ₩549.3m in cash and ₩2.79b in receivables that were due within 12 months. So it has liabilities totalling ₩12.8b more than its cash and near-term receivables, combined.

Of course, Kostecsys has a market capitalization of ₩90.1b, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. When analysing debt levels, the balance sheet is the obvious place to start. But it is Kostecsys's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

View our latest analysis for Kostecsys

Over 12 months, Kostecsys reported revenue of ₩14b, which is a gain of 3.5%, although it did not report any earnings before interest and tax. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Importantly, Kostecsys had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost ₩2.5b at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through ₩2.3b of cash over the last year. So suffice it to say we do consider the stock to be risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Kostecsys is showing 4 warning signs in our investment analysis , and 3 of those don't sit too well with us...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Kostecsys might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A355150

Kostecsys

Kostecsys. Co. Ltd. provides low thermal expansion and high thermal conductivity materials for SiC and GaN Next-generation power semiconductors.

Exceptional growth potential with low risk.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4034.1% undervalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6089.9% undervalued

22 followersusers have followed this narrative

2 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.0% undervalued

43 followersusers have followed this narrative

3 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

ST

stuart_roberts on Unicycive Therapeutics ·

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Fair Value:US$21.5370.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KI

KiwiInvest on Rocket Lab ·

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value:US$97.8335.1% undervalued

137 followersusers have followed this narrative

8 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BA

Bauyrzhan on Dollar General ·

Dollar general to grow

Fair Value:US$158.916.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

120 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.7% undervalued

963 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8688.0% undervalued

77 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative