- South Korea

- /

- Aerospace & Defense

- /

- KOSE:A012450

Market Participants Recognise Hanwha Aerospace Co., Ltd.'s (KRX:012450) Earnings Pushing Shares 26% Higher

Hanwha Aerospace Co., Ltd. (KRX:012450) shareholders have had their patience rewarded with a 26% share price jump in the last month. The annual gain comes to 135% following the latest surge, making investors sit up and take notice.

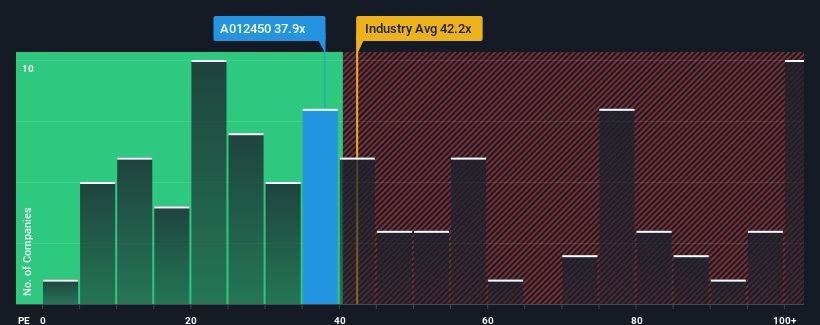

After such a large jump in price, Hanwha Aerospace's price-to-earnings (or "P/E") ratio of 37.9x might make it look like a strong sell right now compared to the market in Korea, where around half of the companies have P/E ratios below 12x and even P/E's below 6x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

With earnings that are retreating more than the market's of late, Hanwha Aerospace has been very sluggish. One possibility is that the P/E is high because investors think the company will turn things around completely and accelerate past most others in the market. If not, then existing shareholders may be very nervous about the viability of the share price.

Check out our latest analysis for Hanwha Aerospace

How Is Hanwha Aerospace's Growth Trending?

Hanwha Aerospace's P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

Retrospectively, the last year delivered a frustrating 28% decrease to the company's bottom line. Even so, admirably EPS has lifted 78% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 36% each year over the next three years. With the market only predicted to deliver 20% each year, the company is positioned for a stronger earnings result.

With this information, we can see why Hanwha Aerospace is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Hanwha Aerospace's P/E?

Shares in Hanwha Aerospace have built up some good momentum lately, which has really inflated its P/E. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Hanwha Aerospace's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Hanwha Aerospace that you should be aware of.

If you're unsure about the strength of Hanwha Aerospace's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Hanwha Aerospace might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A012450

Hanwha Aerospace

Engages in the development, production, and maintenance of aircraft engines worldwide.

Good value with moderate growth potential.