Iveco Group N.V. Just Missed Earnings - But Analysts Have Updated Their Models

It's been a pretty great week for Iveco Group N.V. (BIT:IVG) shareholders, with its shares surging 10% to €10.80 in the week since its latest yearly results. Results overall were not great, with earnings of €0.80 per share falling drastically short of analyst expectations. Meanwhile revenues hit €16b and were slightly better than forecasts. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Iveco Group after the latest results.

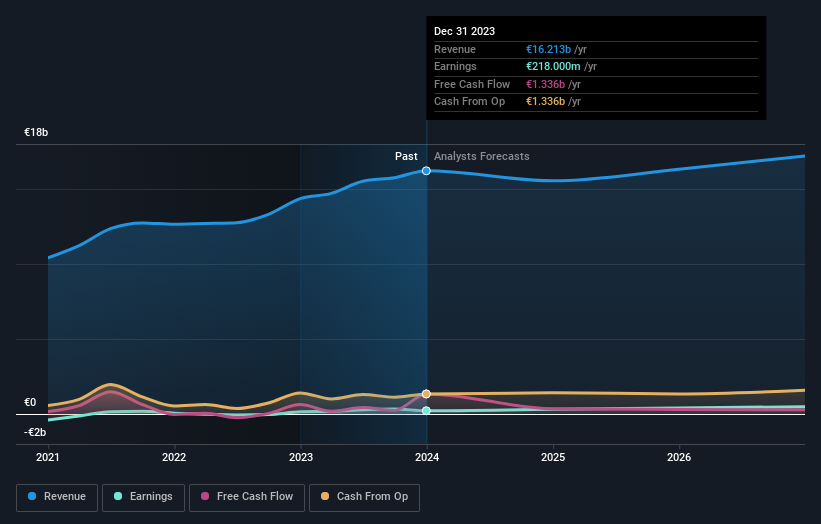

View our latest analysis for Iveco Group

Taking into account the latest results, the current consensus, from the nine analysts covering Iveco Group, is for revenues of €15.5b in 2024. This implies a noticeable 4.1% reduction in Iveco Group's revenue over the past 12 months. Statutory earnings per share are predicted to bounce 43% to €1.18. In the lead-up to this report, the analysts had been modelling revenues of €15.3b and earnings per share (EPS) of €1.24 in 2024. The analysts seem to have become a little more negative on the business after the latest results, given the minor downgrade to their earnings per share numbers for next year.

Althoughthe analysts have revised their earnings forecasts for next year, they've also lifted the consensus price target 6.5% to €11.84, suggesting the revised estimates are not indicative of a weaker long-term future for the business. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Iveco Group at €14.10 per share, while the most bearish prices it at €8.00. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Iveco Group shareholders.

Of course, another way to look at these forecasts is to place them into context against the industry itself. These estimates imply that revenue is expected to slow, with a forecast annualised decline of 4.1% by the end of 2024. This indicates a significant reduction from annual growth of 7.6% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 4.8% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Iveco Group is expected to lag the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. On the plus side, there were no major changes to revenue estimates; although forecasts imply they will perform worse than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

With that in mind, we wouldn't be too quick to come to a conclusion on Iveco Group. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Iveco Group analysts - going out to 2026, and you can see them free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 1 warning sign for Iveco Group that you should be aware of.

If you're looking to trade Iveco Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:IVG

Iveco Group

Engages in the design, production, marketing, sale, servicing, and financing of trucks, commercial vehicles, buses and specialty vehicles, combustion engines, alternative propulsion systems, transmissions, axles, engines, alternative propulsion systems, construction equipment, marine, and power generation applications in Europe, South America, North America, and internationally.

Undervalued with solid track record.

Similar Companies

Market Insights

Community Narratives