Advertisement

- India

- /

- Professional Services

- /

- NSEI:FSL

Here's What Analysts Are Forecasting For Firstsource Solutions Limited (NSE:FSL) After Its Yearly Results

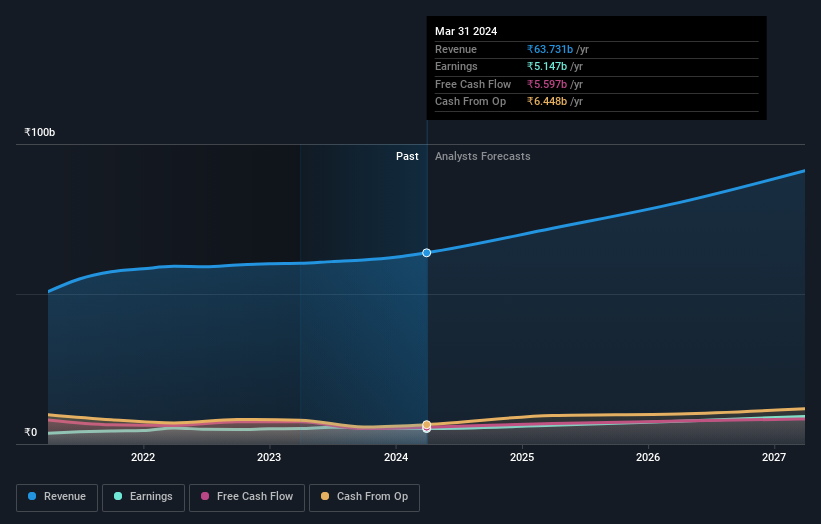

Last week, you might have seen that Firstsource Solutions Limited (NSE:FSL) released its yearly result to the market. The early response was not positive, with shares down 9.3% to ₹198 in the past week. Results were roughly in line with estimates, with revenues of ₹64b and statutory earnings per share of ₹7.34. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

See our latest analysis for Firstsource Solutions

Taking into account the latest results, the current consensus from Firstsource Solutions' nine analysts is for revenues of ₹71.9b in 2025. This would reflect a meaningful 13% increase on its revenue over the past 12 months. Statutory earnings per share are predicted to expand 19% to ₹8.93. Before this earnings report, the analysts had been forecasting revenues of ₹69.7b and earnings per share (EPS) of ₹9.17 in 2025. So it's pretty clear consensus is mixed on Firstsource Solutions after the latest results; whilethe analysts lifted revenue numbers, they also administered a small dip in per-share earnings expectations.

There's been no major changes to the price target of ₹231, suggesting that the impact of higher forecast revenue and lower earnings won't result in a meaningful change to the business' valuation. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Firstsource Solutions analyst has a price target of ₹260 per share, while the most pessimistic values it at ₹200. Even so, with a relatively close grouping of estimates, it looks like the analysts are quite confident in their valuations, suggesting Firstsource Solutions is an easy business to forecast or the the analysts are all using similar assumptions.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Firstsource Solutions' past performance and to peers in the same industry. The period to the end of 2025 brings more of the same, according to the analysts, with revenue forecast to display 13% growth on an annualised basis. That is in line with its 11% annual growth over the past five years. Juxtapose this against our data, which suggests that other companies (with analyst coverage) in the industry are forecast to see their revenues grow 14% per year. So although Firstsource Solutions is expected to maintain its revenue growth rate, it's only growing at about the rate of the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Firstsource Solutions. There was also an upgrade to revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that in mind, we wouldn't be too quick to come to a conclusion on Firstsource Solutions. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Firstsource Solutions analysts - going out to 2027, and you can see them free on our platform here.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Firstsource Solutions that you need to be mindful of.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:FSL

Firstsource Solutions

Provides tech-enabled business processes in India, the United Kingdom, the United States, the United Arab Emirates, and internationally.

High growth potential with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2510.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

SO

sorkdhkddlek on Marvell Technology ·

From AI Infrastructure Plumber to Full-Stack AI Factory Architect

Fair Value:US$14016.9% overvalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MI

MiningStockAnalyst on Aurelia Metals ·

Aurelia Metals Limited — Transitioning Into a Higher-Quality Mid-Tier Producer

Fair Value:AU$0.426.3% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CO

composite32 on TotalEnergies ·

Is This strategic transformation of TTE? Significant re-rating potential

Fair Value:€88.2910.9% undervalued

17 followersusers have followed this narrative

2 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

MI

MiningStockAnalyst on Cobre ·

Cobre Limited Deep Dive: Can Sierra Atacama Unlock a Producer-Level Copper Valuation?

Fair Value:AU$0.5160.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HE

heartwood on Adobe ·

Classic Value Trap

Fair Value:US$163.2355.6% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Polymetals Resources ·

13x Aussie Polymetal Silver/Zinc/Lead Project

Fair Value:AU$15.5294.3% undervalued

4 followersusers have followed this narrative

1 commentusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.235.0% undervalued

68 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9326.4% undervalued

1395 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74017.5% undervalued

31 followersusers have followed this narrative

3 commentsusers have commented on this narrative

32 likesusers have liked this narrative