- Hong Kong

- /

- Transportation

- /

- SEHK:66

This Is Why MTR Corporation Limited's (HKG:66) CEO Compensation Looks Appropriate

Key Insights

- MTR will host its Annual General Meeting on 21st of May

- Salary of HK$9.80m is part of CEO Jacob Kam's total remuneration

- Total compensation is 81% below industry average

- Over the past three years, MTR's EPS grew by 18% and over the past three years, the total loss to shareholders 26%

Performance at MTR Corporation Limited (HKG:66) has been rather uninspiring recently and shareholders may be wondering how CEO Jacob Kam plans to fix this. At the next AGM coming up on 21st of May, they can influence managerial decision making through voting on resolutions, including executive remuneration. It has been shown that setting appropriate executive remuneration incentivises the management to act in the interests of shareholders. We think CEO compensation looks appropriate given the data we have put together.

See our latest analysis for MTR

How Does Total Compensation For Jacob Kam Compare With Other Companies In The Industry?

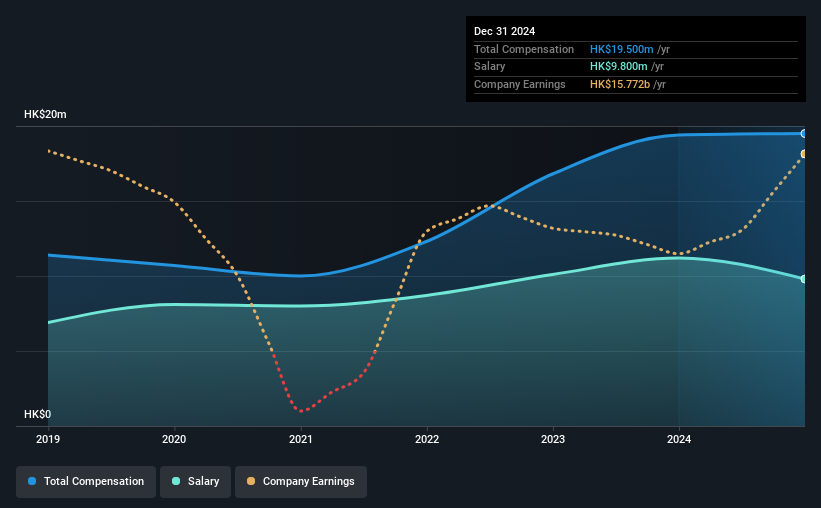

According to our data, MTR Corporation Limited has a market capitalization of HK$174b, and paid its CEO total annual compensation worth HK$20m over the year to December 2024. This means that the compensation hasn't changed much from last year. In particular, the salary of HK$9.80m, makes up a fairly large portion of the total compensation being paid to the CEO.

On comparing similar companies in the Hong Kong Transportation industry with market capitalizations above HK$62b, we found that the median total CEO compensation was HK$104m. Accordingly, MTR pays its CEO under the industry median. Furthermore, Jacob Kam directly owns HK$23m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | HK$9.8m | HK$11m | 50% |

| Other | HK$9.7m | HK$8.2m | 50% |

| Total Compensation | HK$20m | HK$19m | 100% |

Speaking on an industry level, nearly 60% of total compensation represents salary, while the remainder of 40% is other remuneration. MTR sets aside a smaller share of compensation for salary, in comparison to the overall industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at MTR Corporation Limited's Growth Numbers

Over the past three years, MTR Corporation Limited has seen its earnings per share (EPS) grow by 18% per year. It achieved revenue growth of 5.3% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's also good to see modest revenue growth, suggesting the underlying business is healthy. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has MTR Corporation Limited Been A Good Investment?

Since shareholders would have lost about 26% over three years, some MTR Corporation Limited investors would surely be feeling negative emotions. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

The loss to shareholders over the past three years is certainly concerning. This diverges with the robust growth in EPS, suggesting that there is a large discrepancy between share price and fundamentals. A key focus for the board and management will be how to align the share price with fundamentals. The upcoming AGM will provide shareholders the opportunity to raise their concerns and evaluate if the board’s judgement and decision-making is aligned with their expectations.

CEO pay is simply one of the many factors that need to be considered while examining business performance. That's why we did our research, and identified 2 warning signs for MTR (of which 1 makes us a bit uncomfortable!) that you should know about in order to have a holistic understanding of the stock.

Important note: MTR is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you're looking to trade MTR, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:66

MTR

Engages in railway design, construction, operation, maintenance, and investment in Hong Kong, Australia, Mainland China, Macao, Sweden, and the United Kingdom.

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives