Advertisement

- Australia

- /

- Capital Markets

- /

- ASX:MFG

Asian Undervalued Small Caps With Insider Action For April 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets grapple with economic uncertainty and inflation fears, Asian small-cap stocks present a unique opportunity for investors seeking value amid broader market volatility. In this environment, identifying companies with strong fundamentals and strategic insider actions can be key to uncovering potential in the small-cap segment.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Security Bank | 4.8x | 1.1x | 35.86% | ★★★★★★ |

| New Hope | 5.5x | 1.6x | 28.27% | ★★★★★★ |

| Atturra | 27.0x | 1.1x | 41.34% | ★★★★★☆ |

| Viva Energy Group | NA | 0.1x | 20.72% | ★★★★★☆ |

| Dicker Data | 18.8x | 0.6x | -37.01% | ★★★★☆☆ |

| Puregold Price Club | 9.0x | 0.4x | 15.82% | ★★★★☆☆ |

| Sing Investments & Finance | 7.5x | 3.8x | 33.84% | ★★★★☆☆ |

| Integral Diagnostics | 149.0x | 1.7x | 42.76% | ★★★☆☆☆ |

| Zip Co | NA | 2.2x | -64.63% | ★★★☆☆☆ |

| Manawa Energy | NA | 2.6x | 43.39% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

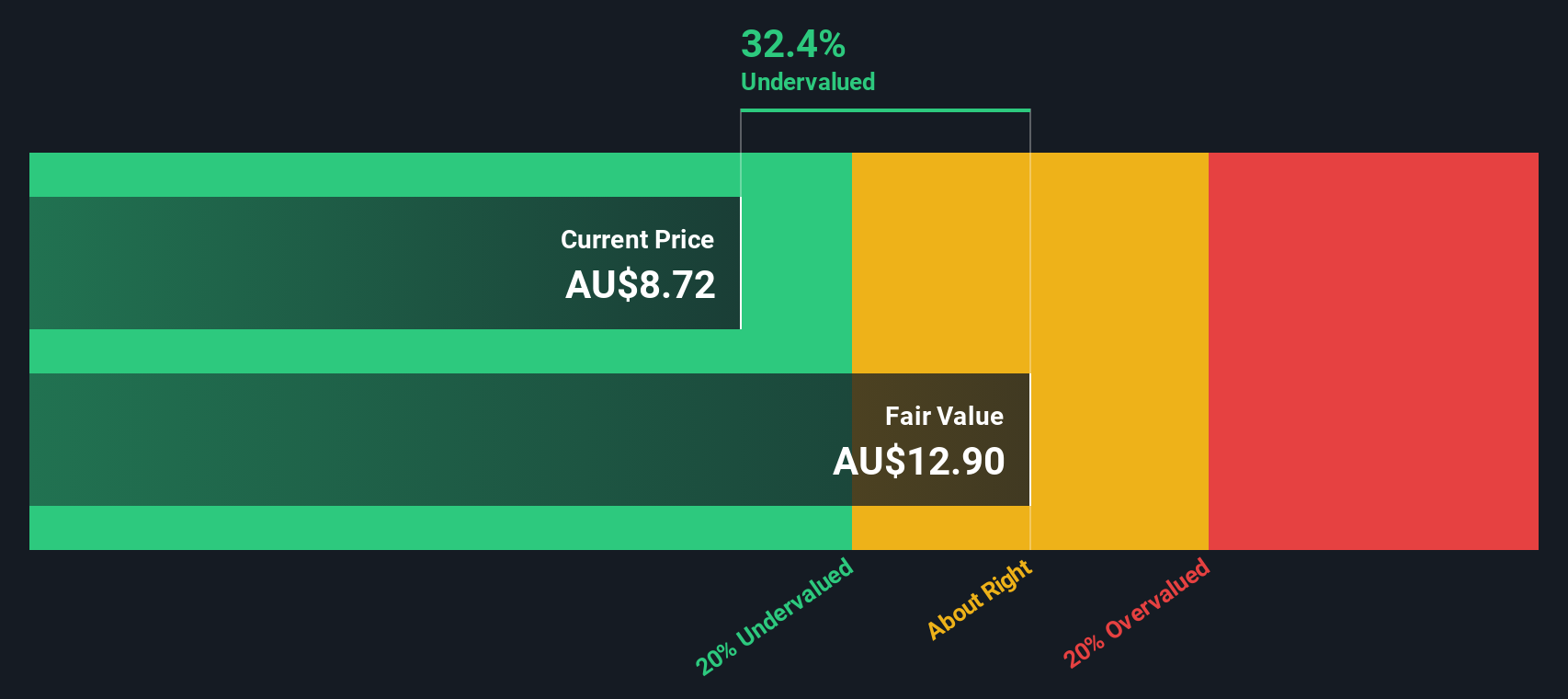

Magellan Financial Group (ASX:MFG)

Simply Wall St Value Rating: ★★★★★★

Overview: Magellan Financial Group is an Australian-based investment management company with a focus on global equities and infrastructure, boasting a market cap of A$3.57 billion.

Operations: The company generates revenue primarily from Fund Investments, with additional contributions from Corporate and Associate Investments. Over recent periods, the net profit margin has shown variation, reaching as high as 69.63% and as low as 36.83%. Operating expenses include significant allocations to General & Administrative Expenses and Sales & Marketing Expenses.

PE: 5.8x

Magellan Financial Group, a smaller player in the Asian market, has seen insider confidence with recent share repurchases totaling A$70.6 million by December 2024. Despite a dip in net income to A$94.01 million for the half-year ending December 2024, revenue grew to A$178.61 million from the previous year. The company is undergoing strategic leadership changes with new appointments like Dean McGuire as CFO and Sophia Rahmani as Director, potentially steering towards future growth amidst expected earnings decline over the next three years.

- Get an in-depth perspective on Magellan Financial Group's performance by reading our valuation report here.

Learn about Magellan Financial Group's historical performance.

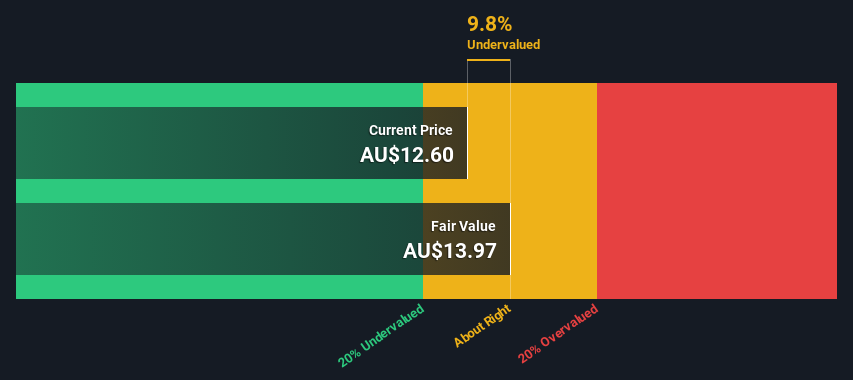

Super Retail Group (ASX:SUL)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Super Retail Group is a leading Australian retail company operating several well-known brands, including Super Cheap Auto, Rebel, Macpac, and Boating, Camping and Fishing (BCF), with a market capitalization of A$2.55 billion.

Operations: Revenue streams are primarily derived from SCA, Rebel, and BCF segments. The net income margin has shown variability, peaking at 8.72% in June 2021 before declining to 5.71% by April 2025. Operating expenses consistently form a significant portion of costs, with sales and marketing being notable contributors.

PE: 12.9x

Super Retail Group, a smaller player in Asia's retail sector, shows potential despite some challenges. Recent earnings for the half-year ending December 2024 reported sales of A$2.11 billion, up from A$2.03 billion the previous year, though net income dipped to A$129.8 million from A$143.4 million. Insider confidence is evident with share purchases over recent months, suggesting optimism about future performance amid reliance on external borrowing for funding. The company announced a fully franked dividend of A$0.32 per share payable in April 2025, reflecting steady shareholder returns despite mixed financial results and forecasts of moderate growth at 4.71% annually.

- Unlock comprehensive insights into our analysis of Super Retail Group stock in this valuation report.

Gain insights into Super Retail Group's past trends and performance with our Past report.

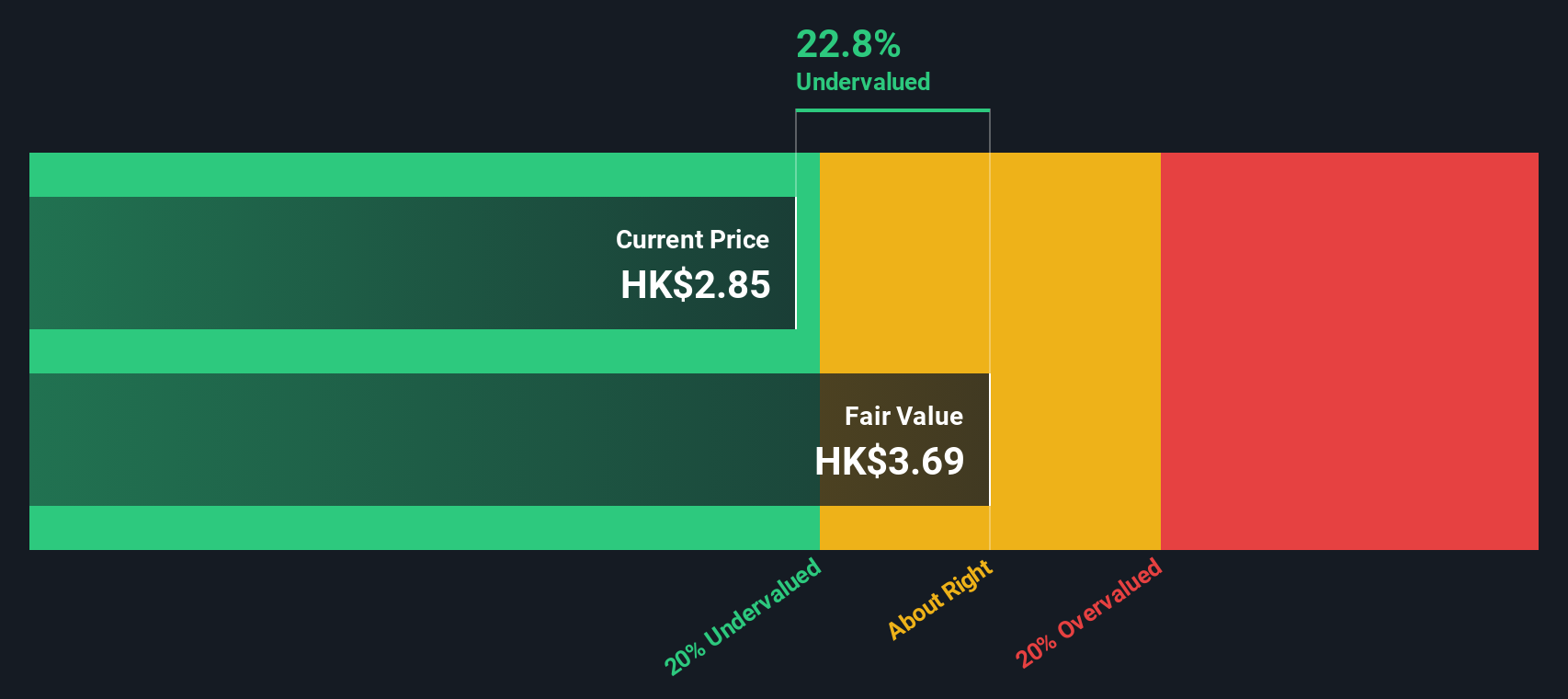

SSY Group (SEHK:2005)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: SSY Group is a company engaged in the production and distribution of medical materials and intravenous infusion solutions, with a market capitalization of HK$10.43 billion.

Operations: The company generates revenue primarily from its Intravenous Infusion Solution and Others segment, contributing significantly to its overall income. The net profit margin has shown variation over the periods, reaching 21.11% in June 2024 before declining to 18.38% by December 2024. Operating expenses are a major component of costs, with sales and marketing being a significant expenditure area.

PE: 9.6x

SSY Group, a smaller pharmaceutical player in Asia, has seen insider confidence with share purchases over recent months. Their earnings for 2024 showed a decline to HK$1.06 billion from HK$1.32 billion the previous year, reflecting challenges but also potential for rebound given their aggressive product expansion. Recent approvals from China's NMPA for various drugs like Nicardipine Hydrochloride and Arbidol Hydrochloride Tablets highlight their strategic focus on diversifying offerings in critical treatment areas, potentially enhancing future revenue streams despite current funding risks due to reliance on external borrowing.

- Click here and access our complete valuation analysis report to understand the dynamics of SSY Group.

Understand SSY Group's track record by examining our Past report.

Seize The Opportunity

- Discover the full array of 57 Undervalued Asian Small Caps With Insider Buying right here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:MFG

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality Assets, Cautious Expansion and Commodity Super-cycle To Deliver Steady Revenue Growth

Fair Value US$20.44|5.0% undervalued

ST

Equity Analyst and Writer

Tullow Oil's Share Price Could Soar Up to 135% if Oil Holds at $70

Fair Value UK£0.45|63.8% undervalued

OI

Community Contributor