Bright Future Technology Holdings Limited's (HKG:1351) CEO Will Probably Find It Hard To See A Huge Raise This Year

Key Insights

- Bright Future Technology Holdings' Annual General Meeting to take place on 22nd of May

- Salary of CN¥1.55m is part of CEO Hui Dong's total remuneration

- The overall pay is comparable to the industry average

- Bright Future Technology Holdings' EPS grew by 85% over the past three years while total shareholder loss over the past three years was 44%

The underwhelming share price performance of Bright Future Technology Holdings Limited (HKG:1351) in the past three years would have disappointed many shareholders. However, what is unusual is that EPS growth has been positive, suggesting that the share price has diverged from fundamentals. Shareholders may want to question the board on the future direction of the company at the upcoming AGM on 22nd of May. Voting on resolutions such as executive remuneration and other matters could also be a way to influence management. We think shareholders might be reluctant to increase compensation for the CEO at the moment, according to our analysis below.

Check out our latest analysis for Bright Future Technology Holdings

Comparing Bright Future Technology Holdings Limited's CEO Compensation With The Industry

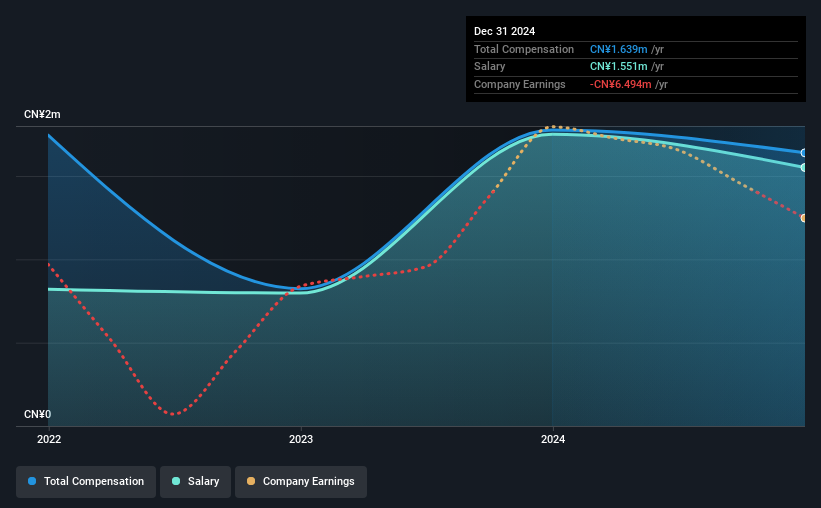

According to our data, Bright Future Technology Holdings Limited has a market capitalization of HK$128m, and paid its CEO total annual compensation worth CN¥1.6m over the year to December 2024. That's a slight decrease of 7.7% on the prior year. In particular, the salary of CN¥1.55m, makes up a huge portion of the total compensation being paid to the CEO.

In comparison with other companies in the Hong Kong Media industry with market capitalizations under HK$1.6b, the reported median total CEO compensation was CN¥1.7m. From this we gather that Hui Dong is paid around the median for CEOs in the industry. What's more, Hui Dong holds HK$46m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | CN¥1.6m | CN¥1.8m | 95% |

| Other | CN¥88k | CN¥26k | 5% |

| Total Compensation | CN¥1.6m | CN¥1.8m | 100% |

On an industry level, roughly 81% of total compensation represents salary and 19% is other remuneration. Bright Future Technology Holdings is paying a higher share of its remuneration through a salary in comparison to the overall industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Bright Future Technology Holdings Limited's Growth Numbers

Over the past three years, Bright Future Technology Holdings Limited has seen its earnings per share (EPS) grow by 85% per year. Its revenue is up 16% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's also good to see decent revenue growth in the last year, suggesting the business is healthy and growing. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Bright Future Technology Holdings Limited Been A Good Investment?

Few Bright Future Technology Holdings Limited shareholders would feel satisfied with the return of -44% over three years. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

Despite the growth in its earnings, the share price decline in the past three years is certainly concerning. A huge lag in share price growth when earnings have grown may indicate there could be other issues that are affecting the company at the moment that the market is focused on. If there are some unknown variables that are influencing the stock's price, surely shareholders would have some concerns. The upcoming AGM will be a chance for shareholders to question the board on key matters, such as CEO remuneration or any other issues they might have and revisit their investment thesis with regards to the company.

CEO pay is simply one of the many factors that need to be considered while examining business performance. We identified 3 warning signs for Bright Future Technology Holdings (2 are concerning!) that you should be aware of before investing here.

Switching gears from Bright Future Technology Holdings, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Bright Future Technology Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1351

Bright Future Technology Holdings

An investment holding company, together with its subsidiaries, engages in the provision of intelligent marketing solutions in the People’s Republic of China.

Slight risk and slightly overvalued.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)