Lonking Holdings (HKG:3339) Is Increasing Its Dividend To CN¥0.13

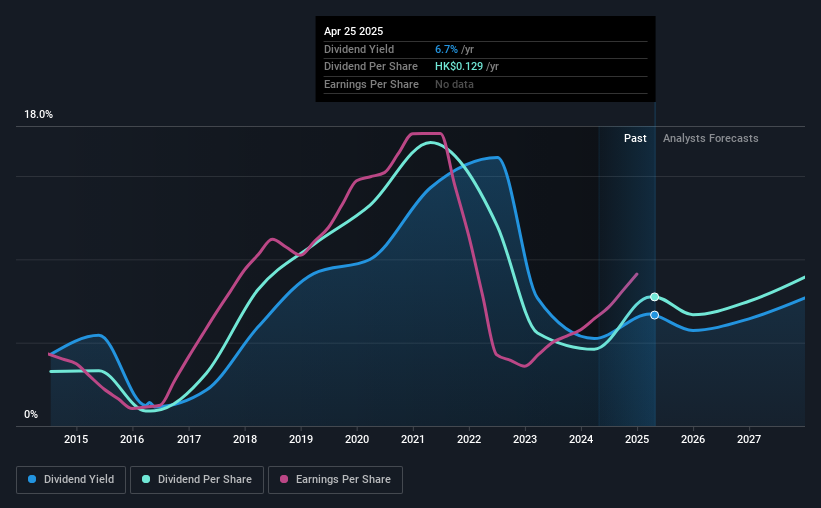

Lonking Holdings Limited's (HKG:3339) dividend will be increasing from last year's payment of the same period to CN¥0.13 on 31st of July. This makes the dividend yield 6.7%, which is above the industry average.

Our free stock report includes 1 warning sign investors should be aware of before investing in Lonking Holdings. Read for free now.Lonking Holdings' Future Dividend Projections Appear Well Covered By Earnings

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. The last dividend was quite easily covered by Lonking Holdings' earnings. This indicates that a lot of the earnings are being reinvested into the business, with the aim of fueling growth.

Over the next year, EPS is forecast to expand by 36.6%. If the dividend continues on this path, the payout ratio could be 44% by next year, which we think can be pretty sustainable going forward.

See our latest analysis for Lonking Holdings

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. Since 2015, the dividend has gone from CN¥0.0512 total annually to CN¥0.121. This means that it has been growing its distributions at 9.0% per annum over that time. We like to see dividends have grown at a reasonable rate, but with at least one substantial cut in the payments, we're not certain this dividend stock would be ideal for someone intending to live on the income.

Dividend Growth May Be Hard To Come By

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Lonking Holdings has seen earnings per share falling at 9.1% per year over the last five years. If the company is making less over time, it naturally follows that it will also have to pay out less in dividends. Earnings are predicted to grow over the next year, but we would remain cautious until a track record of earnings growth is established.

Our Thoughts On Lonking Holdings' Dividend

In summary, while it's always good to see the dividend being raised, we don't think Lonking Holdings' payments are rock solid. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. We don't think Lonking Holdings is a great stock to add to your portfolio if income is your focus.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. Taking the debate a bit further, we've identified 1 warning sign for Lonking Holdings that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:3339

Lonking Holdings

An investment holding company, manufactures and distributes wheel loaders, road rollers, excavators, forklifts, and other construction machinery in Mainland China and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Community Narratives