- United Kingdom

- /

- Transportation

- /

- LSE:FGP

We Think FirstGroup (LON:FGP) Is Taking Some Risk With Its Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies FirstGroup plc (LON:FGP) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

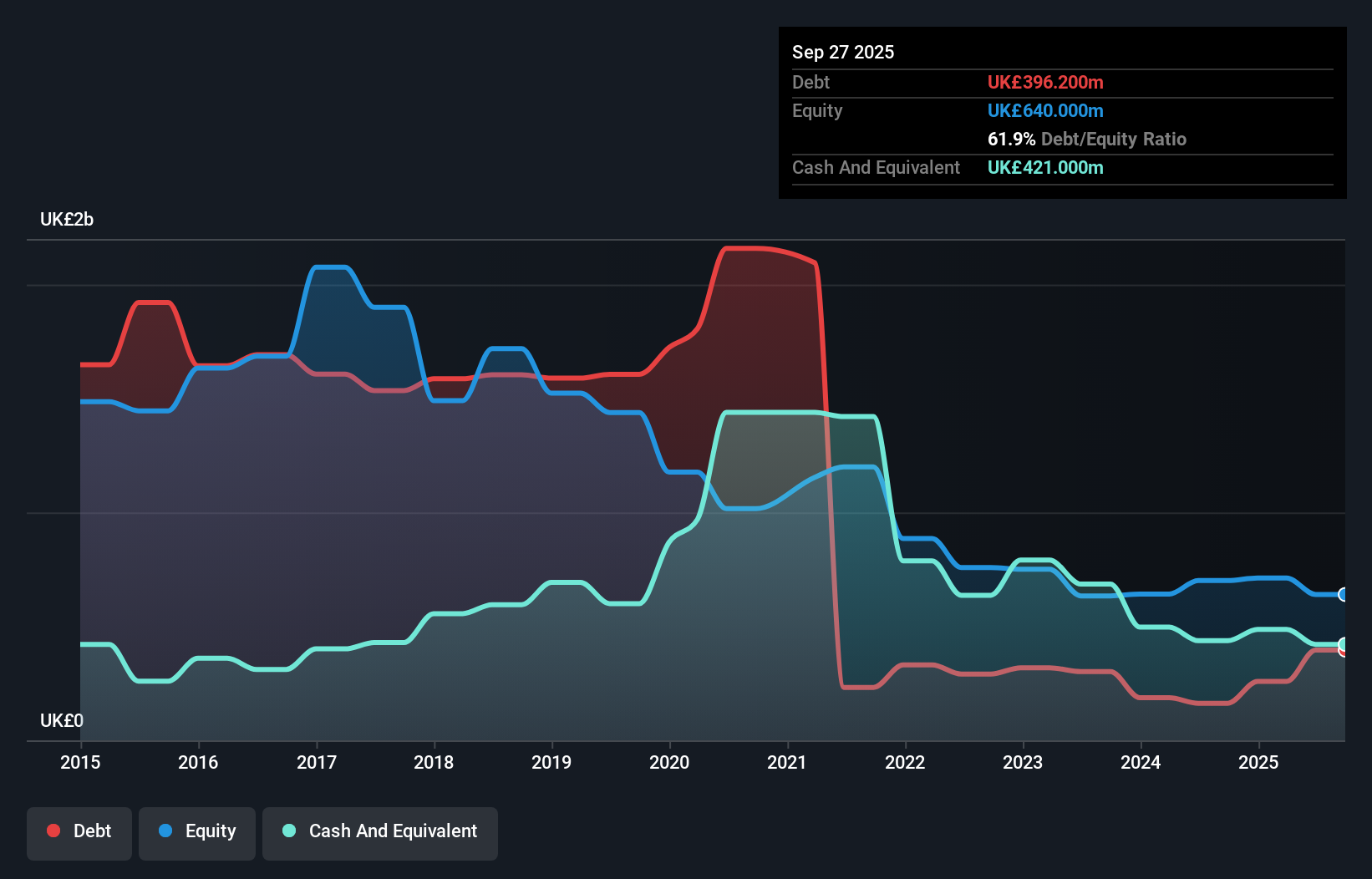

What Is FirstGroup's Debt?

As you can see below, at the end of September 2025, FirstGroup had UK£396.2m of debt, up from UK£162.7m a year ago. Click the image for more detail. But on the other hand it also has UK£421.0m in cash, leading to a UK£24.8m net cash position.

How Healthy Is FirstGroup's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that FirstGroup had liabilities of UK£1.67b due within 12 months and liabilities of UK£1.05b due beyond that. On the other hand, it had cash of UK£421.0m and UK£654.4m worth of receivables due within a year. So it has liabilities totalling UK£1.65b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the UK£1.02b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, FirstGroup would likely require a major re-capitalisation if it had to pay its creditors today. FirstGroup boasts net cash, so it's fair to say it does not have a heavy debt load, even if it does have very significant liabilities, in total.

See our latest analysis for FirstGroup

If FirstGroup can keep growing EBIT at last year's rate of 12% over the last year, then it will find its debt load easier to manage. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if FirstGroup can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While FirstGroup has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, FirstGroup actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing Up

While FirstGroup does have more liabilities than liquid assets, it also has net cash of UK£24.8m. And it impressed us with free cash flow of UK£417m, being 342% of its EBIT. So while FirstGroup does not have a great balance sheet, it's certainly not too bad. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 1 warning sign for FirstGroup you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:FGP

Solid track record and good value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)