- United Kingdom

- /

- Real Estate

- /

- LSE:FOXT

3 UK Stocks Estimated To Be Up To 48.4% Below Intrinsic Value

Reviewed by Simply Wall St

Over the last 7 days, the United Kingdom market has remained flat, yet it boasts a 7.8% increase over the past year with earnings forecasted to grow by 15% annually. In this context of steady growth and potential, identifying stocks that are trading below their intrinsic value can offer investors opportunities for significant returns.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| TBC Bank Group (LSE:TBCG) | £30.65 | £59.35 | 48.4% |

| Gaming Realms (AIM:GMR) | £0.37 | £0.72 | 48.3% |

| Fevertree Drinks (AIM:FEVR) | £7.29 | £13.12 | 44.5% |

| Brickability Group (AIM:BRCK) | £0.659 | £1.25 | 47.1% |

| GlobalData (AIM:DATA) | £1.98 | £3.74 | 47% |

| Tracsis (AIM:TRCS) | £5.30 | £9.72 | 45.5% |

| Vp (LSE:VP.) | £5.50 | £9.79 | 43.8% |

| Informa (LSE:INF) | £8.448 | £15.72 | 46.3% |

| Videndum (LSE:VID) | £2.45 | £4.61 | 46.8% |

| St. James's Place (LSE:STJ) | £8.55 | £15.95 | 46.4% |

Let's review some notable picks from our screened stocks.

Henry Boot (LSE:BOOT)

Overview: Henry Boot PLC operates in the United Kingdom, focusing on property investment and development, land promotion, and construction activities, with a market cap of £298.02 million.

Operations: The company's revenue is derived from property investment and development (£170.56 million), construction (£87.90 million), and land promotion (£28.37 million) in the United Kingdom.

Estimated Discount To Fair Value: 24.1%

Henry Boot appears undervalued with its stock trading at £2.23, below the estimated fair value of £2.94, indicating potential upside based on discounted cash flow analysis. Despite a significant drop in sales and net income for H1 2024, earnings are expected to grow significantly by 25.48% annually over the next three years, outpacing UK market growth rates. However, its dividend yield of 3.35% isn't well covered by free cash flows, posing sustainability concerns.

- Our earnings growth report unveils the potential for significant increases in Henry Boot's future results.

- Unlock comprehensive insights into our analysis of Henry Boot stock in this financial health report.

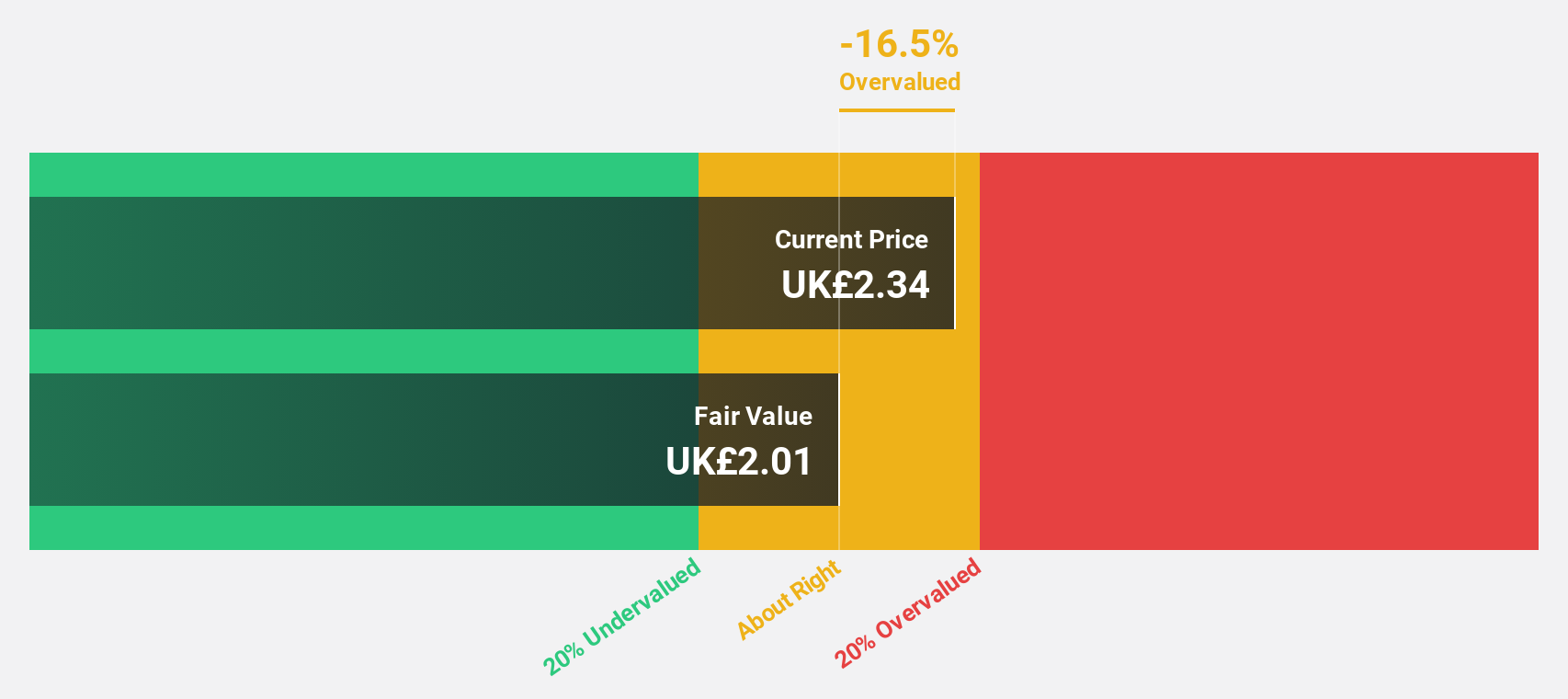

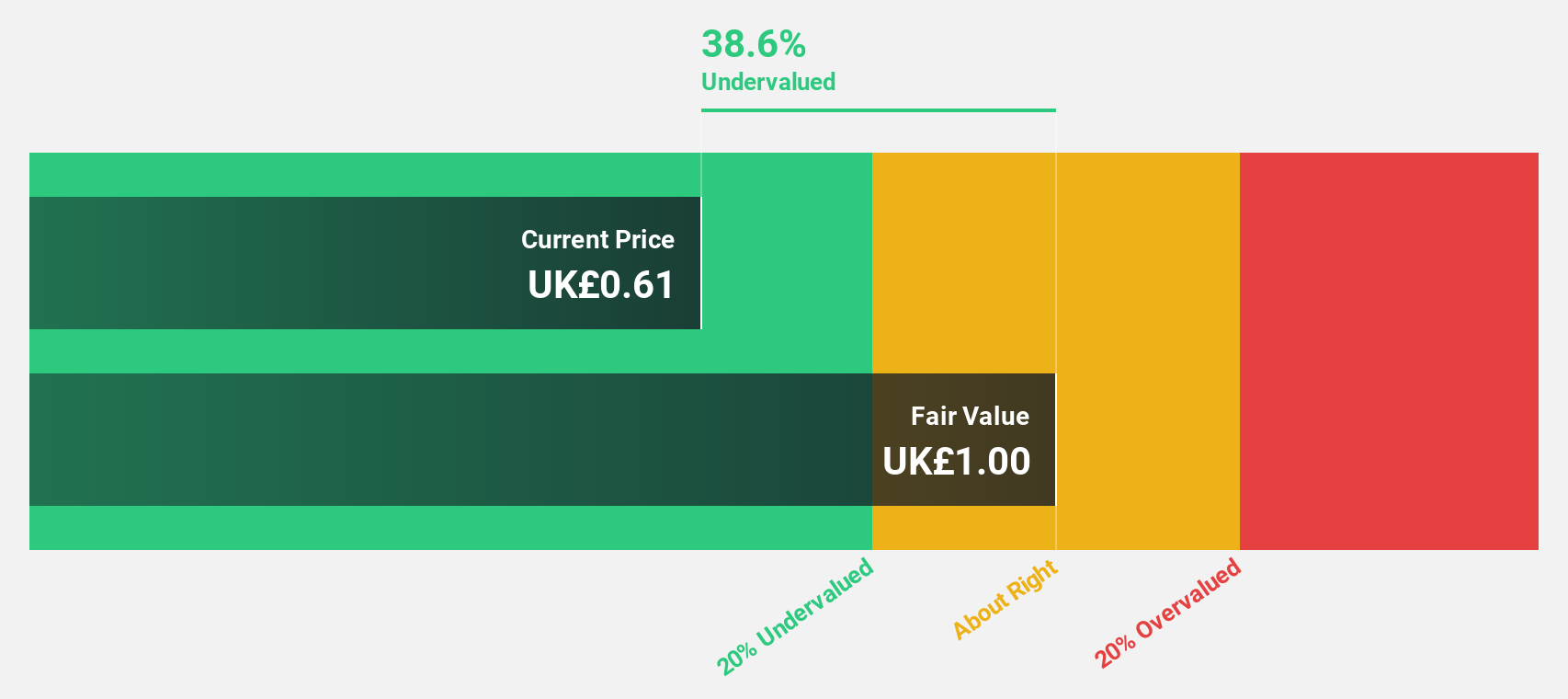

Foxtons Group (LSE:FOXT)

Overview: Foxtons Group plc is an estate agency offering services to the residential property market in the United Kingdom, with a market cap of £203.62 million.

Operations: The company generates revenue through three main segments: Sales (£41.84 million), Lettings (£103.78 million), and Financial Services (£9.10 million).

Estimated Discount To Fair Value: 38.6%

Foxtons Group is trading at £0.67, significantly below its estimated fair value of £1.09, suggesting it could be undervalued based on discounted cash flow analysis. Earnings are forecast to grow robustly at 33.2% annually, outpacing the UK market's growth rate of 14.9%. However, profit margins have decreased from 7.4% to 4.7% over the past year, and its future return on equity is anticipated to remain modest at 10.6%.

- Upon reviewing our latest growth report, Foxtons Group's projected financial performance appears quite optimistic.

- Dive into the specifics of Foxtons Group here with our thorough financial health report.

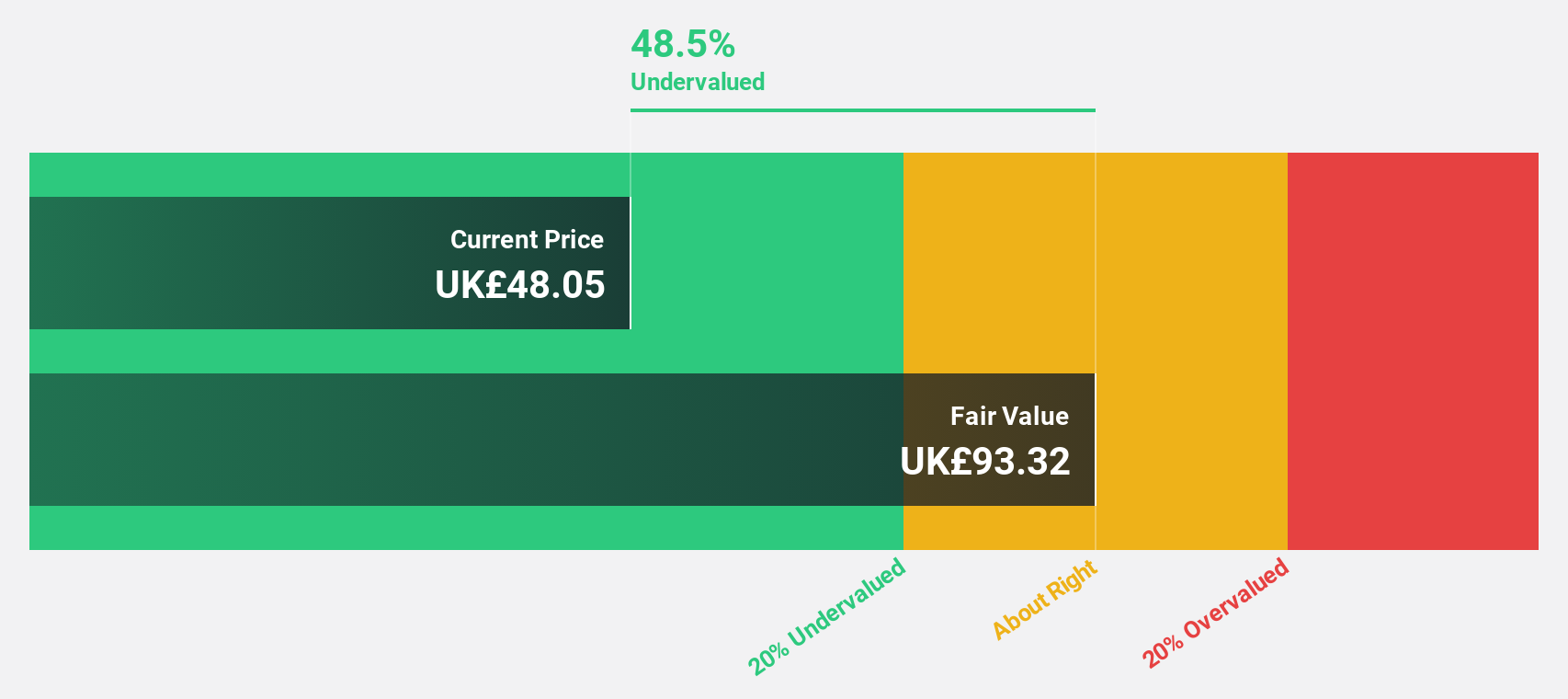

TBC Bank Group (LSE:TBCG)

Overview: TBC Bank Group PLC operates through its subsidiaries to offer banking, leasing, insurance, brokerage, and card processing services to both corporate and individual customers in Georgia, Azerbaijan, and Uzbekistan with a market cap of £1.69 billion.

Operations: The company generates its revenue from providing a range of financial services including banking, leasing, insurance, brokerage, and card processing across Georgia, Azerbaijan, and Uzbekistan.

Estimated Discount To Fair Value: 48.4%

TBC Bank Group is trading at £30.65, well below its estimated fair value of £59.35, indicating potential undervaluation based on cash flows. The bank's earnings grew by 18.1% over the past year and are expected to grow annually by 17.4%, surpassing UK market averages. Revenue growth is forecasted at 20.5% per year, also outpacing the market significantly, though high bad loans (2.1%) and low allowance (76%) remain concerns for investors.

- Insights from our recent growth report point to a promising forecast for TBC Bank Group's business outlook.

- Get an in-depth perspective on TBC Bank Group's balance sheet by reading our health report here.

Next Steps

- Delve into our full catalog of 56 Undervalued UK Stocks Based On Cash Flows here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:FOXT

Foxtons Group

An estate agency, provides services to the residential property market in the United Kingdom.

Reasonable growth potential with mediocre balance sheet.