- United Kingdom

- /

- Biotech

- /

- LSE:GNS

Exploring Undervalued Small Caps With Insider Buying In United Kingdom October 2024

Reviewed by Simply Wall St

As the United Kingdom's major indices, including the FTSE 100 and FTSE 250, face downward pressure due to weak trade data from China and broader global economic concerns, investors are increasingly turning their attention to small-cap stocks. In such a challenging environment, identifying undervalued small caps with insider buying can be an appealing strategy for those looking to uncover potential opportunities in a market where larger companies are struggling against international headwinds.

Top 10 Undervalued Small Caps With Insider Buying In The United Kingdom

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Senior | 18.2x | 0.6x | 37.42% | ★★★★★★ |

| Bytes Technology Group | 21.9x | 5.6x | 12.39% | ★★★★★☆ |

| NWF Group | 8.3x | 0.1x | 38.24% | ★★★★★☆ |

| John Wood Group | NA | 0.2x | 38.67% | ★★★★★☆ |

| Genus | 175.4x | 2.1x | 6.10% | ★★★★★☆ |

| J D Wetherspoon | 16.0x | 0.4x | 5.93% | ★★★★★☆ |

| Headlam Group | NA | 0.2x | 27.28% | ★★★★★☆ |

| Optima Health | NA | 1.3x | 37.58% | ★★★★☆☆ |

| Robert Walters | 43.2x | 0.3x | 40.24% | ★★★☆☆☆ |

| Marlowe | NA | 0.7x | 42.22% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

Restore (AIM:RST)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Restore is a company that provides secure lifecycle services and digital & information management solutions, with a market cap of £0.57 billion.

Operations: The company's revenue is primarily derived from Secure Lifecycle Services (£104.4 million) and Digital & Information Management (£172.5 million). The gross profit margin has exhibited fluctuations, with a recent figure of 42.90% as of June 2024. Operating expenses have consistently been a significant portion of costs, impacting net income margins over time.

PE: 94.8x

Restore, a UK-based company, has shown insider confidence with Charles Skinner purchasing 100,000 shares for £280,000 in July 2024. Despite high-risk external funding and large one-off items affecting earnings quality, the company reported a significant turnaround with net income of £6.4 million for H1 2024 compared to a substantial loss last year. An interim dividend increase to 2 pence per share reflects potential growth prospects amid recent executive changes and anticipated annual earnings growth of nearly 49%.

- Click here to discover the nuances of Restore with our detailed analytical valuation report.

Assess Restore's past performance with our detailed historical performance reports.

YouGov (AIM:YOU)

Simply Wall St Value Rating: ★★★★☆☆

Overview: YouGov is a global online market research and data analytics company, with operations focused on providing data products and services, and has a market capitalization of approximately £1.45 billion.

Operations: Revenue primarily comes from data products, with a significant segment adjustment noted. The gross profit margin has shown an upward trend, reaching 85.63% by January 2024. Operating expenses are substantial, with general and administrative costs being a major component.

PE: 25.0x

YouGov, a UK-based company with a history of volatile share prices over the past three months, faces challenges due to its reliance on higher-risk external borrowing. Despite this, earnings are projected to grow at 28.76% annually. Recent financials show sales rising to £335.3 million for the year ending July 31, 2024, but a net loss of £2.4 million was reported compared to last year's profit of £34.5 million. The appointment of Marc Ryan as Chief Product Officer could enhance their product offerings and strategic direction moving forward.

- Get an in-depth perspective on YouGov's performance by reading our valuation report here.

Gain insights into YouGov's historical performance by reviewing our past performance report.

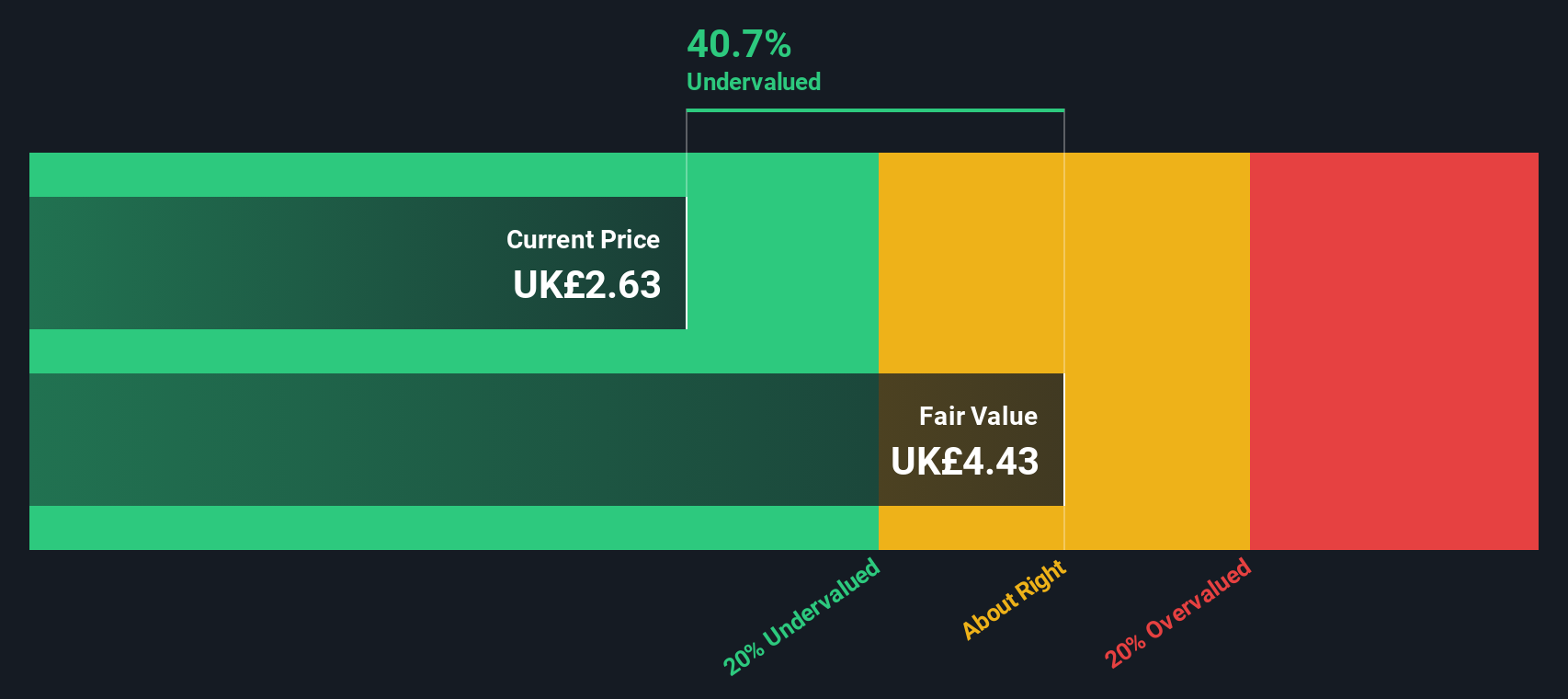

Genus (LSE:GNS)

Simply Wall St Value Rating: ★★★★★☆

Overview: Genus is a global leader in animal genetics, specializing in the development and commercialization of advanced breeding programs for livestock, with a market cap of approximately £1.82 billion.

Operations: Genus generates revenue primarily from its Genus PIC and Genus ABS segments, with recent quarterly revenues reaching £668.80 million. The gross profit margin has varied significantly over the years, peaking at 53.78% in December 2014 and more recently recorded at 38.17% in June 2024. Operating expenses have consistently included substantial R&D investments, reaching £93.30 million by September 2023, impacting the net income margin which was noted at a low of 1.18% in June and October of 2024 due to increased non-operating expenses.

PE: 175.4x

Genus, a player in the UK market, has caught attention with its potential for growth despite recent challenges. The company faced a dip in net income to £7.9 million from £33.3 million last year, impacted by significant one-off items and lower profit margins at 1.2%. However, earnings are forecasted to grow by 37% annually, suggesting future prospects remain promising. Insider confidence is evident as key figures have been purchasing shares throughout the year, indicating belief in Genus's long-term strategy amidst executive transitions and consistent dividend affirmations.

- Dive into the specifics of Genus here with our thorough valuation report.

Examine Genus' past performance report to understand how it has performed in the past.

Seize The Opportunity

- Gain an insight into the universe of 29 Undervalued UK Small Caps With Insider Buying by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:GNS

Genus

Operates as an animal genetics company in North America, Latin America, the United Kingdom, rest of Europe, the Middle East, Russia, Africa, and Asia.

Reasonable growth potential and slightly overvalued.