- United Kingdom

- /

- Capital Markets

- /

- AIM:LDG

3 Penny Stocks On UK Exchange With Market Caps Up To £800M

Reviewed by Simply Wall St

The UK market has recently faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines influenced by weak trade data from China, highlighting ongoing global economic uncertainties. Despite these broader market pressures, investors continue to seek opportunities in smaller or newer companies that may offer growth potential. Penny stocks, although an older term, remain relevant as they often represent affordable entry points into companies with strong financial foundations and potential for significant returns.

Top 10 Penny Stocks In The United Kingdom

| Name | Share Price | Market Cap | Financial Health Rating |

| ME Group International (LSE:MEGP) | £2.115 | £796.86M | ★★★★★★ |

| Begbies Traynor Group (AIM:BEG) | £0.926 | £146.07M | ★★★★★★ |

| Secure Trust Bank (LSE:STB) | £3.52 | £67.13M | ★★★★☆☆ |

| Ultimate Products (LSE:ULTP) | £1.16 | £99.11M | ★★★★★★ |

| Luceco (LSE:LUCE) | £1.31 | £202.04M | ★★★★★☆ |

| Stelrad Group (LSE:SRAD) | £1.35 | £171.93M | ★★★★★☆ |

| Next 15 Group (AIM:NFG) | £3.85 | £382.91M | ★★★★☆☆ |

| Integrated Diagnostics Holdings (LSE:IDHC) | $0.4395 | $255.49M | ★★★★★★ |

| Foresight Group Holdings (LSE:FSG) | £4.12 | £472M | ★★★★★★ |

| Impax Asset Management Group (AIM:IPX) | £2.45 | £313.05M | ★★★★★★ |

Click here to see the full list of 472 stocks from our UK Penny Stocks screener.

Let's take a closer look at a couple of our picks from the screened companies.

Logistics Development Group (AIM:LDG)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Logistics Development Group plc is an investment company with a market cap of £77.34 million.

Operations: Logistics Development Group plc does not report any specific revenue segments.

Market Cap: £77.34M

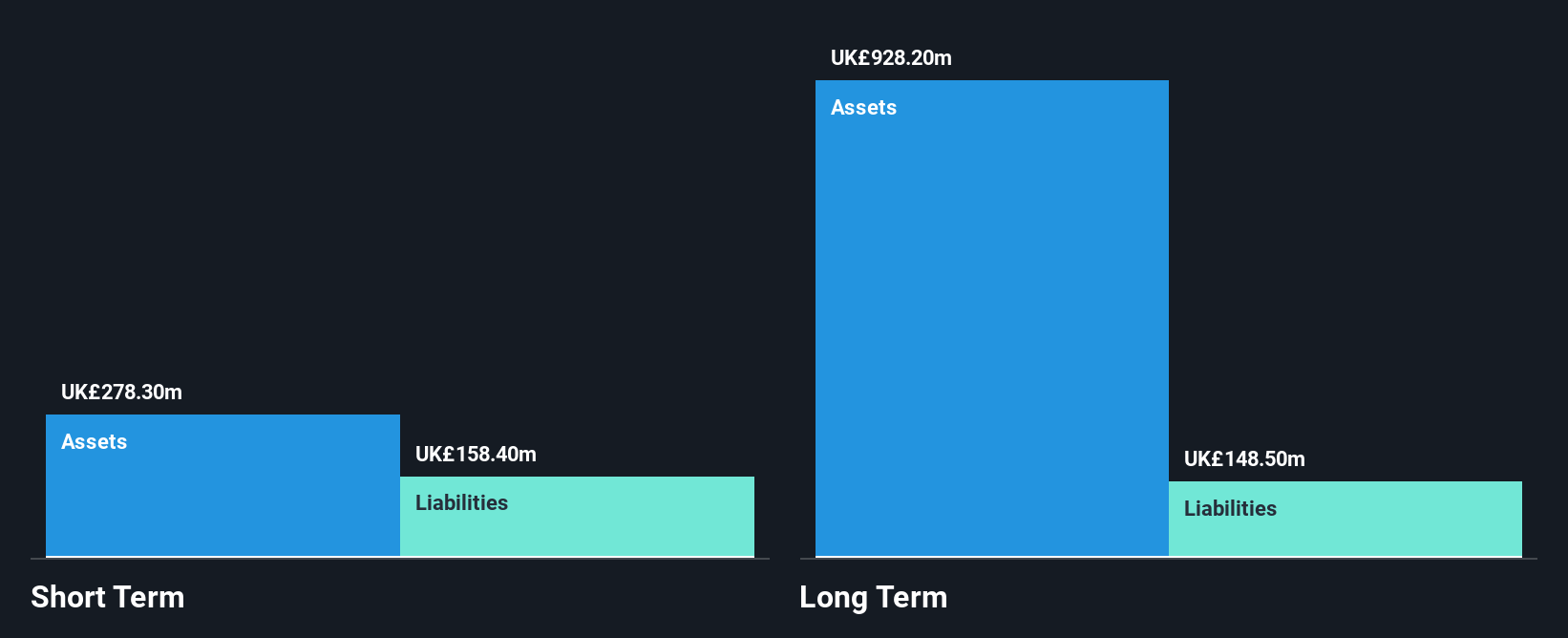

Logistics Development Group plc, with a market cap of £77.34 million, is currently pre-revenue and unprofitable, though it has reduced losses by 61% annually over five years. The company is debt-free and its short-term assets (£32.2 million) significantly exceed its short-term liabilities (£375,000). Recent board changes include the addition of experienced directors Colin Kingsnorth and Mark Butcher. Despite stable weekly volatility compared to last year, the stock remains highly volatile relative to UK peers. The board's average tenure suggests inexperience at 1.9 years, reflecting recent restructuring efforts within the company’s governance framework.

- Get an in-depth perspective on Logistics Development Group's performance by reading our balance sheet health report here.

- Assess Logistics Development Group's previous results with our detailed historical performance reports.

RWS Holdings (AIM:RWS)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: RWS Holdings plc offers technology-enabled language, content, and intellectual property services and has a market cap of £676.17 million.

Operations: The company's revenue is derived from its IP Services (£102.3 million), Language Services (£327.1 million), Regulated Industry (£146.5 million), and Language & Content Technology (£142.3 million) segments.

Market Cap: £676.17M

RWS Holdings plc, with a market cap of £676.17 million, has shown resilience by becoming profitable this year, reporting a net income of £47.5 million for the fiscal year ending September 30, 2024. The company recently launched Tridion Sites 10.1 to enhance digital content management capabilities for clients like Emirates and KONE. Despite a volatile share price and low return on equity at 5.3%, RWS's debt is well-managed with operating cash flow covering it by over 100%. However, its dividend yield of 6.79% isn't fully supported by earnings or free cash flows, indicating potential sustainability concerns.

- Take a closer look at RWS Holdings' potential here in our financial health report.

- Review our growth performance report to gain insights into RWS Holdings' future.

Irish Continental Group (LSE:ICGC)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Irish Continental Group plc is a maritime transport company with a market cap of £735.68 million.

Operations: The company generates revenue from its Ferries segment, which accounts for €430.1 million, and its Container and Terminal segment, contributing €195.8 million.

Market Cap: £735.68M

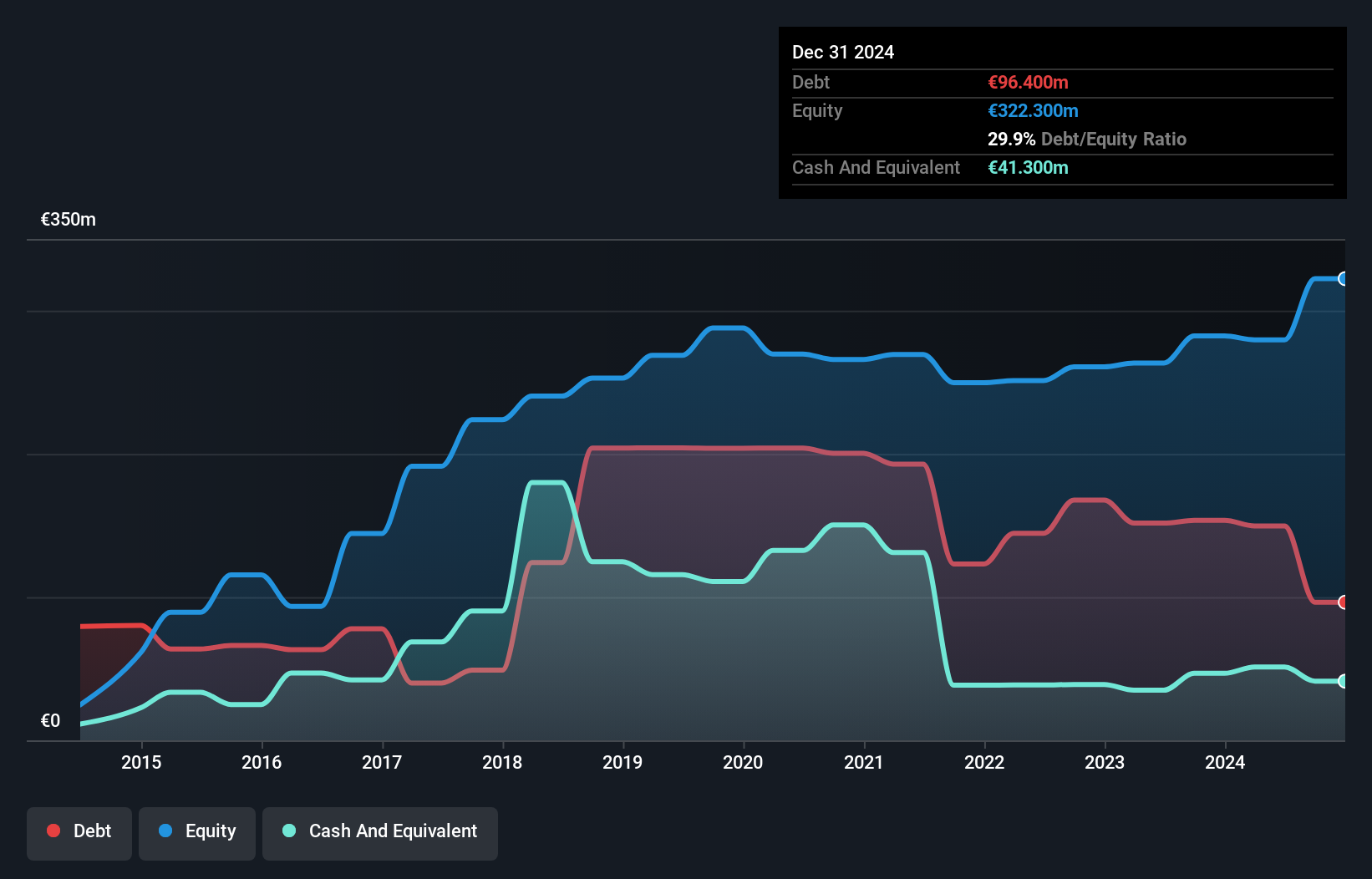

Irish Continental Group plc, with a market cap of £735.68 million, has demonstrated financial stability through its diverse revenue streams from the Ferries (€430.1 million) and Container and Terminal (€195.8 million) segments. The company boasts high-quality earnings with a return on equity of 22.3%, reflecting robust profitability despite an unstable dividend track record. Its debt management is commendable, with interest payments well covered by EBIT at 10 times coverage and operating cash flow covering 80.7% of its debt, though short-term assets fall short in covering both short- and long-term liabilities. Trading below estimated fair value enhances its appeal among penny stocks.

- Navigate through the intricacies of Irish Continental Group with our comprehensive balance sheet health report here.

- Gain insights into Irish Continental Group's future direction by reviewing our growth report.

Summing It All Up

- Discover the full array of 472 UK Penny Stocks right here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:LDG

Adequate balance sheet low.

Market Insights

Community Narratives