- United Kingdom

- /

- Healthcare Services

- /

- LSE:IDHC

Undiscovered Gems In The UK And 2 Other Promising Small Caps With Strong Potential

Reviewed by Simply Wall St

As the United Kingdom's FTSE 100 index faces downward pressure amid weak trade data from China and broader global economic uncertainties, the spotlight turns to smaller companies that may offer untapped potential. In this challenging environment, identifying small-cap stocks with strong fundamentals and growth prospects can be a strategic approach for investors seeking opportunities beyond the traditional blue-chip landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| M&G Credit Income Investment Trust | NA | 17.28% | 15.80% | ★★★★★★ |

| Andrews Sykes Group | NA | 2.15% | 4.93% | ★★★★★★ |

| London Security | 0.22% | 10.13% | 7.75% | ★★★★★★ |

| B.P. Marsh & Partners | NA | 29.42% | 31.34% | ★★★★★★ |

| Octopus Renewables Infrastructure Trust | NA | -28.79% | -14.27% | ★★★★★★ |

| VH Global Energy Infrastructure | NA | 18.30% | 20.03% | ★★★★★★ |

| Rights and Issues Investment Trust | NA | -3.68% | -4.07% | ★★★★★★ |

| FW Thorpe | 5.89% | 11.97% | 12.07% | ★★★★★☆ |

| BBGI Global Infrastructure | 0.02% | 3.08% | 6.85% | ★★★★★☆ |

| Goodwin | 52.21% | 9.26% | 13.12% | ★★★★★☆ |

Here's a peek at a few of the choices from the screener.

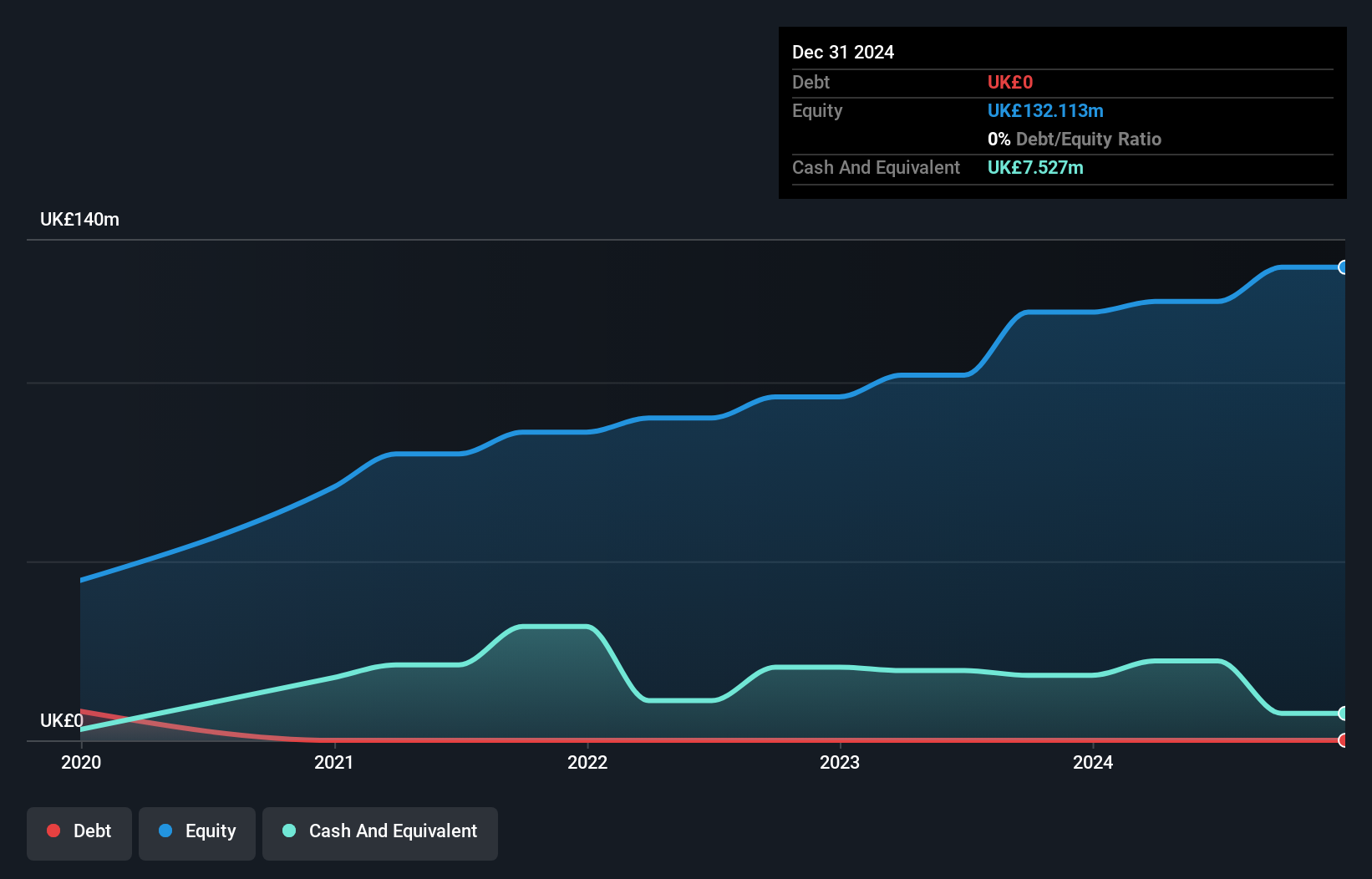

Central Asia Metals (AIM:CAML)

Simply Wall St Value Rating: ★★★★★★

Overview: Central Asia Metals plc, with a market cap of £292.28 million, operates as a base metals producer through its subsidiaries.

Operations: The company generates revenue from its Sasa and Kounrad operations, with contributions of $81.49 million and $117.70 million, respectively.

Central Asia Metals, a nimble player in the metals and mining sector, has shown impressive financial resilience. Over the past year, its earnings skyrocketed by 2874.7%, outpacing industry peers who faced a -0.3% growth rate. The company is trading at 71% below its estimated fair value, suggesting potential undervaluation. With debt to equity reduced from 38% to just 0.1% over five years and cash exceeding total debt, financial stability seems assured. Recent leadership changes see Gavin Ferrar stepping up as CEO after serving as CFO for six years, possibly indicating strategic continuity in management approach.

- Navigate through the intricacies of Central Asia Metals with our comprehensive health report here.

Examine Central Asia Metals' past performance report to understand how it has performed in the past.

Elixirr International (AIM:ELIX)

Simply Wall St Value Rating: ★★★★★★

Overview: Elixirr International plc operates as a management consultancy firm offering services in the United Kingdom, the United States, and internationally, with a market capitalization of £327.44 million.

Operations: Elixirr International generates revenue primarily from management consulting services, amounting to £97.37 million. The company's financial performance can be assessed through its net profit margin, which reflects its profitability after accounting for all expenses.

Elixirr International, a dynamic player in the professional services sector, showcases impressive growth with earnings rising 32.8% over the past year, outpacing industry averages. Despite recent significant insider selling and shareholder dilution from a £25 million equity offering at £6.5 per share, Elixirr remains debt-free and boasts high-quality earnings. Notably, its free cash flow surged to £20.31 million by mid-2024 from just £2.68 million in 2019, indicating robust financial health. Leadership transitions are underway with Graham Busby stepping up as Deputy CEO while maintaining his role in acquisitions—a strategic move likely enhancing future growth prospects.

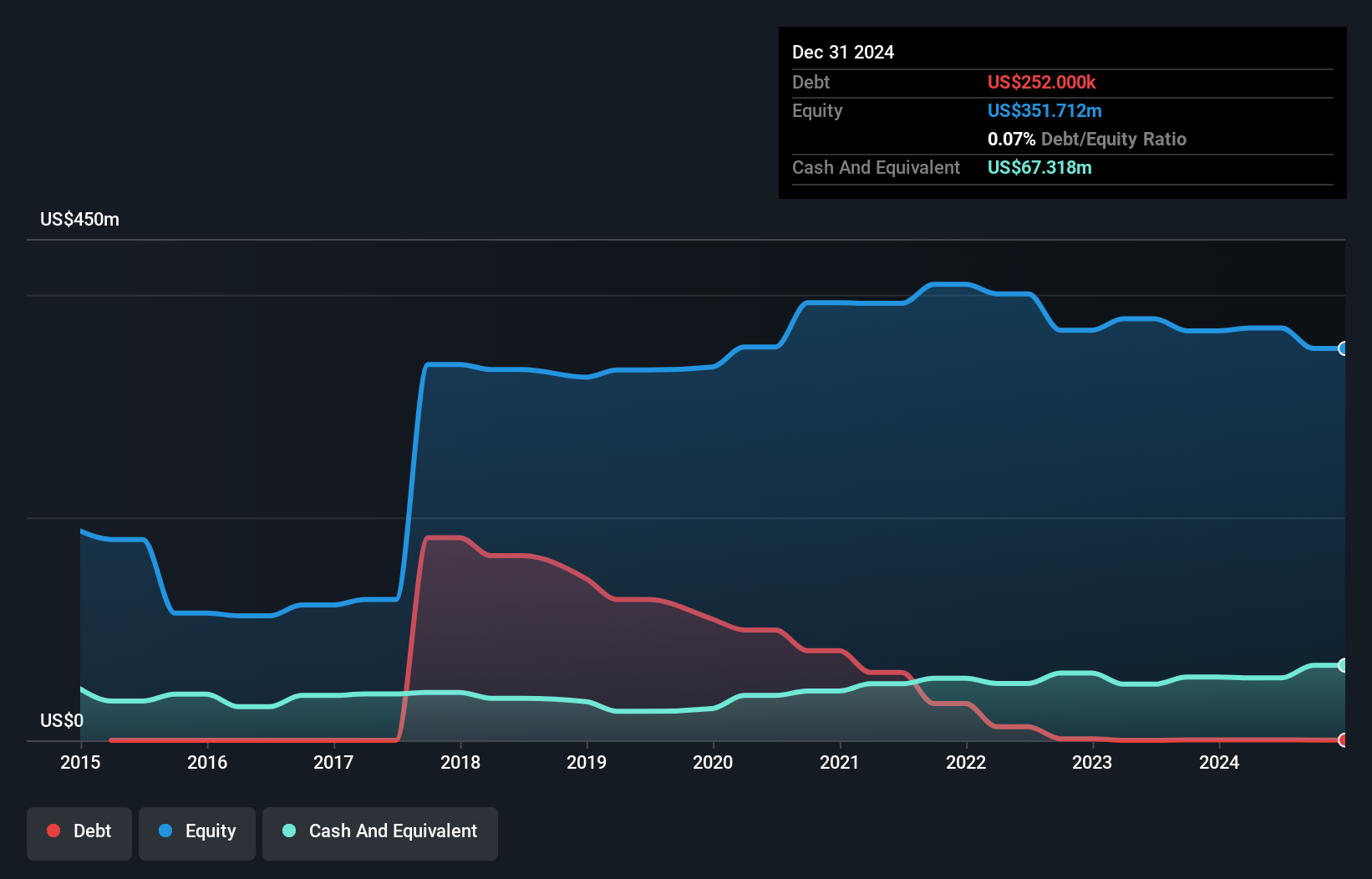

Integrated Diagnostics Holdings (LSE:IDHC)

Simply Wall St Value Rating: ★★★★★★

Overview: Integrated Diagnostics Holdings plc is a consumer healthcare company that offers a range of medical diagnostics services to patients, with a market cap of $266.25 million.

Operations: Integrated Diagnostics Holdings generates revenue primarily through its medical diagnostics services. The company has a market capitalization of $266.25 million.

Integrated Diagnostics Holdings (IDHC) stands out with its robust financial health and significant growth trajectory. The company's interest payments are comfortably covered by EBIT, which is 18 times the required amount, highlighting strong operational efficiency. Over the past year, IDHC's earnings skyrocketed by 139%, far surpassing the healthcare industry's average growth of 15%. This impressive performance is coupled with a reduction in its debt-to-equity ratio from 5.3% to 2.6% over five years, indicating prudent financial management. Trading at a substantial discount of 78% below estimated fair value, IDHC seems poised for continued expansion and offers an attractive prospect for investors seeking undervalued opportunities in the healthcare sector.

Summing It All Up

- Unlock more gems! Our UK Undiscovered Gems With Strong Fundamentals screener has unearthed 67 more companies for you to explore.Click here to unveil our expertly curated list of 70 UK Undiscovered Gems With Strong Fundamentals.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:IDHC

Integrated Diagnostics Holdings

A consumer healthcare company, provides various medical diagnostics services to patients.

Outstanding track record with flawless balance sheet.