How the Recent 4.9% Drop Impacts Compagnie de l'Odet's Valuation in 2025

Reviewed by Simply Wall St

Thinking about whether to hold or buy more Compagnie de l'Odet stock this year? You are definitely not alone. Over the past few years, this French conglomerate has kept investors on their toes, thanks in part to its quietly impressive long-term story. Despite wider market swings and shifting investor sentiment, the stock has delivered a remarkable 108.2% growth over the last five years. But before you get too comfortable, the ride has not been all smooth. The past year has seen shares drop by 12.0%, followed by a 13.1% decline since January. Even in the last month, the price has slipped 4.9%, suggesting some nerves or perhaps a shift in how investors are reading the current macro environment.

When you take a closer look, these recent moves might not reflect deeper trouble for the business itself, but could be tied to ongoing global market volatility and evolving risk appetites across Europe. It is not uncommon to see stocks like Compagnie de l'Odet ebb and flow as investors reassess opportunities and risks in sectors that the company is involved in. The key question now is whether these lower prices mean the shares are attractively valued, risky, or just misunderstood.

To help answer that, we use a value score, which ranges from 0 to 6, with one point for every undervalued box the company checks. Right now, Compagnie de l'Odet lands a score of just 2, meaning it passes two out of six undervaluation tests. But how does that score hold up when we look at the different ways analysts assess value? Let us break down the main valuation methods and at the end, I will share a more holistic way to use this information to guide your investment decisions.

Compagnie de l'Odet scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.Approach 1: Compagnie de l'Odet Discounted Cash Flow (DCF) Analysis

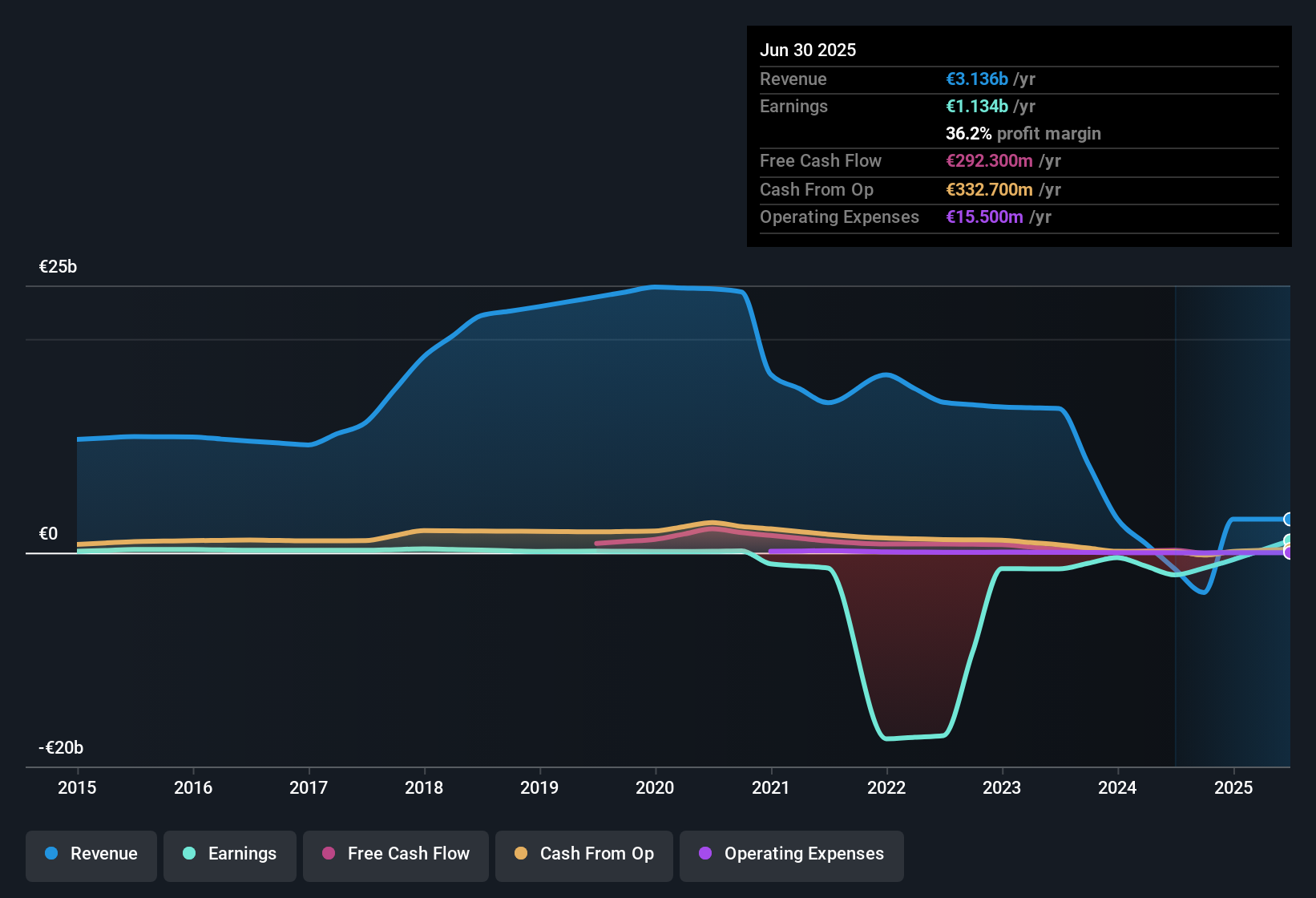

The Discounted Cash Flow (DCF) model estimates a business's value by projecting its future cash flows and discounting them back to today's value. This approach is widely used to capture how much value future earnings may add, while adjusting for the risk and time value of money. For Compagnie de l'Odet, the analysis relies on the company's Free Cash Flow (FCF), which is currently €74.45 million.

Analysts use recent FCF growth, and for the years ahead, projections show annual growth rates tapering from 5.88% to just over 2%. Looking further ahead, estimated FCF in 2035 reaches about €101.85 million. Most long-term projections beyond 2029 are extrapolated from earlier analyst forecasts. This allows for a more complete picture of potential value, even as direct analyst estimates typically only extend about five years into the future.

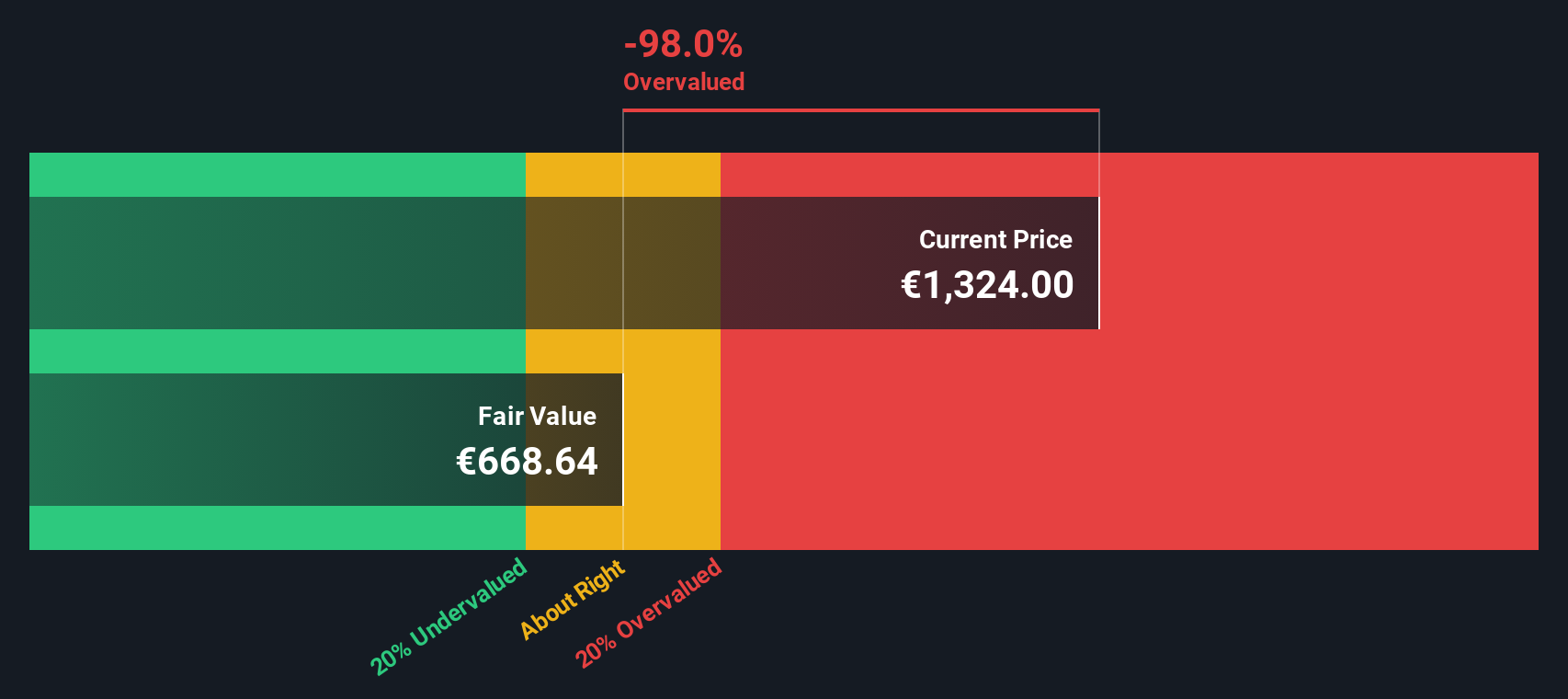

Based on these calculations, Compagnie de l'Odet's estimated intrinsic value per share is €417.53. However, this suggests the stock is currently trading at a premium, since the DCF result implies shares are 232.4% overvalued relative to their fundamentals.

Result: OVERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Compagnie de l'Odet.

Approach 2: Compagnie de l'Odet Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is a classic and widely trusted metric for valuing profitable companies like Compagnie de l'Odet. By comparing a company’s share price to its earnings per share, investors can quickly gauge how much they are paying for each euro of profit. This metric is especially useful when companies have steady profitability, as it allows for apples-to-apples comparisons within and across industries.

Growth expectations and risk levels play a crucial role in determining what a “normal” or “fair” PE ratio should be. Generally, firms with higher expected earnings growth or lower risk warrant a higher PE, while those facing more uncertainty or slower growth usually trade on a lower multiple.

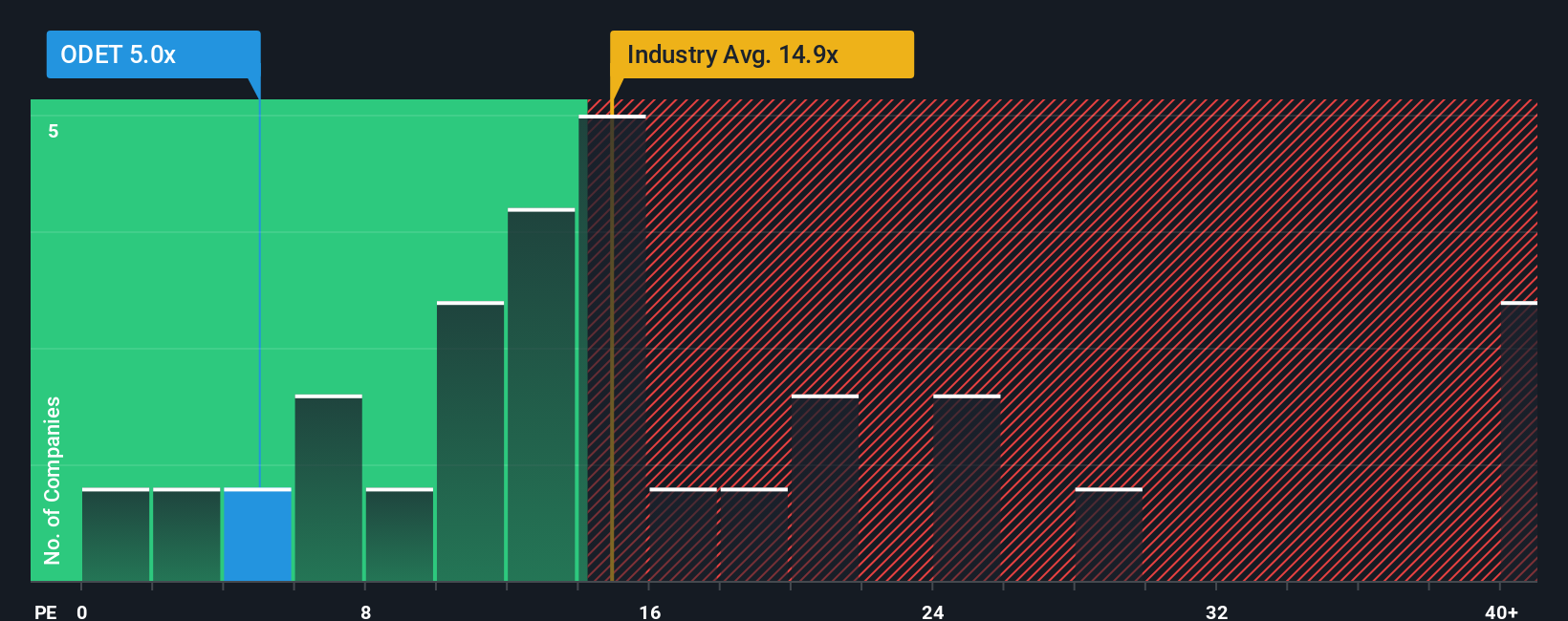

At the moment, Compagnie de l'Odet’s PE ratio stands at 5.18x. This is significantly below the logistics industry average of 16.18x and also well under its peer group’s average of 49.43x. At first glance, such a discount might tempt value-oriented investors as it may signal a bargain relative to similar businesses.

This is where Simply Wall St’s “Fair Ratio” comes in. Unlike industry or peer comparisons, the Fair Ratio goes beyond the surface by incorporating company-specific factors such as historical earnings growth, profit margins, risk profile, industry trends, and market capitalization to suggest what a justifiable multiple should be at the present time. This tailored approach helps avoid the pitfalls of using generic benchmarks that might not fully reflect the company’s unique strengths and circumstances.

If the difference between the actual PE and the Fair Ratio is only marginal, then the stock is trading close to its intrinsic value on this measure. In this case, the comparison signals that Compagnie de l'Odet shares appear to be fairly valued based on their earnings, growth outlook, and risk factors.

Result: ABOUT RIGHT

Upgrade Your Decision Making: Choose your Compagnie de l'Odet Narrative

Earlier, we mentioned there is a better way to understand valuation, so let us introduce Narratives. A Narrative is simply your personal story or perspective for a company, combining your view on its future with estimates of revenue, earnings, and margins to set what you believe is a fair value.

This approach connects the company’s background and outlook directly to its numbers, creating a clear link from the business story to a financial forecast and ultimately to a justifiable price. Narratives are easy to create and share on Simply Wall St’s Community page, used by millions of investors worldwide, making them highly accessible and interactive.

With Narratives, you can decide when to buy or sell by directly comparing your Fair Value to the current Share Price. They are also automatically updated as new information, like fresh news or earnings releases, appears in the market, keeping your view current without extra work.

For example, two investors might see Compagnie de l'Odet very differently, with one Narrative forecasting strong recovery and a higher fair value, while another expects further decline and a much lower fair value.

Do you think there's more to the story for Compagnie de l'Odet? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:ODET

Compagnie de l'Odet

Engages in energy, communication, and industry business in France, Africa, the Americas, the Asia-Pacific, and other European countries.

Excellent balance sheet with acceptable track record.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

CS Disco Stock: Legal AI Is Moving From Efficiency Tool to Competitive Necessity

Cheap if able to sustain revenue, and a potential bargain if able to turn store openings into revenue growth

Butler National (Buks) outperforms.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)