Advertisement

- France

- /

- Entertainment

- /

- ENXTPA:ALCHI

Alchimie S.A.S. (EPA:ALCHI) Analysts Just Slashed This Year's Revenue Estimates By 16%

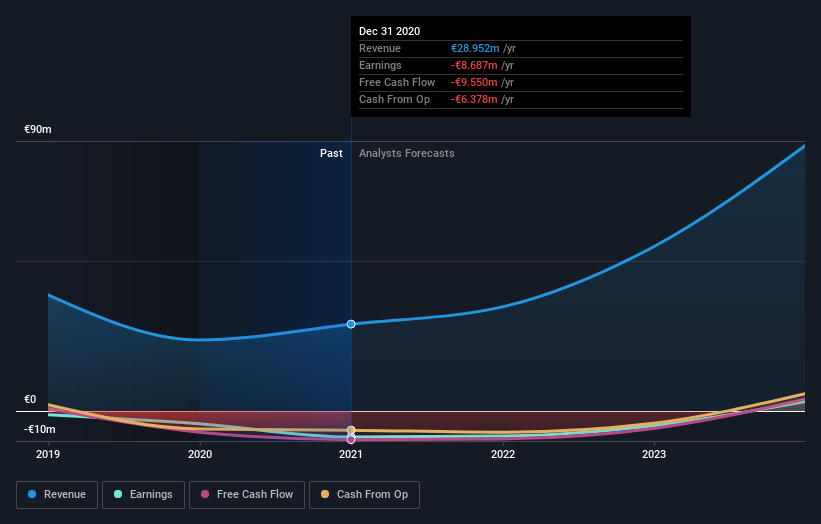

One thing we could say about the analysts on Alchimie S.A.S. (EPA:ALCHI) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. Revenue estimates were cut sharply as analysts signalled a weaker outlook - perhaps a sign that investors should temper their expectations as well.

Following the downgrade, the current consensus from AlchimieS' two analysts is for revenues of €35m in 2021 which - if met - would reflect a notable 20% increase on its sales over the past 12 months. The loss per share is anticipated to greatly reduce in the near future, narrowing 22% to €1.91. Yet before this consensus update, the analysts had been forecasting revenues of €41m and losses of €1.84 per share in 2021. Ergo, there's been a clear change in sentiment, with the analysts administering a notable cut to this year's revenue estimates, while at the same time increasing their loss per share forecasts.

View our latest analysis for AlchimieS

The consensus price target fell 13% to €25.75, with the analysts clearly concerned about the company following the weaker revenue and earnings outlook. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. There are some variant perceptions on AlchimieS, with the most bullish analyst valuing it at €26.00 and the most bearish at €25.50 per share. Still, with such a tight range of estimates, it suggests the analysts have a pretty good idea of what they think the company is worth.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the AlchimieS' past performance and to peers in the same industry. The period to the end of 2021 brings more of the same, according to the analysts, with revenue forecast to display 20% growth on an annualised basis. That is in line with its 22% annual growth over the past year. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 6.1% per year. So it's pretty clear that AlchimieS is forecast to grow substantially faster than its industry.

The Bottom Line

The most important thing to take away is that analysts increased their loss per share estimates for this year. While analysts did downgrade their revenue estimates, these forecasts still imply revenues will perform better than the wider market. Furthermore, there was a cut to the price target, suggesting that the latest news has led to more pessimism about the intrinsic value of the business. Overall, given the drastic downgrade to this year's forecasts, we'd be feeling a little more wary of AlchimieS going forwards.

Still, the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for AlchimieS going out as far as 2023, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

When trading AlchimieS or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ENXTPA:ALCHI

Alchimie

Operates as an OTT video streaming platform in France and internationally.

Low and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.8% undervalued

RO

Community Contributor