Is adidas Stock Pricing In Its Recovery After Direct to Consumer Pivot?

Reviewed by Bailey Pemberton

- Thinking about whether adidas is a bargain or a value trap at today’s price? You are not alone, and this breakdown is designed to help you see what the market might be missing.

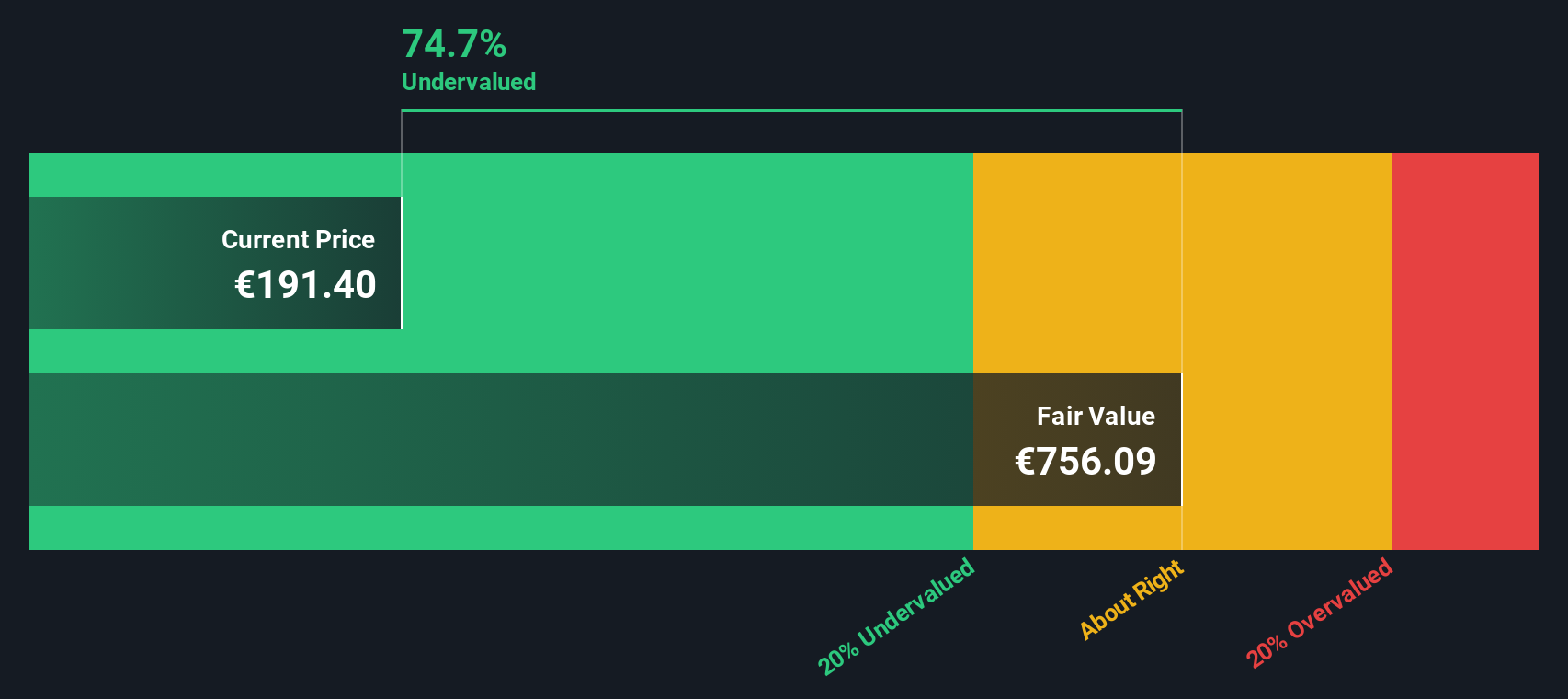

- Despite being up 1.0% over the last week and 2.3% over the last month, the stock is still down 31.8% year to date and 32.6% over the past year, a combination that often signals either deep value or lingering risk.

- Recent headlines have focused on adidas pushing harder into direct to consumer channels and refreshing key franchises like the Samba and Gazelle, aiming to keep the brand culturally relevant. At the same time, investors are watching how the company navigates cost pressures and competition from Nike and newer lifestyle players, all of which feeds into sentiment and those volatile price swings.

- On our framework, adidas currently scores a 4/6 valuation check, suggesting it looks undervalued on several metrics but not across the board. Next, we will unpack how different valuation approaches treat the stock and why there may be an even better way to judge its true worth by the end of this article.

Approach 1: adidas Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and discounting those cash flows back to today in € terms. For adidas, the model used is a 2 Stage Free Cash Flow to Equity approach, which starts from the latest twelve month Free Cash Flow of about €0.36 billion and then applies analyst forecasts and longer term projections.

Analysts currently expect adidas to grow Free Cash Flow substantially, with projections rising to roughly €3.03 billion by 2029. Beyond the explicit analyst horizon, Simply Wall St extrapolates further cash flows, gradually tapering growth as the business matures. These future cash flows, once discounted to today, imply an intrinsic value of about €276.85 per share.

Compared to the current share price, this DCF suggests adidas is trading at about a 41.7% discount, which indicates the market may be underestimating the company’s ability to convert brand strength and operational improvements into cash generation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests adidas is undervalued by 41.7%. Track this in your watchlist or portfolio, or discover 908 more undervalued stocks based on cash flows.

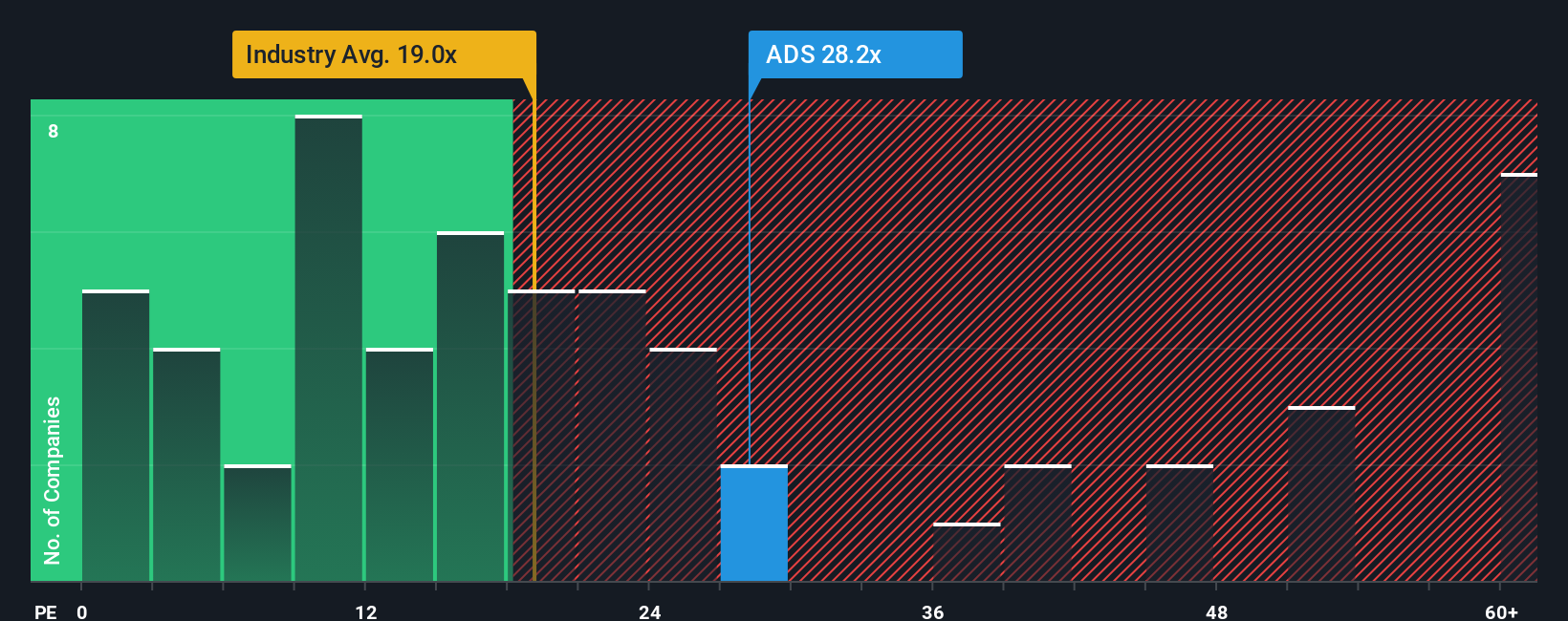

Approach 2: adidas Price vs Earnings

For a profitable brand like adidas, the Price to Earnings ratio is a practical way to gauge how much investors are willing to pay for each euro of current profits. Higher growth and lower risk usually justify a higher PE, while slower or less certain earnings should command a lower, more cautious multiple.

Right now, adidas trades on about 23.80x earnings, which is above the Luxury industry average of around 17.36x but below the peer group average of roughly 31.61x. To move beyond simple comparisons, Simply Wall St uses a proprietary Fair Ratio of 22.35x for adidas, which reflects its earnings growth outlook, industry positioning, profit margins, market cap and risk profile.

This Fair Ratio is more tailored than a blunt industry or peer benchmark because it adjusts for adidas specific fundamentals rather than assuming it should be priced like every other luxury or athletic name. With the current PE only modestly above the Fair Ratio, the market appears to be valuing adidas roughly in line with its risk and growth profile.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your adidas Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of adidas’ story with a concrete forecast and Fair Value on Simply Wall St’s Community page, where millions of investors share their perspectives.

A Narrative is your personal storyline for the company, where you spell out what you think will happen to adidas’ revenue, earnings and margins, and those assumptions are automatically turned into a financial forecast and Fair Value that you can compare to today’s share price to decide whether you see a buy or a sell.

Because Narratives are updated dynamically whenever new information arrives, like earnings results or major news, they help you quickly see whether your thesis still holds up or if it is time to revise your expectations.

For example, one adidas Narrative might lean bullish and anchor around a Fair Value closer to €280, while a more cautious Narrative might sit nearer €182. By comparing both to the current price you can decide which story you believe, or build your own in between.

Do you think there's more to the story for adidas? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:ADS

adidas

Designs, develops, produces, and markets a range of athletic and sports lifestyle products in Europe, Greater China, Japan, South Korea, Latin America, North America, and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Dollar general to grow

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026