Advertisement

- China

- /

- Basic Materials

- /

- SZSE:001296

Undiscovered Gems With Strong Fundamentals December 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a period of caution following the Federal Reserve's recent rate cut and tempered expectations for future reductions, small-cap stocks have been particularly impacted by broad-based declines. Despite these challenges, the U.S. economy shows resilience with strong consumer spending and job data, creating an environment where discerning investors may uncover stocks with robust fundamentals that remain underappreciated by the broader market. In such a landscape, identifying companies with solid financial health and growth potential becomes crucial for those seeking to capitalize on overlooked opportunities in the small-cap sector.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Resource Alam Indonesia | 2.66% | 30.36% | 43.87% | ★★★★★★ |

| Philippine Savings Bank | NA | 5.49% | 20.73% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Mandiri Herindo Adiperkasa | NA | 20.72% | 11.08% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Arab Insurance Group (B.S.C.) | NA | -59.20% | 20.33% | ★★★★★☆ |

| Eclatorq Technology | 37.47% | 8.43% | 18.41% | ★★★★★☆ |

| Chita Kogyo | 8.34% | 2.84% | 8.49% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Yuan Cheng CableLtd | 112.32% | 6.17% | 58.39% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

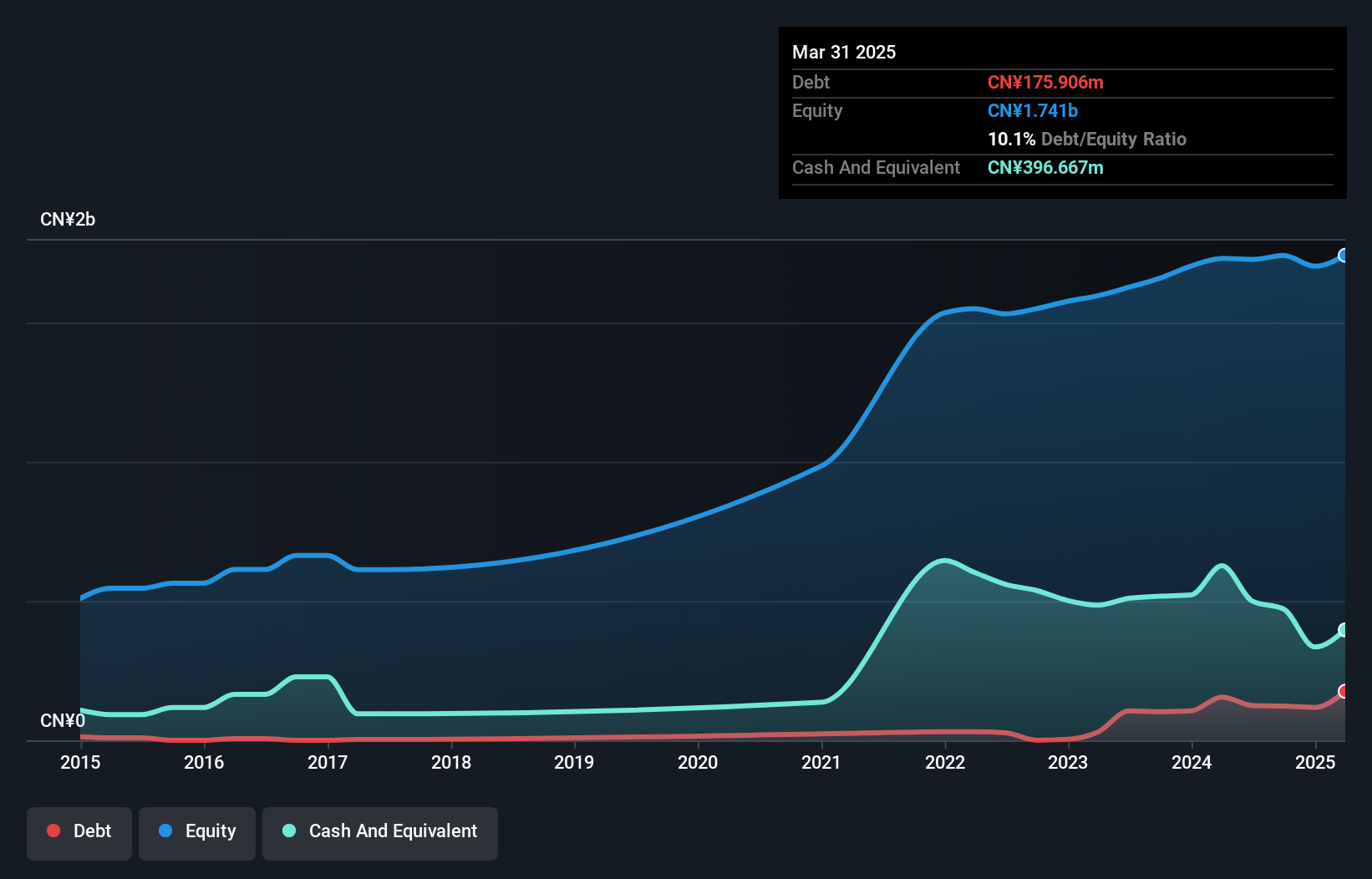

Chongqing Changjiang River Moulding Material (Group) (SZSE:001296)

Simply Wall St Value Rating: ★★★★★☆

Overview: Chongqing Changjiang River Moulding Material (Group) Co., Ltd. operates in the manufacturing sector and has a market capitalization of approximately CN¥2.69 billion.

Operations: The company generates revenue primarily through its manufacturing operations. It has a market capitalization of approximately CN¥2.69 billion.

Chongqing Changjiang River Moulding Material (Group) showcases a compelling mix of financial strength and growth potential. Over the past year, earnings grew by 17%, outpacing the Basic Materials industry which faced a -22.9% shift. The company trades at 25.7% below its estimated fair value, indicating potential undervaluation. Despite an increase in debt to equity ratio from 1.9% to 7% over five years, it holds more cash than total debt, suggesting robust financial health. Recent activities include repurchasing 977,746 shares for CNY 13.73 million and distributing dividends of CNY 2 per ten shares, reflecting shareholder-friendly policies.

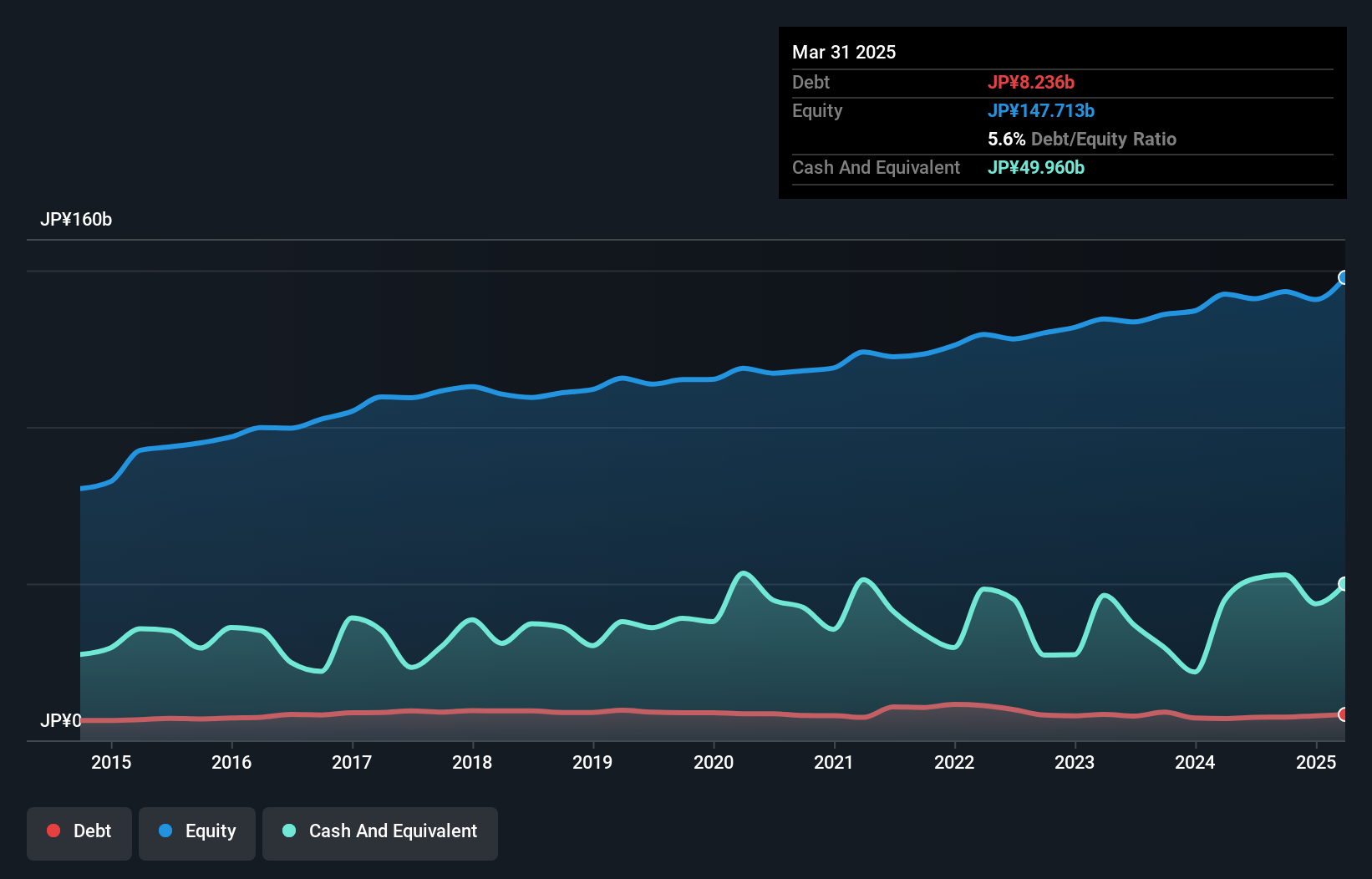

Yurtec (TSE:1934)

Simply Wall St Value Rating: ★★★★★★

Overview: Yurtec Corporation is a facility engineering company operating in Japan and internationally, with a market cap of ¥100.18 billion.

Operations: Yurtec generates revenue primarily from its facility engineering services in Japan and abroad. The company's net profit margin has been observed at 3.5% over the recent periods, highlighting its efficiency in managing costs relative to income.

Yurtec, a notable player in the construction sector, has shown a solid financial footing with its debt-to-equity ratio improving from 7.6% to 5.2% over five years and maintaining high-quality earnings. The company’s price-to-earnings ratio of 11.5x suggests it offers good value against the JP market average of 13.5x, though recent earnings growth at 17.2% lagged behind the industry’s 20.7%. Yurtec recently completed a share buyback totaling ¥4,510 million for approximately 4.23% of outstanding shares and increased its dividend to JPY 23 per share from JPY 14 last year, reflecting strong shareholder returns initiatives.

- Click here to discover the nuances of Yurtec with our detailed analytical health report.

Gain insights into Yurtec's historical performance by reviewing our past performance report.

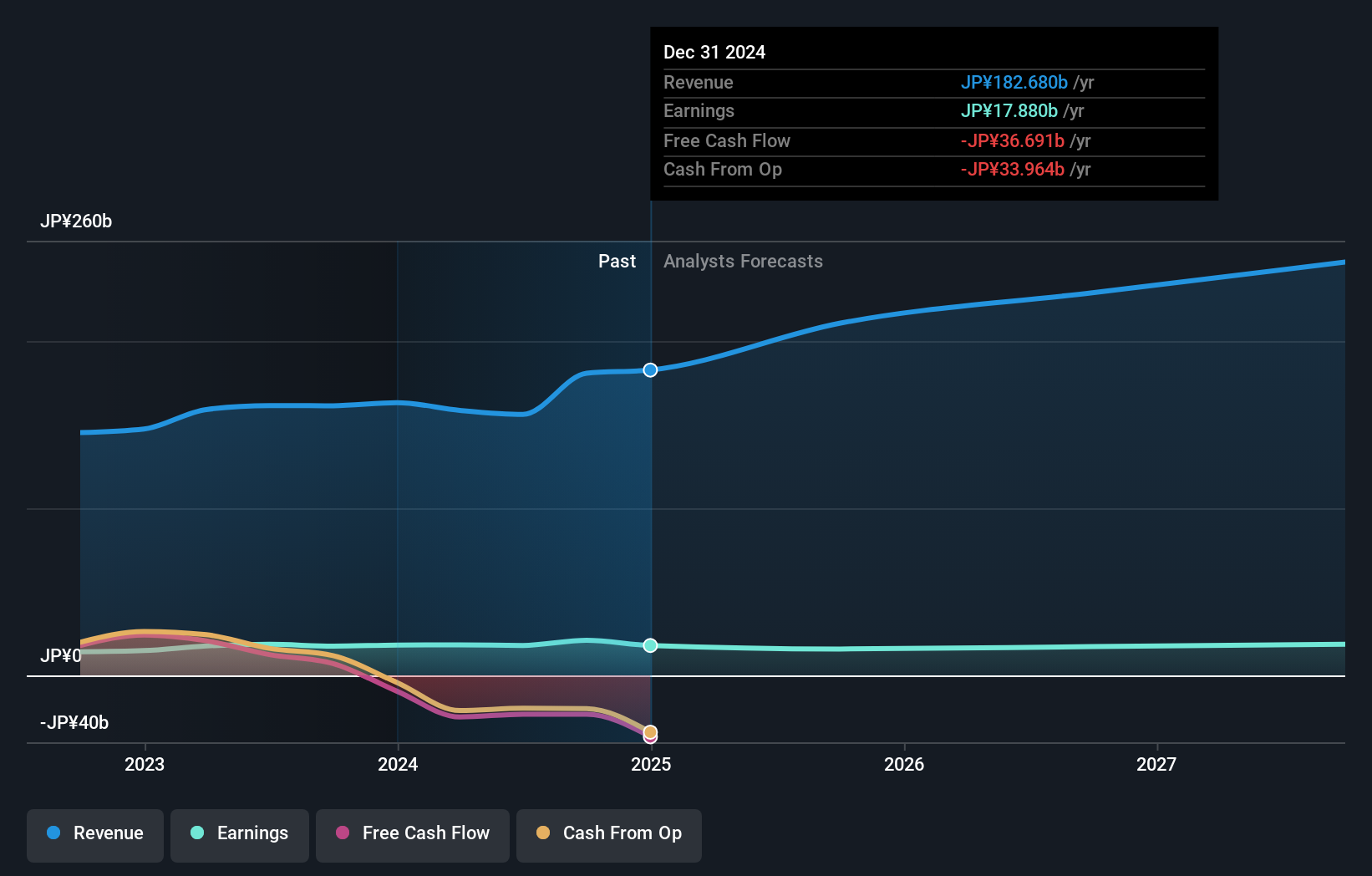

Pressance (TSE:3254)

Simply Wall St Value Rating: ★★★★★☆

Overview: Pressance Corporation operates in the real estate sector in Japan and has a market capitalization of approximately ¥135.54 billion.

Operations: The company generates revenue primarily from its real estate activities in Japan. It has a market capitalization of approximately ¥135.54 billion, reflecting its scale within the sector.

Pressance, a smaller player in the real estate sector, has demonstrated robust financial health with a net debt to equity ratio of 1.8%, which is considered satisfactory. Over the last five years, its debt to equity ratio has impressively decreased from 160.5% to 53.8%. The company exhibits strong earnings growth at 20% over the past year, surpassing its industry peers who saw a -3.2% change in earnings. With EBIT covering interest payments by 44 times, Pressance's profitability seems well-supported despite not being free cash flow positive currently. Revenue is anticipated to grow at an annual rate of approximately 10%.

- Take a closer look at Pressance's potential here in our health report.

Examine Pressance's past performance report to understand how it has performed in the past.

Seize The Opportunity

- Click this link to deep-dive into the 4625 companies within our Undiscovered Gems With Strong Fundamentals screener.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:001296

Chongqing Changjiang River Moulding Material (Group)

Chongqing Changjiang River Moulding Material (Group) Co., Ltd.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor