- China

- /

- Healthcare Services

- /

- SZSE:301239

Chengdu Bright Eye Hospital (SZSE:301239) Seems To Use Debt Quite Sensibly

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Chengdu Bright Eye Hospital Co., Ltd. (SZSE:301239) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Chengdu Bright Eye Hospital

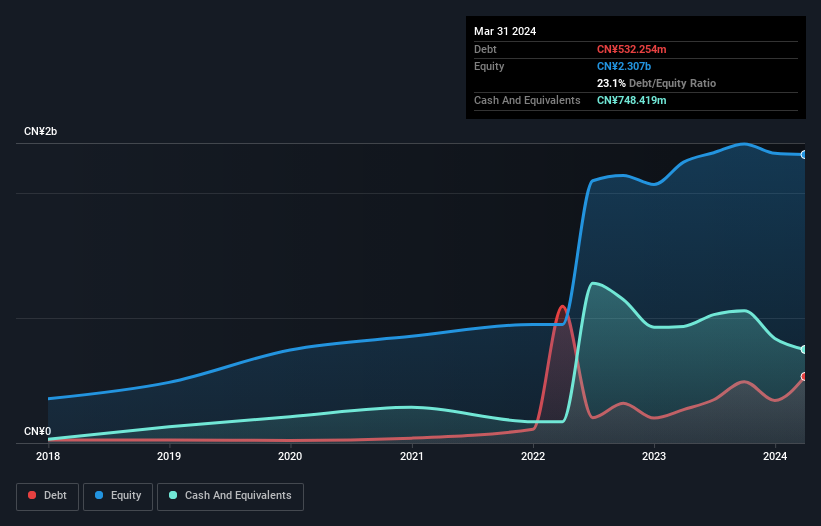

What Is Chengdu Bright Eye Hospital's Debt?

The image below, which you can click on for greater detail, shows that at March 2024 Chengdu Bright Eye Hospital had debt of CN¥532.3m, up from CN¥266.8m in one year. But on the other hand it also has CN¥748.4m in cash, leading to a CN¥216.2m net cash position.

A Look At Chengdu Bright Eye Hospital's Liabilities

The latest balance sheet data shows that Chengdu Bright Eye Hospital had liabilities of CN¥774.6m due within a year, and liabilities of CN¥1.66b falling due after that. Offsetting this, it had CN¥748.4m in cash and CN¥213.1m in receivables that were due within 12 months. So it has liabilities totalling CN¥1.47b more than its cash and near-term receivables, combined.

Chengdu Bright Eye Hospital has a market capitalization of CN¥5.43b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. While it does have liabilities worth noting, Chengdu Bright Eye Hospital also has more cash than debt, so we're pretty confident it can manage its debt safely.

Notably, Chengdu Bright Eye Hospital's EBIT launched higher than Elon Musk, gaining a whopping 117% on last year. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Chengdu Bright Eye Hospital can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Chengdu Bright Eye Hospital may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Chengdu Bright Eye Hospital recorded negative free cash flow, in total. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Summing Up

Although Chengdu Bright Eye Hospital's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of CN¥216.2m. And we liked the look of last year's 117% year-on-year EBIT growth. So we are not troubled with Chengdu Bright Eye Hospital's debt use. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 2 warning signs for Chengdu Bright Eye Hospital that you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301239

Chengdu Bright Eye Hospital Group

A specialized chain medical institution company, engages in the provision of ophthalmic general medical services in China.

Reasonable growth potential with mediocre balance sheet.