- Canada

- /

- Metals and Mining

- /

- TSX:AGI

Green Thumb Industries Leads Three Value Stocks On TSX For Your Consideration

Reviewed by Simply Wall St

Amidst a landscape of moderating inflation and shifting interest rate expectations in Canada, investors are closely watching market movements for opportunities. In such an environment, identifying undervalued stocks on the TSX can offer potential avenues for those looking to diversify their portfolios in alignment with current economic conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Canada

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Calian Group (TSX:CGY) | CA$56.01 | CA$110.60 | 49.4% |

| Calibre Mining (TSX:CXB) | CA$1.86 | CA$3.17 | 41.3% |

| goeasy (TSX:GSY) | CA$186.99 | CA$313.71 | 40.4% |

| Trisura Group (TSX:TSU) | CA$41.35 | CA$80.18 | 48.4% |

| Kinaxis (TSX:KXS) | CA$148.71 | CA$249.67 | 40.4% |

| Viemed Healthcare (TSX:VMD) | CA$10.45 | CA$20.08 | 48% |

| Endeavour Mining (TSX:EDV) | CA$29.64 | CA$54.00 | 45.1% |

| Green Thumb Industries (CNSX:GTII) | CA$16.00 | CA$27.13 | 41% |

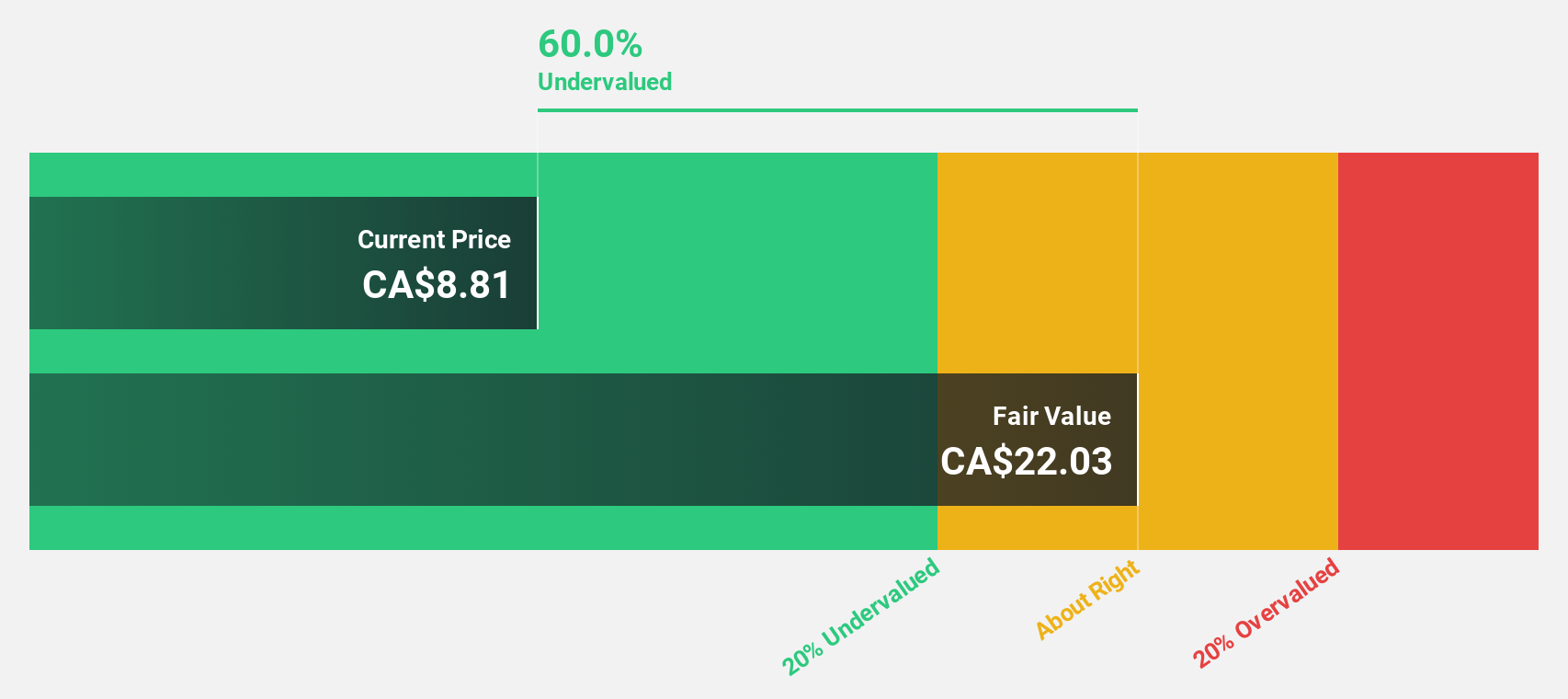

| Kits Eyecare (TSX:KITS) | CA$8.41 | CA$14.23 | 40.9% |

| Capstone Copper (TSX:CS) | CA$9.62 | CA$16.43 | 41.5% |

Let's dive into some prime choices out of from the screener

Green Thumb Industries (CNSX:GTII)

Overview: Green Thumb Industries Inc. operates in the United States, focusing on the manufacturing, distribution, marketing, and sale of cannabis products for both medical and adult use, with a market capitalization of approximately CA$3.79 billion.

Operations: The company generates revenue primarily through its Retail and Consumer Packaged Goods segments, with figures reported at $806.38 million and $583.78 million respectively.

Estimated Discount To Fair Value: 41%

Green Thumb Industries, trading at CA$16, significantly below the estimated fair value of CA$27.13, appears undervalued based on discounted cash flows. Recent expansion into new markets and potential strategic mergers indicate proactive management despite a forecasted modest return on equity of 7.5% in three years. With earnings expected to grow by 23% annually—outpacing the Canadian market's 14.6%—and revenue growth also above market trends at 10.3%, Green Thumb's financial health seems poised for improvement, aligning with its strategic initiatives and market expansions.

- Upon reviewing our latest growth report, Green Thumb Industries' projected financial performance appears quite optimistic.

- Click here to discover the nuances of Green Thumb Industries with our detailed financial health report.

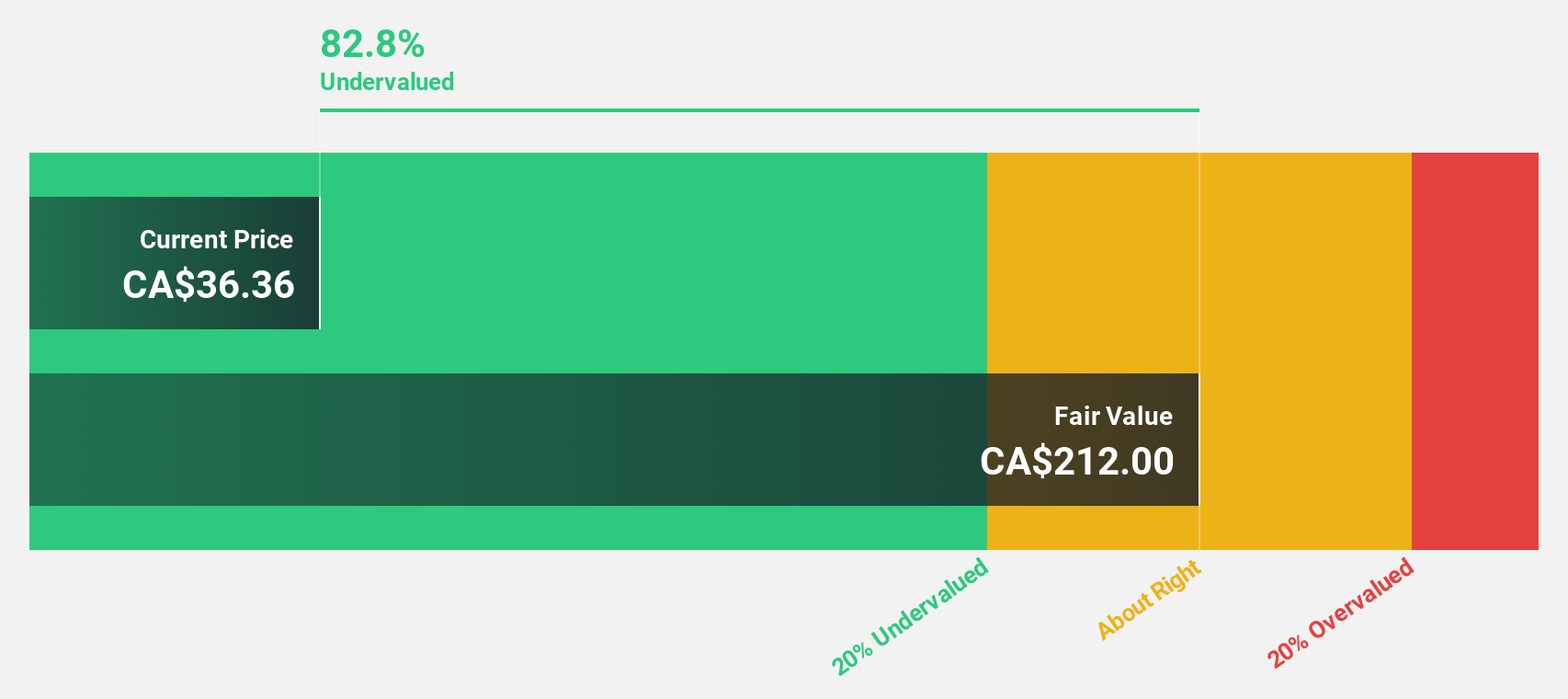

Alamos Gold (TSX:AGI)

Overview: Alamos Gold Inc. is a company involved in acquiring, exploring, developing, and extracting precious metals primarily in Canada and Mexico, with a market capitalization of approximately CA$8.51 billion.

Operations: The company generates revenue from three main segments: Mulatos (CA$442.80 million), Island Gold (CA$254.90 million), and Young-Davidson (CA$351.70 million).

Estimated Discount To Fair Value: 26.1%

Alamos Gold, priced at CA$21.75, trades 26.1% below its assessed fair value of CA$29.45, suggesting significant undervaluation based on cash flows. With a robust earnings growth forecast of 24.69% annually and revenue growth anticipated to exceed the Canadian market average at 16.4%, the company's financial prospects appear strong despite a relatively low expected return on equity of 15%. Recent exploration results indicate potential for further resource expansion, reinforcing its growth trajectory amidst ongoing dividend payments and shareholder returns.

- Our expertly prepared growth report on Alamos Gold implies its future financial outlook may be stronger than recent results.

- Dive into the specifics of Alamos Gold here with our thorough financial health report.

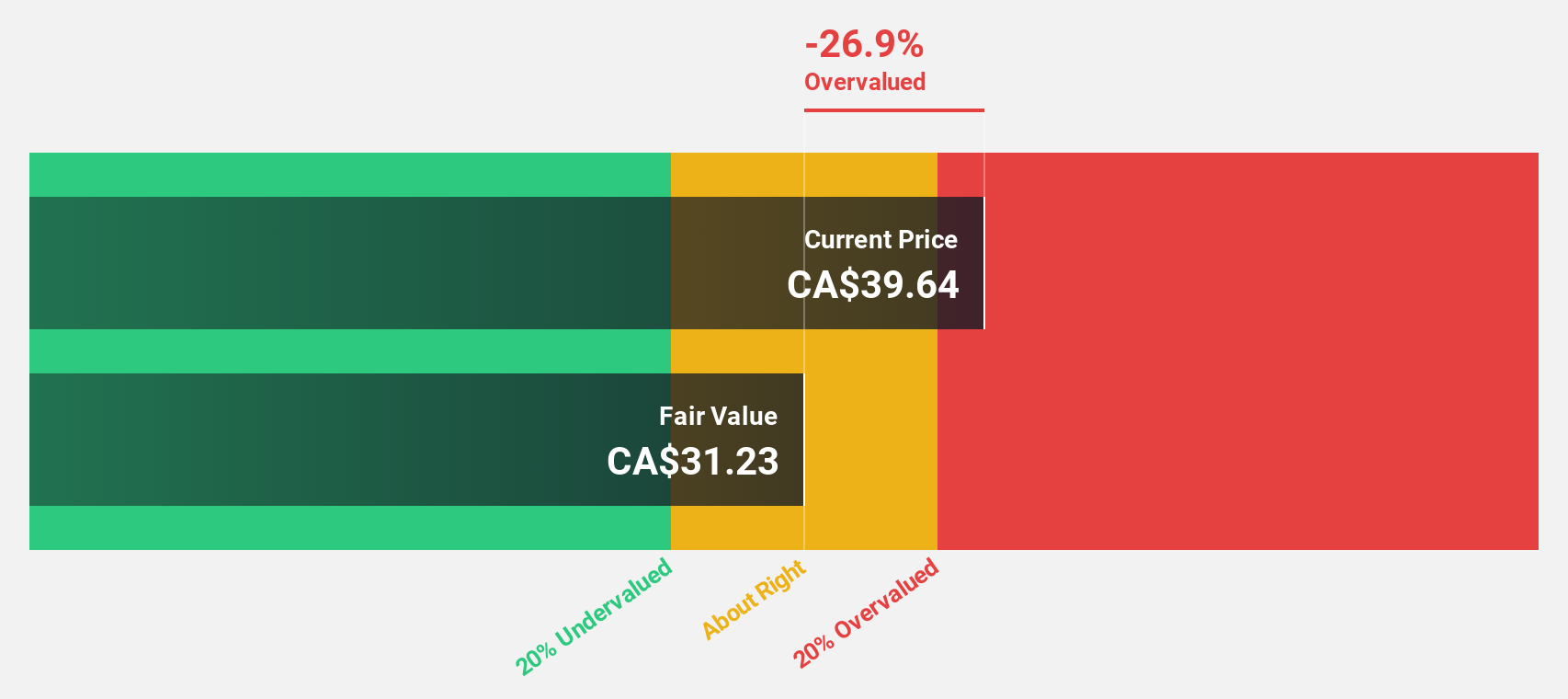

Docebo (TSX:DCBO)

Overview: Docebo Inc. is a learning management software company offering an AI-powered learning platform across North America and internationally, with a market capitalization of approximately CA$1.53 billion.

Operations: The company's revenue is primarily generated from its educational software segment, totaling CA$190.78 million.

Estimated Discount To Fair Value: 12.3%

Docebo, priced at CA$50.33, is considered undervalued against a fair value of CA$57.39, reflecting a modest discount based on cash flow analysis. The company's recent financial performance shows robust growth with Q1 sales rising from US$41.46 million to US$51.4 million year-over-year and net income increasing significantly to US$5.17 million. Forecasted annual earnings growth of 50.63% and revenue growth at 16.2% per year outpace the Canadian market averages, despite current profit margins being lower than the previous year at 3.5%.

- In light of our recent growth report, it seems possible that Docebo's financial performance will exceed current levels.

- Click to explore a detailed breakdown of our findings in Docebo's balance sheet health report.

Turning Ideas Into Actions

- Dive into all 25 of the Undervalued TSX Stocks Based On Cash Flows we have identified here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:AGI

Alamos Gold

Operates as a gold producer in Canada, Mexico, and the United States.

Exceptional growth potential with solid track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)