Advertisement

Dollarama (TSX:DOL) Q2 Earnings Soar with EPS of $1.02; Strategic Expansion in Latin America Boosts Growth

Dollarama(TSX:DOL) is navigating a dynamic period marked by both strengths and challenges. Recent highlights include a robust EPS of $1.02 for Q2 fiscal 2025 and a 4.7% growth in same-store sales, contrasted with concerns over high valuation and increased operating costs. In the discussion that follows, we will delve into Dollarama's financial health, operational inefficiencies, strategic growth initiatives, and external threats to provide a comprehensive overview of the company's current business situation.

Navigate through the intricacies of Dollarama with our comprehensive report here.

Strengths: Core Advantages Driving Sustained Success For Dollarama

Dollarama has demonstrated robust financial performance, as evidenced by its strong second quarter fiscal 2025 results, translating into an EPS of $1.02, as noted by CEO Neil Rossy. The company has also seen a 4.7% growth in same-store sales, driven primarily by the demand for consumable products, which are everyday essentials. CFO Patrick Bui highlighted an improved gross margin of 45.2% compared to 43.9% in the same quarter last year, reflecting effective cost management. Additionally, the company's successful expansion in Latin America, with Dollarcity opening 23 new stores during the quarter, underscores its strategic growth initiatives. Dollarama's management team, with an average tenure of 3.7 years, brings valuable experience to its strategic goals, further solidifying its market position.

Weaknesses: Critical Issues Affecting Dollarama's Performance and Areas For Growth

Dollarama has faced challenges with weak seasonal product sales, a trend that has persisted across several quarters, as noted by Neil Rossy. The same-store sales growth was primarily driven by a 7% increase in transactions but was partially offset by a 2.2% decrease in basket size, reflecting pressures on consumer spending. Operating costs have risen, and Patrick Bui has highlighted ongoing efforts to counteract these expenses through efficiency and productivity improvements.

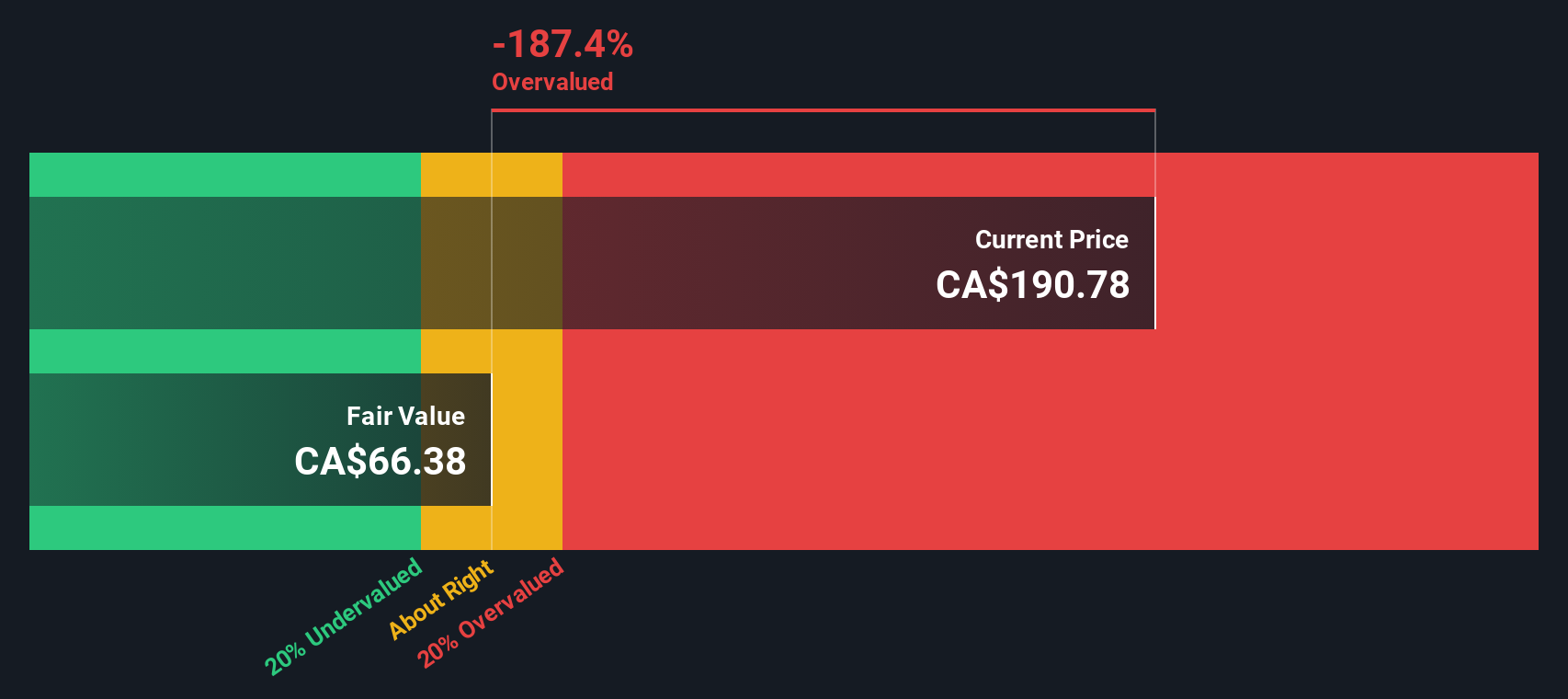

Amid these challenges, the company's current share price is approximately 20% above the analyst's target price. The Price-To-Earnings Ratio of 34.9x suggests that Dollarama is trading at a premium compared to the industry average of 19.6x and the peer average of 21.3x, indicating a higher valuation. To dive deeper into how Dollarama's valuation metrics are shaping its market position, check out our detailed analysis of Dollarama's Valuation.

Opportunities: Potential Strategies for Leveraging Growth and Competitive Advantage

DOL has several strategic opportunities that could enhance its market position. The company's planned expansion into Mexico by 2026, as mentioned by Neil Rossy, represents a significant growth avenue. Leveraging existing infrastructure in Latin America, as highlighted by Patrick Bui, could streamline operations and reduce costs. Additionally, there is potential for increased capital return from Dollarcity, which is being assessed for future shareholder returns. These initiatives could help Dollarama capitalize on emerging market opportunities and strengthen its competitive advantage.

Learn more about how these opportunities could impact Dollarama's future growth by reviewing our analysis of Dollarama's Future Performance.

Threats: Key Risks and Challenges That Could Impact Dollarama's Success

Several external factors pose risks to Dollarama's growth. Cautious consumer spending in the current economic environment, as noted by Neil Rossy, could impact sales. The competitive landscape in the Canadian retail market is another challenge, with Rossy acknowledging that all retailers are each other's competition on any given item or category. Additionally, adverse weather conditions negatively impacted summer sales, a factor that could continue to affect performance. Significant insider selling over the past three months and the company's high level of debt further exacerbate these risks. These threats highlight the need for Dollarama to navigate external pressures carefully to maintain its market share and growth trajectory.

Conclusion

Dollarama's strong financial performance, highlighted by its improved gross margin and EPS growth, underscores its effective cost management and strategic expansion efforts, particularly in Latin America. However, the company's high Price-To-Earnings Ratio of 34.9x, significantly above industry and peer averages, suggests that its current share price may be overextended, posing a risk to future investor returns. Additionally, challenges such as soft seasonal product sales and increased operating costs indicate underlying pressures on consumer spending. While the planned expansion into Mexico and potential capital returns from Dollarcity present growth opportunities, Dollarama must navigate these risks carefully to sustain its market position and drive future growth.

Have a stake in these TSX:DOL? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About TSX:DOL

Dollarama

Operates a chain of stores and provides related logistical and administrative support activities.

Reasonable growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.3% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$6.60|7.0% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|65.0% undervalued

ME

Community Contributor