- Canada

- /

- Oil and Gas

- /

- TSX:TVE

Undervalued Small Caps In Global With Insider Buying

Reviewed by Simply Wall St

In recent weeks, global markets have experienced significant volatility driven by escalating trade tensions and fluctuating consumer sentiment. While major indices like the S&P 500 and Nasdaq Composite showed gains, small-cap stocks, as represented by the Russell 2000 Index, posted more modest increases amid ongoing economic uncertainty. In such a dynamic environment, identifying promising investment opportunities often involves looking for companies with strong fundamentals that can navigate these challenges effectively.

Top 10 Undervalued Small Caps With Insider Buying Globally

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Morgan Advanced Materials | 10.4x | 0.5x | 43.75% | ★★★★★★ |

| Tristel | 25.5x | 3.6x | 32.69% | ★★★★★☆ |

| Speedy Hire | NA | 0.2x | 26.95% | ★★★★★☆ |

| Chorus Aviation | NA | 0.4x | 19.07% | ★★★★★☆ |

| Sing Investments & Finance | 7.4x | 3.7x | 41.49% | ★★★★☆☆ |

| Saturn Oil & Gas | 5.1x | 0.3x | 0.52% | ★★★★☆☆ |

| Norcros | 22.9x | 0.5x | 31.44% | ★★★☆☆☆ |

| FRP Advisory Group | 12.4x | 2.2x | 10.11% | ★★★☆☆☆ |

| Arendals Fossekompani | 20.9x | 1.6x | 48.06% | ★★★☆☆☆ |

| Westshore Terminals Investment | 13.3x | 3.8x | 38.92% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

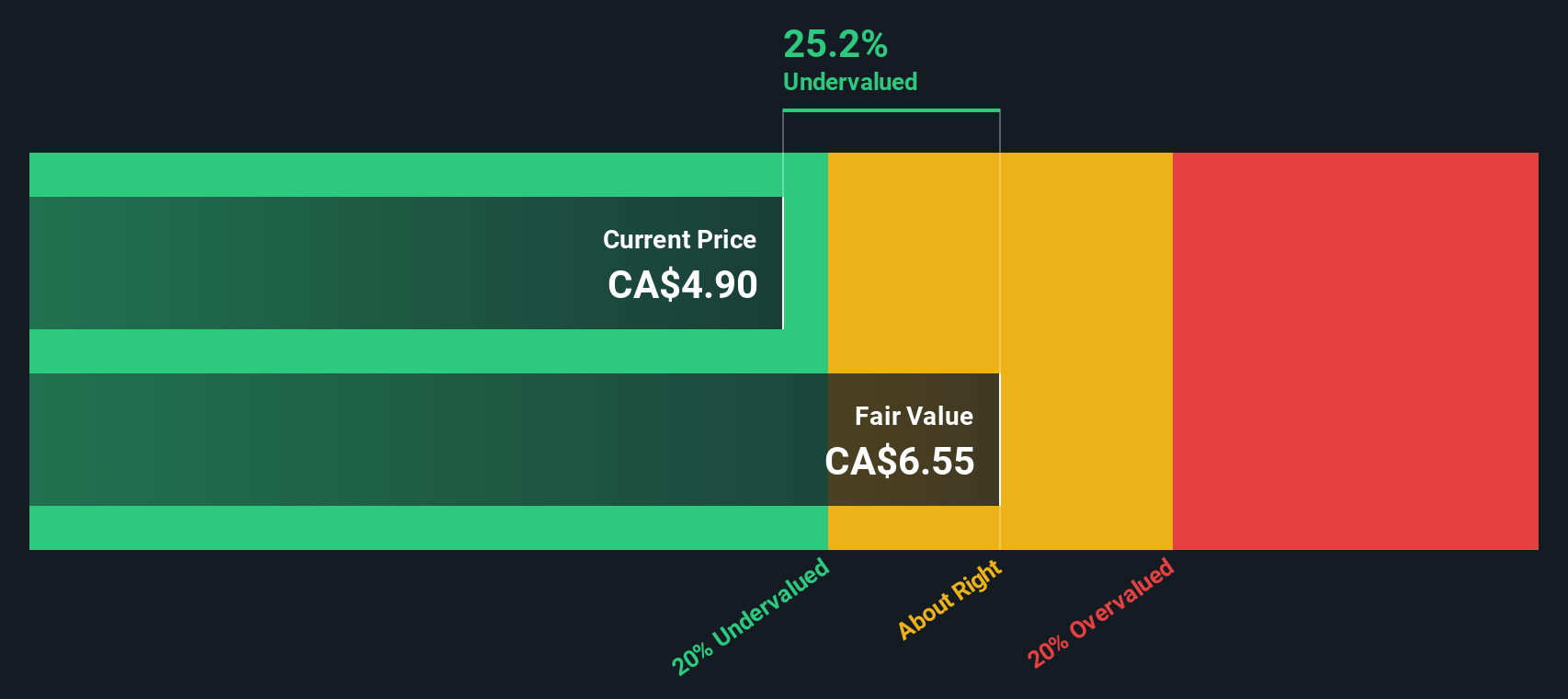

Navigator Global Investments (ASX:NGI)

Simply Wall St Value Rating: ★★★★★★

Overview: Navigator Global Investments is an asset management company primarily operating through its Lighthouse segment, with a market capitalization of A$0.37 billion.

Operations: Lighthouse contributes significantly to revenue generation. The gross profit margin has shown a downward trend, decreasing from 93.93% to 36.25% over the observed period, indicating a rise in cost of goods sold relative to revenue. Operating expenses are primarily driven by general and administrative costs, with notable fluctuations in non-operating expenses impacting net income margins significantly across different periods.

PE: 4.3x

Navigator Global Investments, a smaller company in the investment space, has shown significant earnings growth with revenue reaching US$148.06 million for the half-year ending December 2024, up from US$105.9 million the previous year. Net income surged to US$68.79 million from US$9.98 million year-over-year, reflecting strong operational performance despite reliance on external borrowing for funding. Insider confidence is evident with recent share purchases by insiders during early 2025, suggesting potential value recognition within the company’s stock amidst forecasted revenue growth of 10.43% annually over three years despite expected earnings decline by an average of 18.5% per year in the same period.

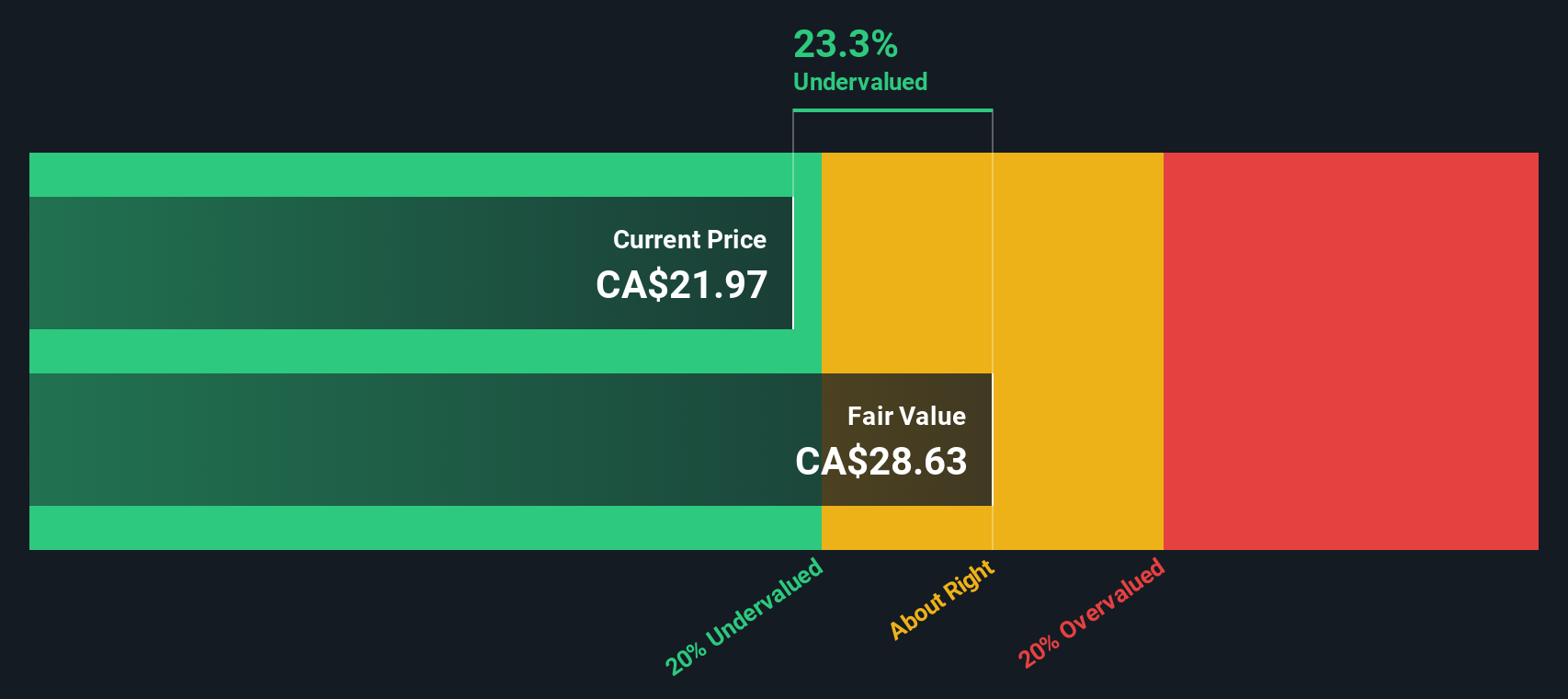

Allied Properties Real Estate Investment Trust (TSX:AP.UN)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Allied Properties Real Estate Investment Trust is a Canadian real estate investment trust focused on owning, managing, and developing urban office environments primarily in major cities such as Toronto, Montréal, and Vancouver with a market capitalization of CA$2.98 billion.

Operations: The company's revenue is primarily derived from its operations in Toronto & Kitchener and Montréal & Ottawa, contributing CA$285.19 million and CA$214.63 million, respectively. The gross profit margin has shown fluctuations, with recent figures around 49.21% to 54.46%. Operating expenses have varied slightly over time, with the most recent quarter reporting CA$26.01 million in operating expenses and a non-operating expense of CA$608.97 million impacting net income significantly.

PE: -6.1x

Allied Properties Real Estate Investment Trust, a smaller player in the market, has recently shown insider confidence with increased share purchases. The company declared a monthly distribution of C$0.15 per unit for April 2025, maintaining its annualized payout of C$1.80 per unit. Allied completed a private placement offering of C$400 million in senior unsecured debentures to refinance existing debt, rated “BBB” with a negative trend by Morningstar DBRS. Despite challenges like high-risk funding sources and uncovered debt by operating cash flow, earnings are projected to grow significantly at 107% annually, indicating potential future value for investors seeking opportunities within this sector.

- Take a closer look at Allied Properties Real Estate Investment Trust's potential here in our valuation report.

Learn about Allied Properties Real Estate Investment Trust's historical performance.

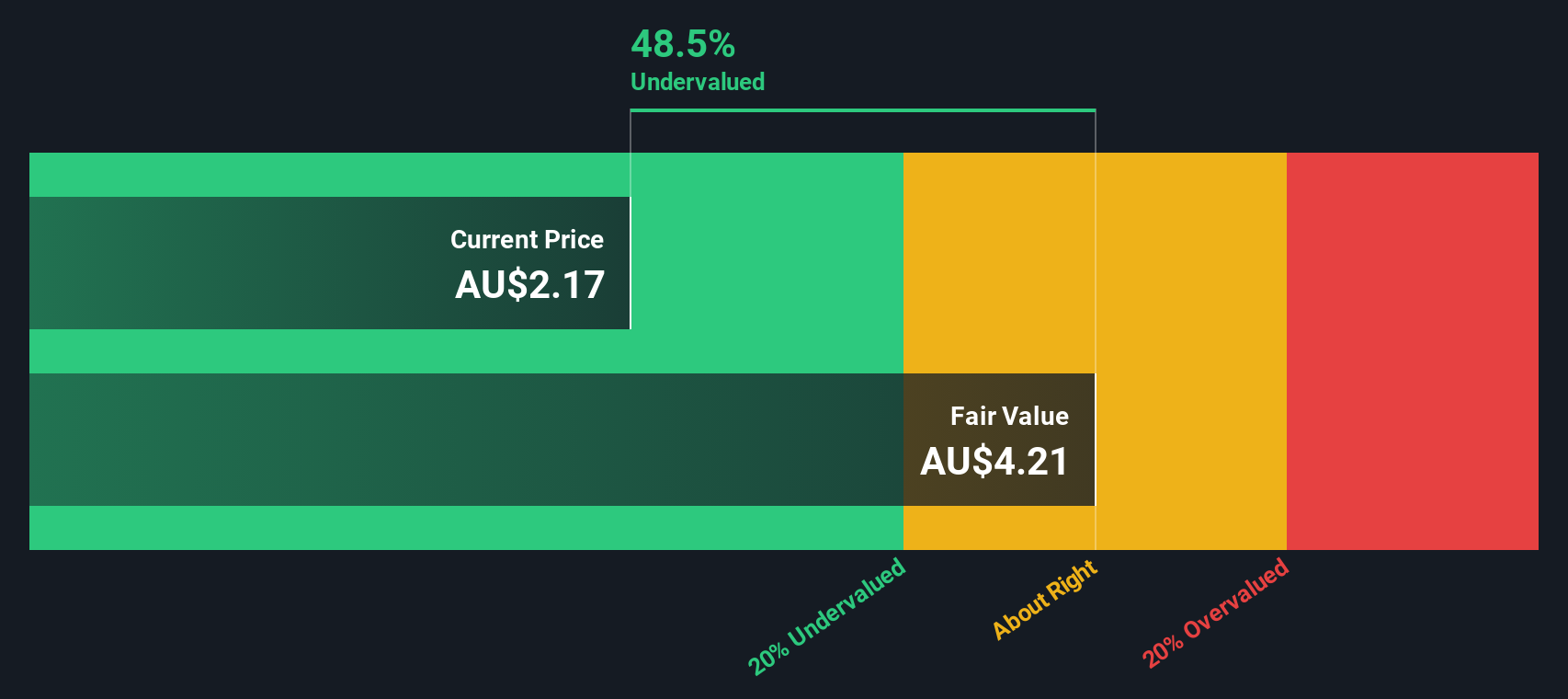

Tamarack Valley Energy (TSX:TVE)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Tamarack Valley Energy is a Canadian oil and gas company focused on exploration and production, with a market cap of CA$2.14 billion.

Operations: The company generates revenue primarily from its oil and gas exploration and production activities, with a recent quarterly revenue of CA$1.40 billion. The gross profit margin has shown variability, reaching 78.25% in the latest period. Cost of goods sold (COGS) was reported at CA$305.44 million, impacting overall profitability alongside operating expenses such as depreciation and general administrative costs.

PE: 11.5x

Tamarack Valley Energy, a smaller company in the energy sector, has seen insider confidence with share purchases over recent months. Despite a decrease in revenue to C$1.34 billion from C$1.42 billion last year, net income rose significantly to C$162 million from C$94 million. The company also repurchased 11.9 million shares for C$31.1 million between October and December 2024, indicating strategic capital management amid fluctuating production levels and consistent dividend payouts of CAD 0.01275 per share monthly.

Summing It All Up

- Click this link to deep-dive into the 150 companies within our Undervalued Global Small Caps With Insider Buying screener.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tamarack Valley Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:TVE

Tamarack Valley Energy

Engages in the exploration, development, production, and sale of oil, natural gas, and natural gas liquids in the Western Canadian sedimentary basin.

Good value with proven track record.

Market Insights

Community Narratives