Advertisement

January 2025's Noteworthy Stocks Trading Below Estimated Value

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate the early days of President Trump's administration, investors are buoyed by hopes for softer tariffs and enthusiasm surrounding artificial intelligence, propelling U.S. stocks to record highs. Amid this optimistic climate, identifying undervalued stocks becomes crucial as they offer potential opportunities for growth when trading below their estimated value.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Alltop Technology (TPEX:3526) | NT$264.50 | NT$526.73 | 49.8% |

| Guangdong Mingyang ElectricLtd (SZSE:301291) | CN¥50.90 | CN¥101.57 | 49.9% |

| World Fitness Services (TWSE:2762) | NT$92.70 | NT$184.63 | 49.8% |

| 74Software (ENXTPA:74SW) | €26.50 | €52.89 | 49.9% |

| Solum (KOSE:A248070) | ₩18950.00 | ₩37756.10 | 49.8% |

| Dynavox Group (OM:DYVOX) | SEK68.20 | SEK136.07 | 49.9% |

| GemPharmatech (SHSE:688046) | CN¥13.06 | CN¥26.02 | 49.8% |

| Shandong Weigao Orthopaedic Device (SHSE:688161) | CN¥25.57 | CN¥51.06 | 49.9% |

| St. James's Place (LSE:STJ) | £9.31 | £18.53 | 49.8% |

| Netum Group Oyj (HLSE:NETUM) | €2.82 | €5.63 | 49.9% |

Let's explore several standout options from the results in the screener.

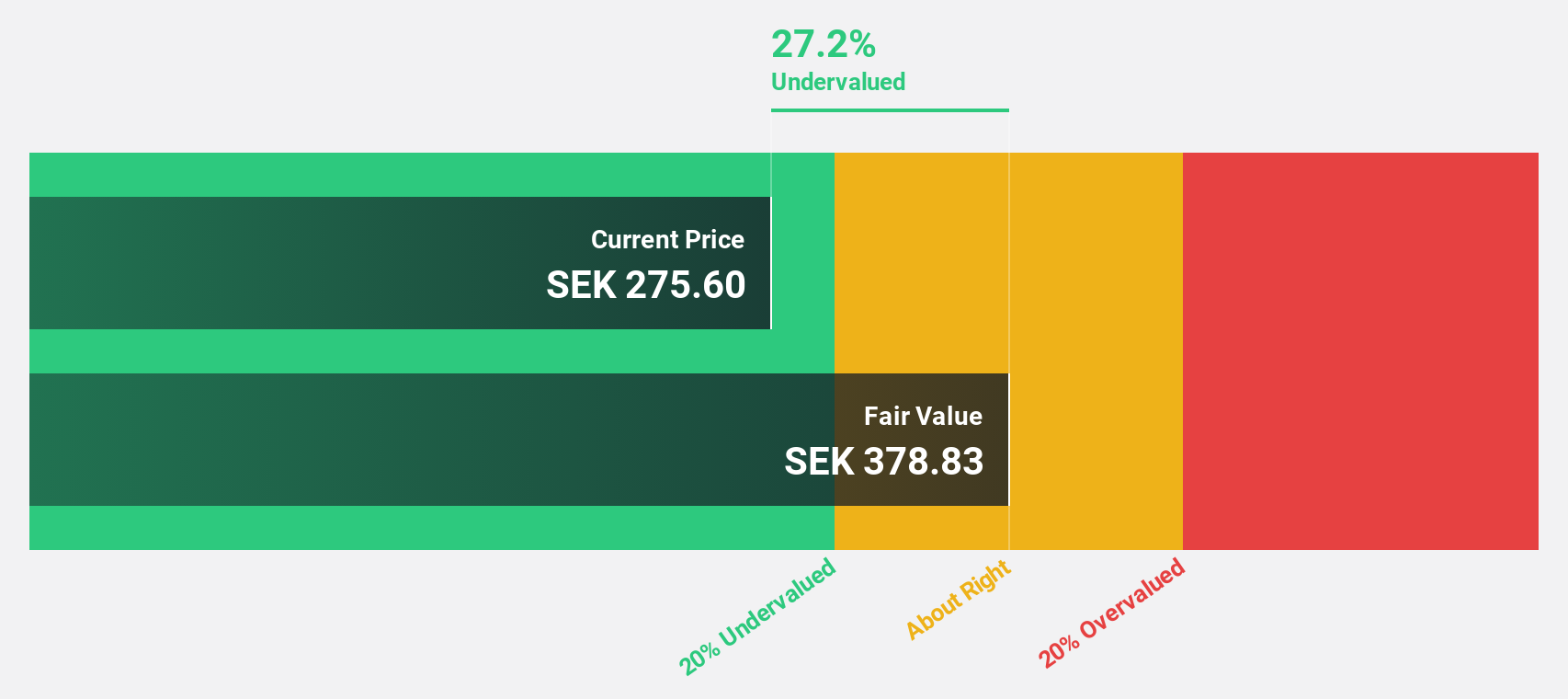

Thule Group (OM:THULE)

Overview: Thule Group AB (publ) is a sports and leisure company operating in Sweden and internationally, with a market cap of SEK38.26 billion.

Operations: The company's revenue is primarily derived from its Outdoor & Bags segment, which generated SEK9.43 billion.

Estimated Discount To Fair Value: 12.3%

Thule Group's stock is trading at SEK353.2, below its fair value estimate of SEK402.55, indicating potential undervaluation. The company's revenue growth forecast of 14% annually surpasses the Swedish market average and its earnings are expected to grow significantly at 23.4% per year over the next three years. Despite an unstable dividend track record, Thule's high projected return on equity of 21.9% in three years enhances its investment appeal amidst ongoing strategic activities like considering Quad Lock acquisition.

- Our expertly prepared growth report on Thule Group implies its future financial outlook may be stronger than recent results.

- Click here to discover the nuances of Thule Group with our detailed financial health report.

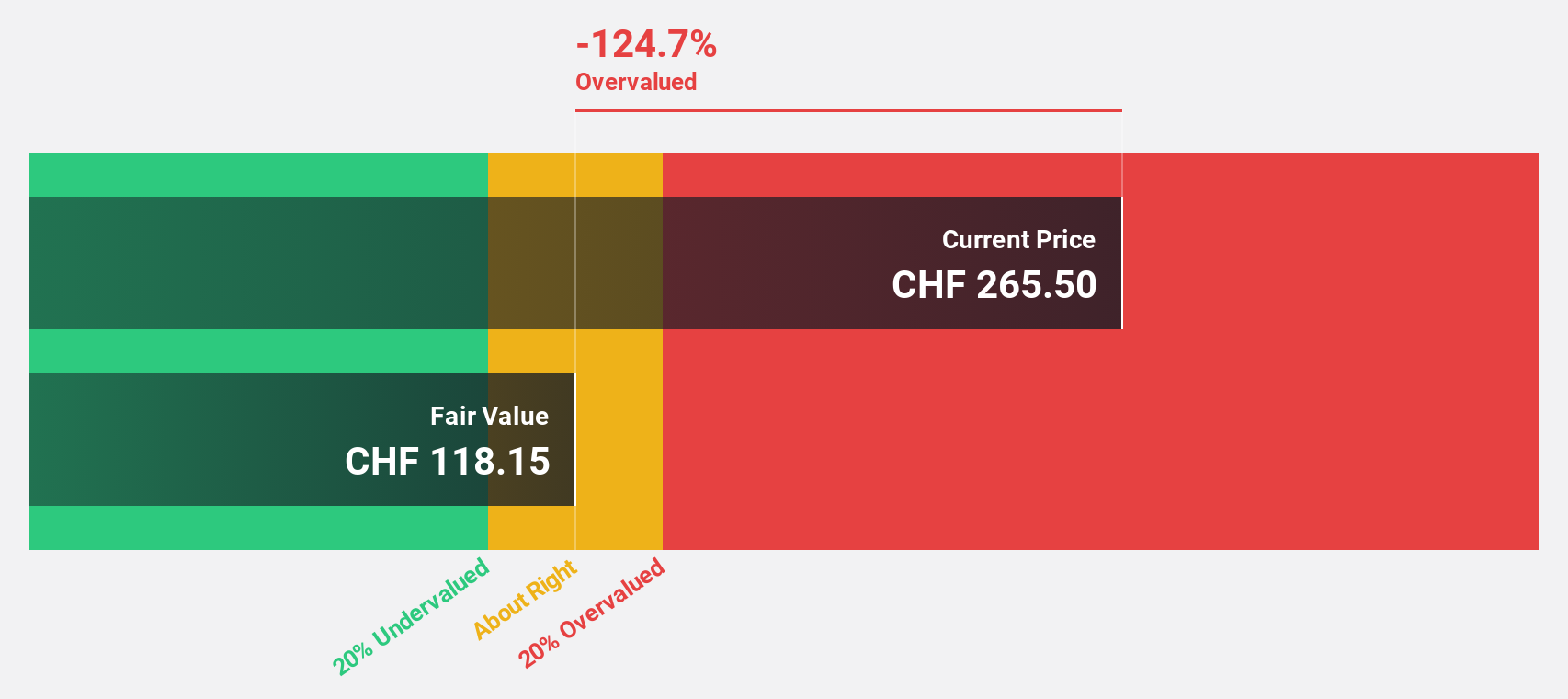

ALSO Holding (SWX:ALSN)

Overview: ALSO Holding AG is a technology services provider for the ICT industry operating in Switzerland, Germany, the Netherlands, Poland, and internationally with a market cap of CHF3.06 billion.

Operations: The company's revenue is derived from its operations in Central Europe, generating €4.62 billion, and Northern/Eastern Europe, contributing €5.24 billion.

Estimated Discount To Fair Value: 49.1%

ALSO Holding's stock, trading at CHF244.5, is significantly undervalued compared to its fair value estimate of CHF480.36. Despite a modest revenue growth forecast of 9.8% annually, which outpaces the Swiss market average, the company's earnings are expected to grow substantially at 26.4% per year over the next three years. However, a lower projected return on equity of 15.3% in three years may temper some investor enthusiasm despite its attractive valuation based on cash flows.

- In light of our recent growth report, it seems possible that ALSO Holding's financial performance will exceed current levels.

- Delve into the full analysis health report here for a deeper understanding of ALSO Holding.

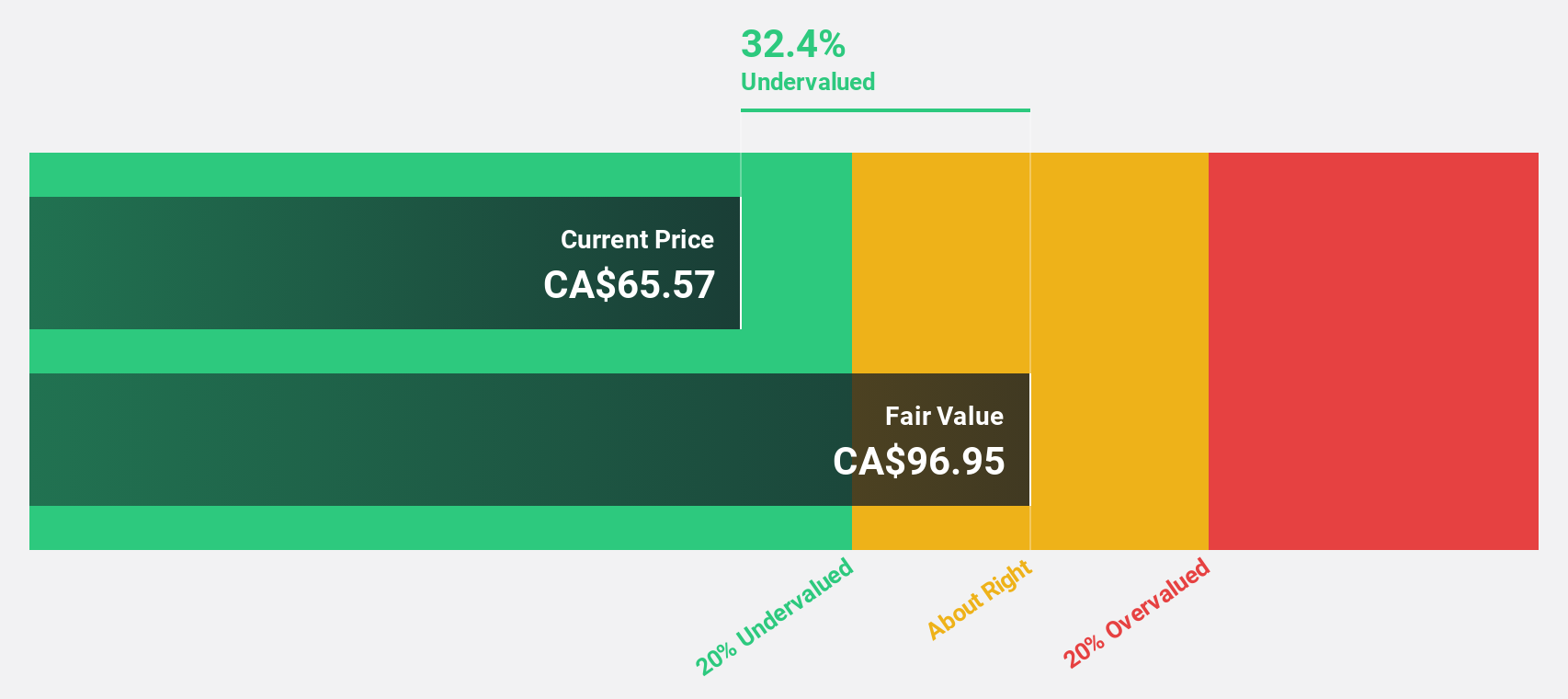

GFL Environmental (TSX:GFL)

Overview: GFL Environmental Inc. provides non-hazardous solid waste management and environmental services across Canada and the United States, with a market cap of CA$23.83 billion.

Operations: The company's revenue segments consist of CA$4.86 billion from U.S. solid waste, CA$2.21 billion from Canadian solid waste, and CA$1.69 billion from environmental services.

Estimated Discount To Fair Value: 19.2%

GFL Environmental, trading at CA$61.95, appears undervalued against its fair value estimate of CA$76.68. The company is in talks to sell its environmental services division for approximately $8 billion, potentially enhancing cash flow and reducing debt by at least CAD 3.5 billion post-tax. Despite a slower revenue growth forecast of 6.5% annually compared to market averages, earnings are projected to grow significantly at over 100% per year, indicating strong future profitability prospects.

- Upon reviewing our latest growth report, GFL Environmental's projected financial performance appears quite optimistic.

- Get an in-depth perspective on GFL Environmental's balance sheet by reading our health report here.

Summing It All Up

- Take a closer look at our Undervalued Stocks Based On Cash Flows list of 888 companies by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Thule Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:THULE

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.1% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.9% undervalued

TI

Community Contributor