- Belgium

- /

- Communications

- /

- ENXTBR:EVS

At €15.10, Is It Time To Put EVS Broadcast Equipment SA (EBR:EVS) On Your Watch List?

EVS Broadcast Equipment SA (EBR:EVS), is not the largest company out there, but it led the ENXTBR gainers with a relatively large price hike in the past couple of weeks. Less-covered, small caps tend to present more of an opportunity for mispricing due to the lack of information available to the public, which can be a good thing. So, could the stock still be trading at a low price relative to its actual value? Let’s examine EVS Broadcast Equipment’s valuation and outlook in more detail to determine if there’s still a bargain opportunity.

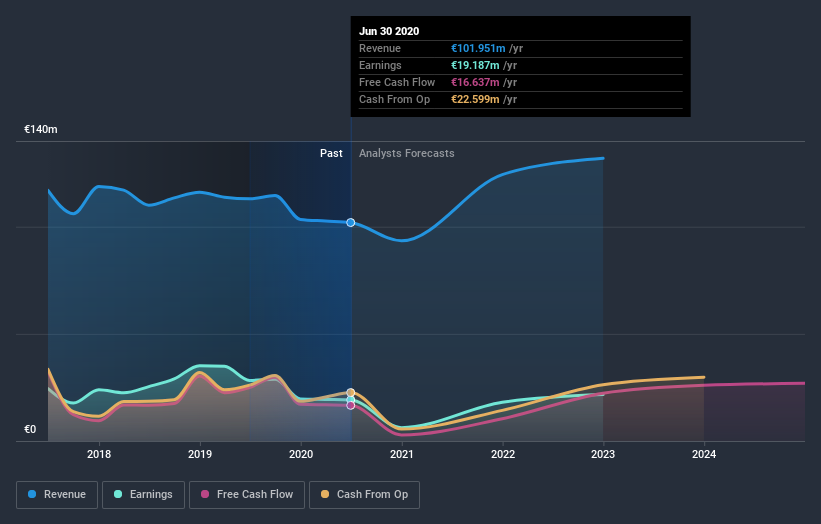

View our latest analysis for EVS Broadcast Equipment

What is EVS Broadcast Equipment worth?

Great news for investors – EVS Broadcast Equipment is still trading at a fairly cheap price according to my price multiple model, where I compare the company's price-to-earnings ratio to the industry average. In this instance, I’ve used the price-to-earnings (PE) ratio given that there is not enough information to reliably forecast the stock’s cash flows. I find that EVS Broadcast Equipment’s ratio of 10.93x is below its peer average of 27.73x, which indicates the stock is trading at a lower price compared to the Communications industry. Another thing to keep in mind is that EVS Broadcast Equipment’s share price is quite stable relative to the rest of the market, as indicated by its low beta. This means that if you believe the current share price should move towards its industry peers, a low beta could suggest it is not likely to reach that level anytime soon, and once it’s there, it may be hard to fall back down into an attractive buying range again.

What does the future of EVS Broadcast Equipment look like?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. However, with a relatively muted profit growth of 3.4% expected over the next couple of years, growth doesn’t seem like a key driver for a buy decision for EVS Broadcast Equipment, at least in the short term.

What this means for you:

Are you a shareholder? Even though growth is relatively muted, since EVS is currently trading below the industry PE ratio, it may be a great time to accumulate more of your holdings in the stock. However, there are also other factors such as capital structure to consider, which could explain the current price multiple.

Are you a potential investor? If you’ve been keeping an eye on EVS for a while, now might be the time to make a leap. Its future profit outlook isn’t fully reflected in the current share price yet, which means it’s not too late to buy EVS. But before you make any investment decisions, consider other factors such as the strength of its balance sheet, in order to make a well-informed investment decision.

Since timing is quite important when it comes to individual stock picking, it's worth taking a look at what those latest analysts forecasts are. Luckily, you can check out what analysts are forecasting by clicking here.

If you are no longer interested in EVS Broadcast Equipment, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

When trading EVS Broadcast Equipment or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if EVS Broadcast Equipment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ENXTBR:EVS

EVS Broadcast Equipment

Provides live video technology for broadcast and media productions in the United States, Europe, Africa, Middle East, and Asia Pacific.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)