3 Undervalued Small Caps On ASX With Insider Action In Australia

Reviewed by Simply Wall St

The Australian market has recently seen a mix of gains and losses, with the ASX200 closing up 0.34% despite some sectors like Utilities and Materials underperforming. In this environment, identifying small-cap stocks that show potential through insider actions can be crucial for investors seeking opportunities amidst fluctuating market conditions.

Top 10 Undervalued Small Caps With Insider Buying In Australia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Infomedia | 41.5x | 3.7x | 36.40% | ★★★★★★ |

| Collins Foods | 15.3x | 0.6x | 14.27% | ★★★★★☆ |

| SHAPE Australia | 14.8x | 0.3x | 28.54% | ★★★★☆☆ |

| Dicker Data | 18.9x | 0.7x | -57.60% | ★★★★☆☆ |

| Eureka Group Holdings | 18.6x | 6.0x | 30.79% | ★★★★☆☆ |

| Abacus Group | NA | 5.3x | 28.10% | ★★★★☆☆ |

| Healius | NA | 0.6x | 8.63% | ★★★★☆☆ |

| Tabcorp Holdings | NA | 0.6x | 3.14% | ★★★★☆☆ |

| Corporate Travel Management | 22.0x | 2.6x | 46.17% | ★★★☆☆☆ |

| Abacus Storage King | 11.0x | 6.9x | -20.25% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

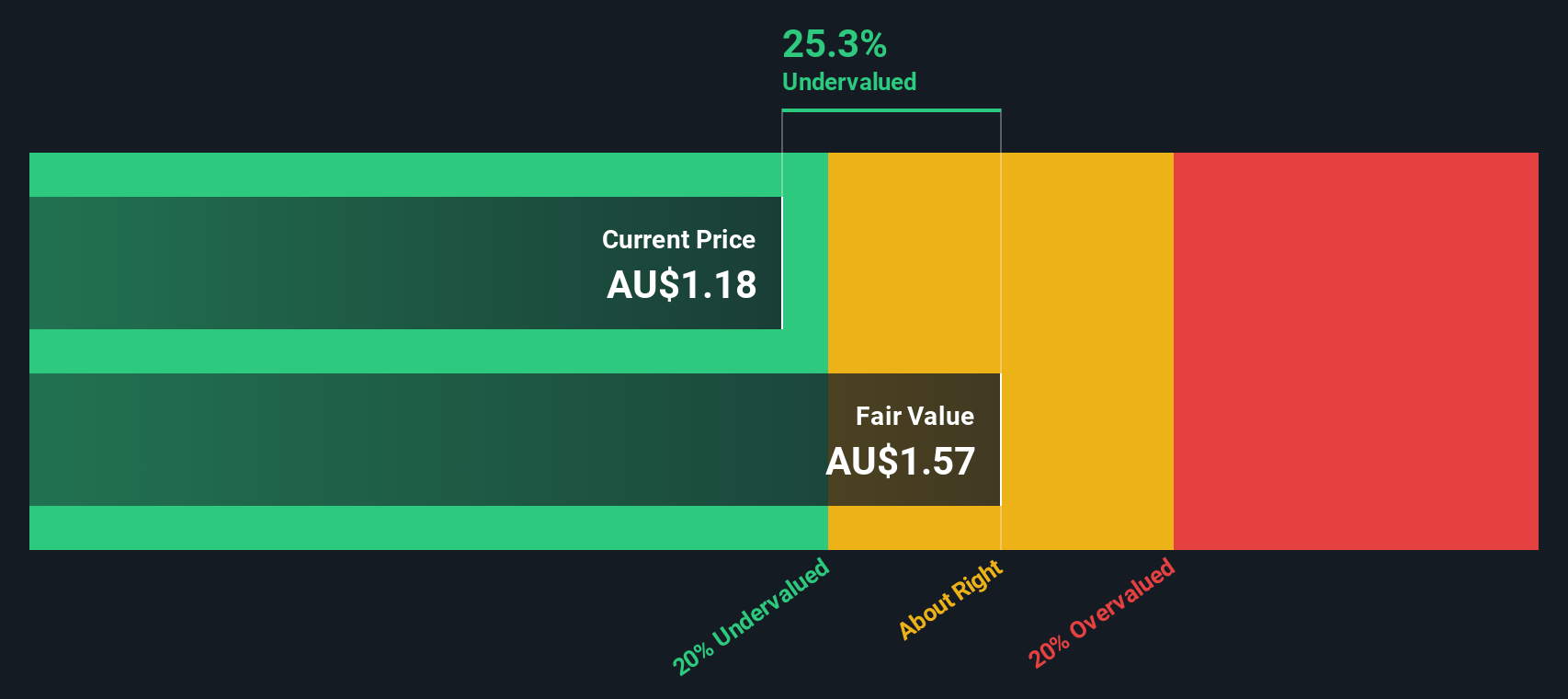

Abacus Group (ASX:ABG)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Abacus Group is a diversified property investment company focusing on commercial real estate, with a market capitalization of A$2.34 billion.

Operations: Abacus Group's recent financial data shows a revenue of A$192.35 million, with a gross profit of A$148.76 million and operating expenses at A$38.76 million for the period ending June 30, 2024. The company experienced a net income margin of -125.81% during this time frame, indicating significant non-operating expenses impacting its profitability.

PE: -4.2x

Abacus Group, a smaller player in the Australian market, is drawing attention with its forecasted earnings growth of 53.58% annually. Despite relying solely on external borrowing for funding, which carries higher risk, insider confidence is evident with share purchases throughout 2024. The company recently affirmed a dividend of A$0.0425 per share for the second half of 2024, indicating steady shareholder returns. Looking ahead, Abacus's financial strategy and leadership changes could shape its growth trajectory amidst these dynamics.

- Take a closer look at Abacus Group's potential here in our valuation report.

Assess Abacus Group's past performance with our detailed historical performance reports.

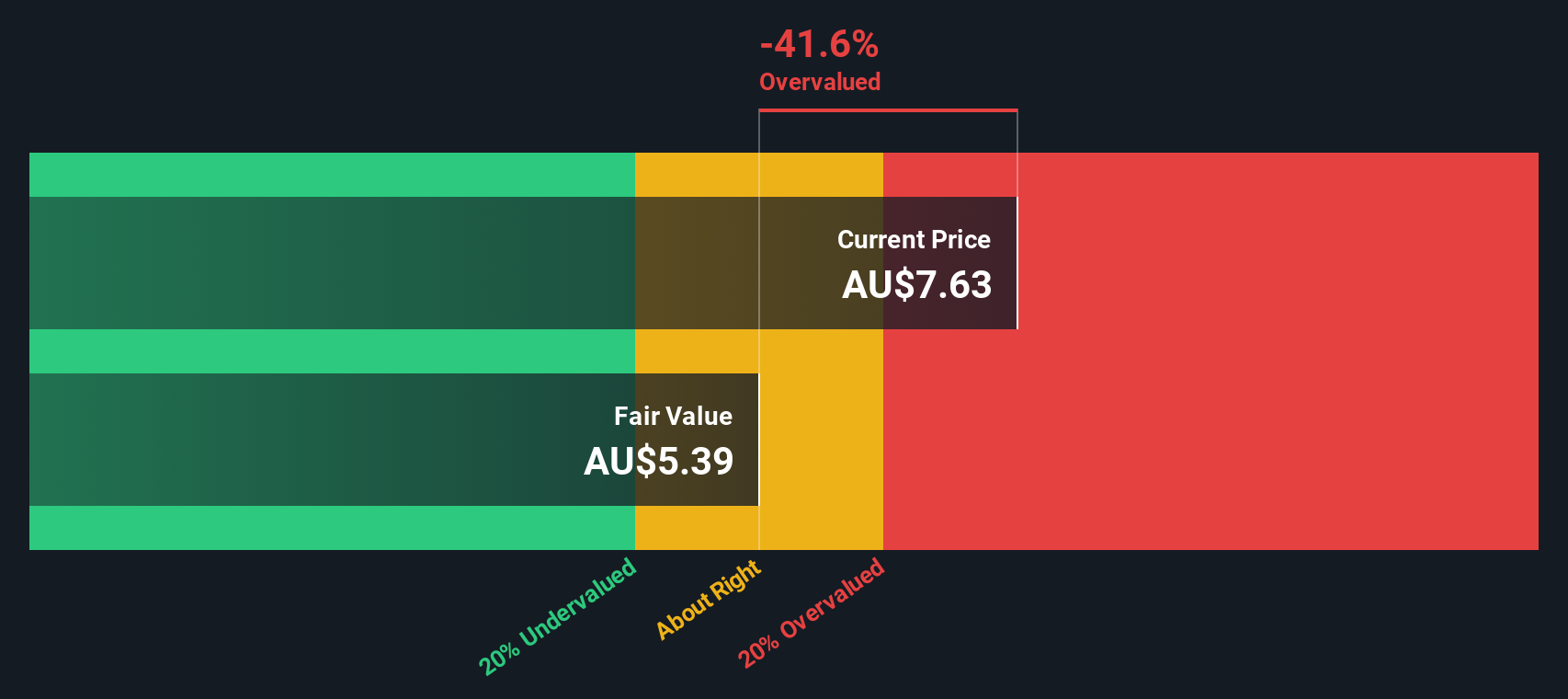

Centuria Capital Group (ASX:CNI)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Centuria Capital Group is a diversified investment manager specializing in property funds management, co-investments, and development finance, with a market capitalization of A$1.76 billion.

Operations: Centuria Capital Group's revenue is primarily derived from Property Funds Management, Co-Investments, and Development segments. The company has experienced fluctuations in its gross profit margin, with a notable high of 89.33% in June 2020 and a low of 41.37% in June 2017. Operating expenses have varied significantly over time, impacting overall profitability.

PE: 20.4x

Centuria Capital Group, a player in the Australian investment sector, shows potential as an undervalued stock. With a forecasted earnings growth of 13% annually and recent insider confidence demonstrated by Kristie Brown's A$453,035 share purchase in late 2024, it suggests internal optimism about future prospects. The company recently increased its interim distribution to 5.20 cents per security for December 2024. Despite reliance on higher-risk external borrowing for funding, the appointment of Ms. Brown as Chairman brings extensive expertise to steer strategic directions forward.

Data#3 (ASX:DTL)

Simply Wall St Value Rating: ★★★★★★

Overview: Data#3 is a value-added IT reseller and IT solutions provider with a market cap of A$1.08 billion.

Operations: The company's revenue is primarily generated from its operations as a value-added IT reseller and IT solutions provider, with recent quarterly revenues reaching A$805.75 million. Over the analyzed periods, the gross profit margin has shown an upward trend, peaking at 9.87%. Operating expenses have varied slightly but remain a significant component of costs alongside depreciation and non-operating expenses.

PE: 22.5x

Data#3, a smaller company in Australia, has caught attention with its potential for value. The recent appointment of Bronwyn Morris to the board brings seasoned expertise in finance and governance, enhancing strategic direction. Despite relying on external borrowing for funding, which carries higher risk, earnings are projected to grow by 9.61% annually. Insider confidence is evident from recent share purchases over the past year, indicating belief in future prospects amidst evolving leadership dynamics.

- Delve into the full analysis valuation report here for a deeper understanding of Data#3.

Explore historical data to track Data#3's performance over time in our Past section.

Seize The Opportunity

- Click here to access our complete index of 22 Undervalued ASX Small Caps With Insider Buying.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:CNI

Centuria Capital Group

An investment manager, markets and manages investment products primarily in Australia.

Solid track record average dividend payer.

Similar Companies

Market Insights

Community Narratives