ASX Stocks Estimated To Be Trading Below Intrinsic Value In January 2025

Reviewed by Simply Wall St

As the Australian market continues to adjust to the new Trump administration, the ASX200 has climbed higher for the third consecutive week, closing up 0.36% at 8,408 points. Amidst this upward momentum and sector-specific performances, identifying stocks that are trading below their intrinsic value can offer potential opportunities for investors looking to capitalize on undervalued assets in a fluctuating market environment.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Data#3 (ASX:DTL) | A$6.85 | A$12.30 | 44.3% |

| SKS Technologies Group (ASX:SKS) | A$2.15 | A$3.80 | 43.4% |

| Mader Group (ASX:MAD) | A$6.09 | A$11.91 | 48.9% |

| Atlas Arteria (ASX:ALX) | A$4.99 | A$9.71 | 48.6% |

| MLG Oz (ASX:MLG) | A$0.605 | A$1.16 | 47.9% |

| Charter Hall Group (ASX:CHC) | A$15.31 | A$29.16 | 47.5% |

| ReadyTech Holdings (ASX:RDY) | A$3.15 | A$6.20 | 49.2% |

| Gold Road Resources (ASX:GOR) | A$2.47 | A$4.63 | 46.7% |

| Vault Minerals (ASX:VAU) | A$0.365 | A$0.68 | 46% |

| Syrah Resources (ASX:SYR) | A$0.23 | A$0.42 | 45.2% |

We'll examine a selection from our screener results.

Life360 (ASX:360)

Overview: Life360, Inc. operates a technology platform for locating people, pets, and things across North America, Europe, the Middle East, Africa, and internationally with a market cap of A$5.64 billion.

Operations: The company generates revenue primarily from its Software & Programming segment, amounting to $342.92 million.

Estimated Discount To Fair Value: 24.6%

Life360 is trading at A$24.93, significantly below its estimated fair value of A$33.08, indicating potential undervaluation based on cash flows. Despite recent insider selling and revised revenue guidance due to lower hardware sales, the company maintains strong core subscription growth above 25% year-over-year. With earnings turning positive in Q3 2024 and expected profitability within three years, Life360's forecasted earnings growth of 50.97% annually positions it for robust future performance relative to the market.

- Our earnings growth report unveils the potential for significant increases in Life360's future results.

- Unlock comprehensive insights into our analysis of Life360 stock in this financial health report.

Charter Hall Group (ASX:CHC)

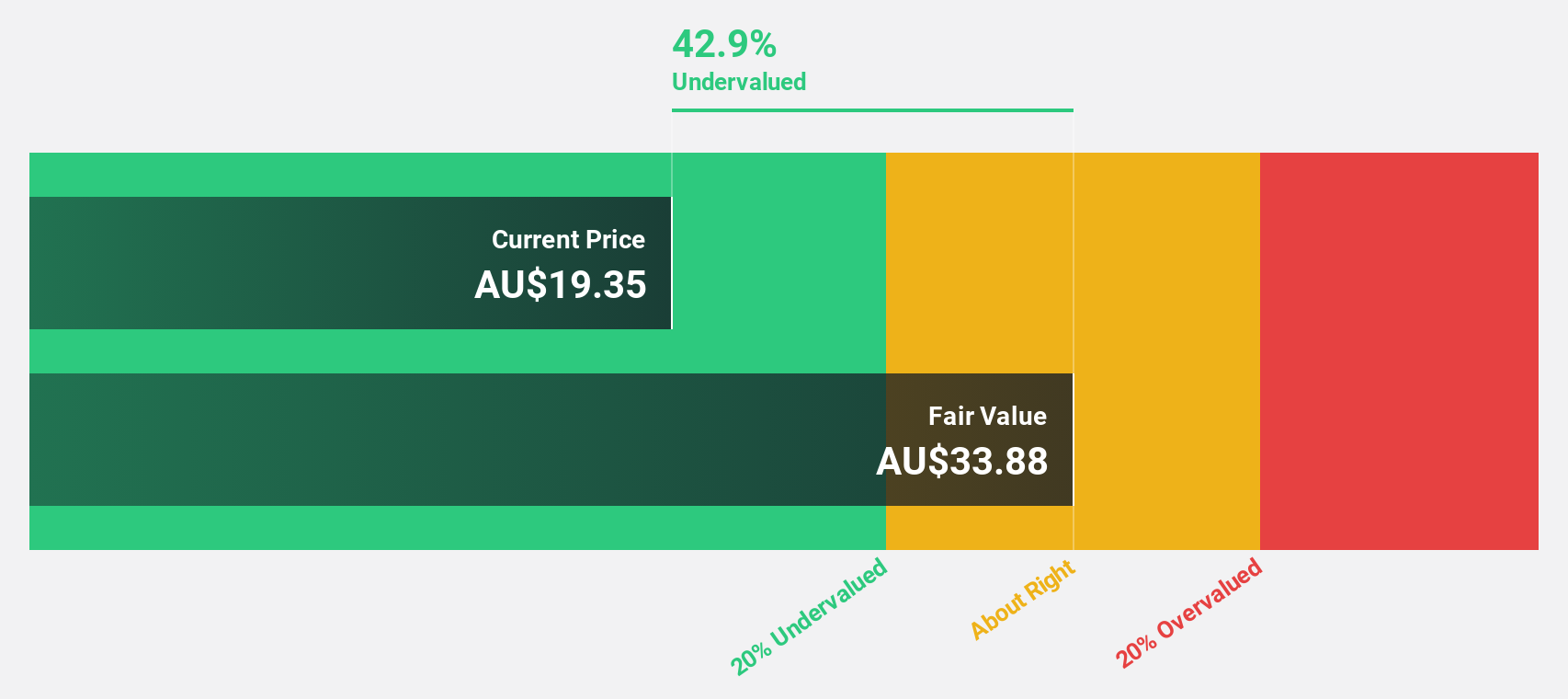

Overview: Charter Hall Group is a leading Australian fully integrated property investment and funds management group with a market cap of A$7.24 billion.

Operations: The company's revenue is derived from three main segments: Funds Management (A$448.60 million), Property Investments (A$322.80 million), and Development Investments (A$73.30 million).

Estimated Discount To Fair Value: 47.5%

Charter Hall Group, trading at A$15.31, is considerably undervalued based on cash flows with an estimated fair value of A$29.16, suggesting a 47.5% discount. While its Return on Equity is forecast to be low at 13.1% in three years, revenue growth of 10.1% annually surpasses the Australian market average of 6.1%. Recent discussions around potential M&A activities highlight strategic interest in expanding real estate investments amidst ongoing dividend affirmations and corporate maneuvers.

- Our growth report here indicates Charter Hall Group may be poised for an improving outlook.

- Click to explore a detailed breakdown of our findings in Charter Hall Group's balance sheet health report.

Praemium (ASX:PPS)

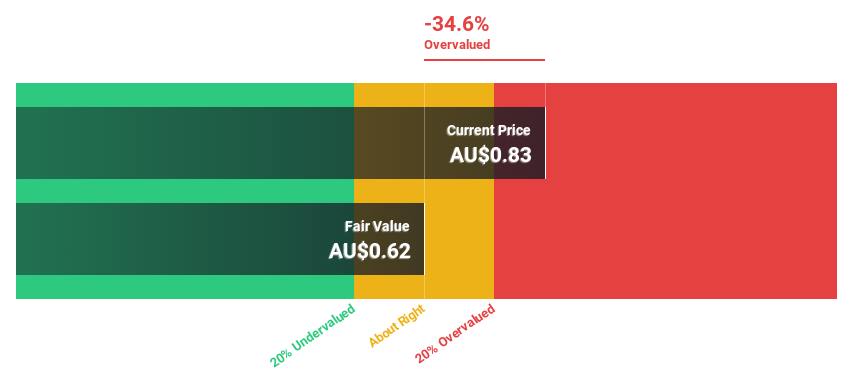

Overview: Praemium Limited, along with its subsidiaries, offers advisors and wealth management solutions through a seamless digital platform experience in Australia and internationally, with a market cap of A$408.45 million.

Operations: The company generates revenue of A$82.73 million from its Software & Programming segment.

Estimated Discount To Fair Value: 33.5%

Praemium, priced at A$0.86, is trading 33.5% below its estimated fair value of A$1.29, highlighting significant undervaluation based on cash flows. Despite a drop in profit margins from 20.4% to 10.6%, the company forecasts robust earnings growth of 27.5% annually over the next three years, outpacing the Australian market's average growth rate of 12.6%. Recent earnings calls underscore ongoing strategic adjustments aimed at enhancing financial performance and shareholder value.

- The growth report we've compiled suggests that Praemium's future prospects could be on the up.

- Take a closer look at Praemium's balance sheet health here in our report.

Seize The Opportunity

- Discover the full array of 46 Undervalued ASX Stocks Based On Cash Flows right here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:360

Life360

Operates a technology platform to locate people, pets, and things in North America, Europe, the Middle East, Africa, and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Community Narratives